PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1782127

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1782127

AI Hardware Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

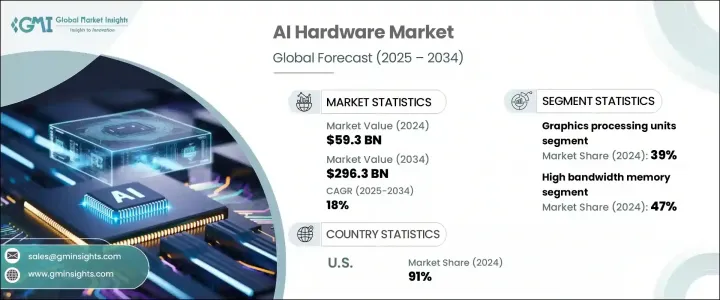

The Global AI Hardware Market was valued at USD 59.3 billion in 2024 and is estimated to grow at a CAGR of 18% to reach USD 296.3 billion by 2034. This strong growth trajectory is driven by the widespread adoption of artificial intelligence across diverse sectors, which has significantly amplified the need for high-performance computing infrastructure. As organizations increasingly deploy AI models with complex computational demands, there is a growing reliance on dedicated AI hardware capable of handling large-scale processing tasks.

Businesses are transitioning toward hardware that can support not only faster data throughput but also lower latency and greater energy efficiency. This trend is not limited to cloud environments alone; AI is also being implemented across edge computing environments, powering real-time decision-making in industrial systems, mobile devices, and embedded solutions. The proliferation of edge AI is further boosting demand for processors and memory units capable of operating independently without constant reliance on cloud services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $59.3 Billion |

| Forecast Value | $296.3 Billion |

| CAGR | 18% |

Across the processor landscape, the AI hardware market is segmented into graphics processing units (GPUs), central processing units (CPUs), tensor processing units (TPUs), application-specific integrated circuits (ASICs), field-programmable gate arrays (FPGAs), and neural processing units (NPUs). Among these, GPUs held the dominant share of the market in 2024, accounting for approximately 39% of total revenue. From 2025 to 2034, this segment is expected to grow at a CAGR exceeding 18%. The dominance of GPUs can be attributed to their unmatched capabilities in parallel computing, memory handling, and their efficiency in training and running inference models. These features have made GPUs essential to both enterprise-grade AI platforms and research institutions that require scalable performance for complex model development.

When viewed through the lens of memory and storage, the AI hardware market includes high bandwidth memory (HBM), AI-optimized DRAM, non-volatile memory, and emerging memory technologies. In 2024, the high bandwidth memory segment captured the largest share, contributing 47% of the total market. The segment is forecasted to expand at a CAGR of over 19% during the forecast period. This surge in demand is largely influenced by the growing need for speed and bandwidth in AI systems. As AI models become more sophisticated and data-heavy, high bandwidth memory enables near-instant data retrieval, which is critical for achieving seamless performance, particularly in real-time applications. This capability allows enterprises to minimize latency, enhance responsiveness, and better manage workload processing.

On the basis of application, data center and cloud computing remain the largest contributors to market revenue. The segment continues to expand rapidly as the need for scalable, high-performance infrastructure intensifies. The proliferation of AI models with massive training and inference requirements is driving companies to build data centers specifically designed to support AI workloads. These centers are equipped with cutting-edge accelerators and components tailored for efficient AI execution. Organizations are prioritizing investment in purpose-built infrastructure that not only meets current AI needs but also anticipates the demands of future models.

In regional terms, the United States led the AI hardware market in North America, accounting for nearly 91% of the regional revenue share and generating around USD 19.8 billion in 2024. This stronghold is driven by the country's leadership in technology innovation, a robust supply chain, and access to advanced semiconductor manufacturing capabilities. The U.S. remains a global hub for AI hardware development, supported by a rich ecosystem of hardware companies, research institutions, and cloud service providers.

Leading companies in the AI hardware market include NVIDIA, Intel, Qualcomm Technologies, Advanced Micro Devices (AMD), Apple, Google, Amazon Web Services (AWS), Microsoft, IBM, Samsung Electronics, and others. These firms are consistently investing in the development of custom chips, high-performance processors, and next-generation accelerators to support the evolving needs of AI-powered systems. Their efforts are crucial in shaping the next phase of the global AI hardware landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Processor

- 2.2.3 Memory and storage

- 2.2.4 Application

- 2.2.5 Deployment

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Proliferation of generative AI applications

- 3.2.1.2 Rapid expansion of edge AI deployment

- 3.2.1.3 Cloud & data center adoption

- 3.2.1.4 AI in healthcare & life sciences

- 3.2.1.5 Government AI investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High power consumption & cooling needs

- 3.2.2.2 Global chip supply constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for on-device AI

- 3.2.3.2 Government semiconductor incentives

- 3.2.3.3 AI supercomputing & hyperscale expansion

- 3.2.3.4 Growth of industry-specific AI applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Advanced process node development (3nm, 2nm)

- 3.7.1.2 High bandwidth memory (HBM) evolution

- 3.7.1.3 Chiplet architecture and modular design

- 3.7.2 Emerging technologies

- 3.7.2.1 Quantum computing hardware for AI

- 3.7.2.2 Photonic computing and optical AI hardware

- 3.7.2.3 Neuromorphic computing architectures

- 3.7.2.4 Advanced memory technologies

- 3.7.1 Current technological trends

- 3.8 Case studies

- 3.9 Use cases

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Processor, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Graphics processing unit (GPU)

- 5.2.1 Training

- 5.2.2 Inference

- 5.2.3 Edge

- 5.2.4 Data center

- 5.3 Central processing unit (CPU)

- 5.3.1 AI-optimized

- 5.3.2 Server CPU with AI acceleration

- 5.3.3 Edge computing

- 5.4 Tensor processing unit (TPU)

- 5.4.1 Cloud

- 5.4.2 Edge

- 5.4.3 Custom designs

- 5.5 Application-specific integrated circuit (ASIC)

- 5.5.1 AI training

- 5.5.2 AI inference

- 5.5.3 Custom AI

- 5.6 Field-programmable gate arrays (FPGA)

- 5.6.1 AI-optimized

- 5.6.2 Edge AI

- 5.6.3 Reconfigurable computing platforms

- 5.7 Neural processing units (NPU)

- 5.7.1 Smartphone

- 5.7.2 Edge AI

- 5.7.3 IoT

Chapter 6 Market Estimates & Forecast, By Memory & Storage, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 High bandwidth memory (HBM)

- 6.3 AI-optimized DRAM

- 6.4 Non-volatile memory

- 6.5 Emerging memory technologies

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Data center and cloud computing

- 7.3 Automotive and transportation

- 7.4 Healthcare and life sciences

- 7.5 Consumer electronics

- 7.6 Industrial and manufacturing

- 7.7 Financial services

- 7.8 Telecommunications

Chapter 8 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Cloud-Based

- 8.3 On-Premises

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Vietnam

- 9.4.6 Philippines

- 9.4.7 ANZ

- 9.4.8 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Advanced Micro Devices

- 10.2 Amazon Web Services (AWS)

- 10.3 Apple

- 10.4 ARM

- 10.5 Broadcom

- 10.6 Cerebra’s Systems

- 10.7 Fujitsu

- 10.8 Google

- 10.9 Graph core

- 10.10 IBM

- 10.11 Intel

- 10.12 Marvell Technology

- 10.13 Micron Technology

- 10.14 Microsoft

- 10.15 NVIDIA

- 10.16 Qualcomm Technologies

- 10.17 Samsung Electronics

- 10.18 SiPearl

- 10.19 SK Hynix

- 10.20 Tenstorrent