PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833429

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833429

China Diabetes Care Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

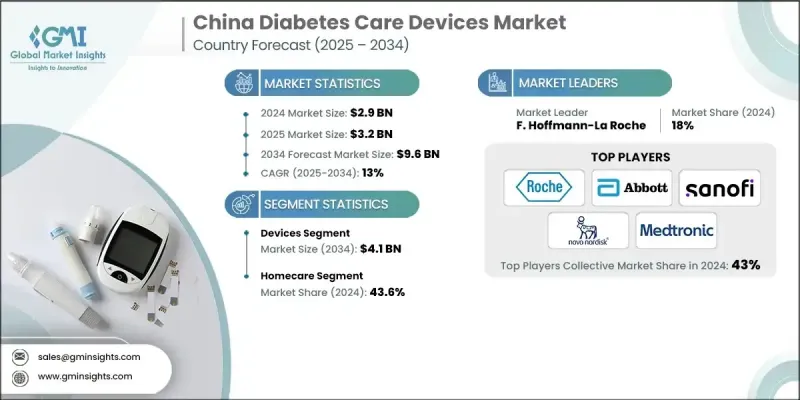

The China Diabetes Care Devices Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 13% to reach USD 9.6 billion by 2034.

China is facing an unprecedented diabetes burden, with over 140 million adults currently living with the condition. This epidemic is fueled by a combination of factors, including rapid urbanization, an aging population, increased consumption of processed foods, and declining physical activity levels.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $9.6 Billion |

| CAGR | 13% |

Rising Adoption of Devices

The devices segment held a notable share in 2024, encompassing blood glucose meters, test strips, insulin pens, insulin pumps, and continuous glucose monitoring (CGM) systems. With the country's diabetic population exceeding 140 million, there is constant demand for accurate, user-friendly tools that support long-term disease management. Companies are responding by introducing localized, cost-effective devices with smart features such as Bluetooth connectivity and mobile app integration. To strengthen their foothold, leading players are forming partnerships with local distributors, expanding regional manufacturing, and customizing product lines to meet cultural and economic preferences in urban and rural markets alike.

Homecare to Gain Traction

The homecare segment generated a significant share in 2024 as more patients shifted toward self-management and at-home monitoring. Factors such as the rising cost of in-clinic care, growing health consciousness, and the increasing prevalence of type 2 diabetes among middle-aged adults have all contributed to this trend. Companies are prioritizing ease of use, portability, and affordability while ensuring accuracy and reliability. Key strategies to capture this segment include launching direct-to-consumer online platforms, offering multilingual user support, and partnering with digital health apps to deliver personalized insights and remote monitoring capabilities. These approaches are helping companies build lasting relationships with patients and establish a dominant presence in China's evolving diabetes care ecosystem.

Major players in the China diabetes care devices market are Sinocare, B. Braun Melsungen, Insulet, Eli Lilly and Company, Ascensia Diabetes Care, Ypsomed Holding, Bionime, Novo Nordisk, Dr. Reddy's Laboratories, F. Hoffmann-La Roche, ARKRAY, Sanofi, Medtronic, Abbott Laboratories, Becton, Dickinson and Company.

To strengthen their foothold in the China diabetes care devices market, companies are focusing on a combination of localization, innovation, and strategic partnerships. Many global players are tailoring their product offerings to meet the unique needs of Chinese consumers, including language customization, simplified user interfaces, and pricing models suitable for a cost-sensitive market. Local manufacturing and assembly are being scaled up to reduce operational costs and ensure faster distribution, especially to underserved Tier 2 and Tier 3 cities. At the same time, companies are investing in digital health integration, linking devices with smartphone apps that allow for real-time glucose tracking, remote doctor consultations, and personalized health insights.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Escalating diabetes prevalence in China

- 3.2.1.2 Advancements in diabetes care device technology

- 3.2.1.3 Growing public and private sector initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of diabetes care devices

- 3.2.2.2 Stringent regulatory landscape

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding reach in underserved regions of China

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Diabetes epidemiology and disease burden analysis

- 3.6.1 Diabetes prevalence trends

- 3.6.2 Gestational diabetes prevalence

- 3.6.3 Complication rates and healthcare costs

- 3.7 Patent landscape analysis for diabetes device innovations

- 3.8 Clinical trial pipeline assessment for emerging technologies

- 3.9 Supply chain and distribution analysis

- 3.10 Pricing analysis, 2024

- 3.11 Future market trends

- 3.12 Gap analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Device

- 5.2.1 Blood glucose monitoring devices

- 5.2.1.1 Self-monitoring blood glucose meters

- 5.2.1.2 Continuous glucose monitors

- 5.2.2 Insulin delivery devices

- 5.2.2.1 Insulin pumps

- 5.2.2.1.1 Tubed pumps

- 5.2.2.1.2 Tubeless pumps

- 5.2.2.2 Pens

- 5.2.2.2.1 Reusable

- 5.2.2.2.2 Disposable

- 5.2.2.1 Insulin pumps

- 5.2.3 Other insulin delivery devices

- 5.2.1 Blood glucose monitoring devices

- 5.3 Consumables

- 5.3.1 Testing strips

- 5.3.2 Lancets

- 5.3.3 Pen needles

- 5.3.3.1 Standard

- 5.3.3.2 Safety

- 5.3.4 Syringes

- 5.3.5 Insulin pumps consumables

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospital

- 6.3 Ambulatory surgical centres

- 6.4 Diagnostic centres

- 6.5 Homecare

- 6.6 Other end use

Chapter 7 Company Profiles

- 7.1 Abbott Laboratories

- 7.2 ARKRAY

- 7.3 Ascensia Diabetes Care

- 7.4 B. Braun Melsungen

- 7.5 Becton, Dickinson and Company

- 7.6 Bionime

- 7.7 Dr. Reddy’s Laboratories

- 7.8 Eli Lilly and Company

- 7.9 F. Hoffmann-La Roche

- 7.10 Insulet

- 7.11 Medtronic

- 7.12 Novo Nordisk

- 7.13 Sanofi

- 7.14 Sinocare

- 7.15 Ypsomed Holding