PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1871171

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1871171

Compact Recloser Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

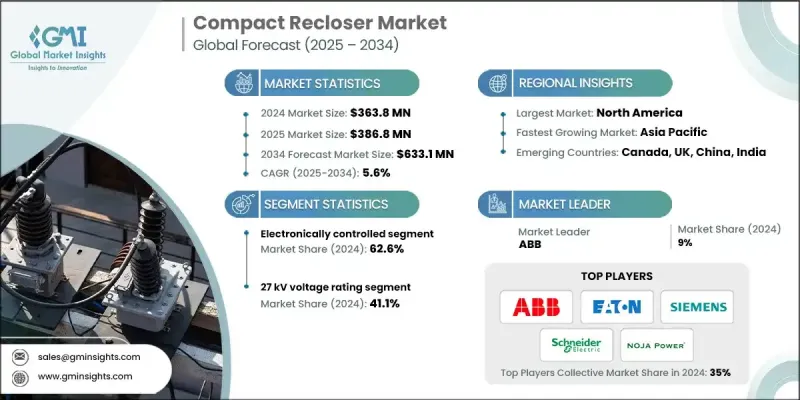

The Global Compact Recloser Market was valued at USD 363.8 million in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 633.1 million by 2034.

The rapid modernization of outdated electrical networks and the widespread integration of renewable power sources are the primary forces driving this market. As utilities move toward intelligent, highly resilient grid systems, compact reclosers have become indispensable for their ability to automate fault detection, isolation, and restoration. These systems help minimize outages and improve power reliability, making them essential for modern grid operations. Their small, flexible design allows utilities to retrofit them into existing setups without the need for extensive infrastructure modifications. In addition, global energy policies and large-scale utility investments are increasingly directed toward technologies that enhance remote monitoring, grid flexibility, and system resilience capabilities that compact reclosers deliver efficiently. The ongoing shift toward renewable energy generation has also intensified the need for responsive fault management tools. Compact reclosers help stabilize grids impacted by variable energy flows, maintaining smooth power distribution across decentralized systems and ensuring quick recovery after disruptions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $363.8 Million |

| Forecast Value | $633.1 Million |

| CAGR | 5.6% |

The electronically controlled compact reclosers segment held 62.6% share in 2024 and is expected to grow at a CAGR of 6.2% through 2034. The growing adoption of digital communication technologies, integration of smart sensors, and demand for modular and space-efficient equipment are fueling this segment's growth. Advanced electronic reclosers now support communication standards such as IEC 61850, Modbus, and DNP3, which enable real-time interaction with digital substations and centralized monitoring systems. Integrated sensors provide continuous data on voltage, current, and fault events, improving situational awareness and enhancing grid performance and safety.

The 15 kV compact recloser segment is forecasted to grow at a CAGR of 5.6% through 2034. Increasing focus on urban power distribution network optimization and the expansion of single-phase systems across emerging regions are accelerating the adoption of 15 kV units. These reclosers are well-suited for dense city grids and suburban environments where compact design and simplified installation are key advantages. Their efficiency and adaptability make them a preferred choice for managing low-voltage, space-limited applications.

United States Compact Recloser Market held 58.1% share, generating USD 83.8 million in 2024. The region is experiencing rapid advancements in grid modernization, driven by the replacement of outdated infrastructure with intelligent, automated recloser systems. Compact reclosers are being implemented widely to enhance service reliability, reduce downtime, and optimize overall grid performance. Utilities across the U.S. and Canada are prioritizing digital upgrades that allow faster fault isolation, improved restoration times, and long-term cost efficiency.

Leading players in the Global Compact Recloser Market include ABB, Siemens, Eaton, Schneider Electric, S&C Electric Company, NOJA Power Switchgear Pty Ltd, Tavrida Electric, G&W Electric, ENTEC Electric & Electronic Co., Ltd, Arteche Group, Hubbell Power Systems, Camlin Group, Pomanique Electric, Rockwill Electric Group, Hughes Power System, Sriwin Electric, Wenzhou Rena Electric Co., Ltd, Zhejiang Farady Powertech Co., Ltd, Chongqing Blue Jay Technology Co., Ltd, and Zhejiang Geya Electrical Co., Ltd. To strengthen their position, companies in the Compact Recloser Market are focusing on a combination of strategic initiatives. These include continuous investment in product innovation, integration of IoT and AI-based monitoring capabilities, and development of compact, maintenance-free designs tailored for next-generation smart grids. Strategic partnerships with utilities and regional distributors help expand geographic presence, while mergers and acquisitions accelerate technological advancement. Many firms are also prioritizing R&D to enhance fault detection accuracy and communication interoperability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.1.1 Business trends

- 2.1.2 Control trends

- 2.1.3 Interruption trends

- 2.1.4 Voltage trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Control, 2021 - 2034 (USD Million, Units)

- 5.1 Key trends

- 5.2 Electronic

- 5.3 Hydraulic

Chapter 6 Market Size and Forecast, By Interruption, 2021 - 2034 (USD Million, Units)

- 6.1 Key trends

- 6.2 Oil

- 6.3 Vacuum

Chapter 7 Market Size and Forecast, By Voltage Rating, 2021 - 2034 (USD Million, Units)

- 7.1 Key trends

- 7.2 15 kV

- 7.3 27 kV

- 7.4 38 kV

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Arteche Group

- 9.3 Camlin Group

- 9.4 Chongqing Blue Jay Technology Co., Ltd

- 9.5 Eaton

- 9.6 ENTEC Electric & Electronic Co., Ltd

- 9.7 G&W Electric

- 9.8 Hubbell Power Systems

- 9.9 Hughes Power System

- 9.10 NOJA Power Switchgear Pty Ltd

- 9.11 Pomanique Electric

- 9.12 Rockwill Electric Group

- 9.13 S&C Electric Company

- 9.14 Schneider Electric

- 9.15 Siemens

- 9.16 Sriwin Electric

- 9.17 Tavrida Electric

- 9.18 Wenzhou Rena Electric Co., Ltd

- 9.19 Zhejiang Farady Powertech Co., Ltd

- 9.20 Zhejiang Geya Electrical Co., Ltd