PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876610

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876610

Storage Vapor Recovery Units Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

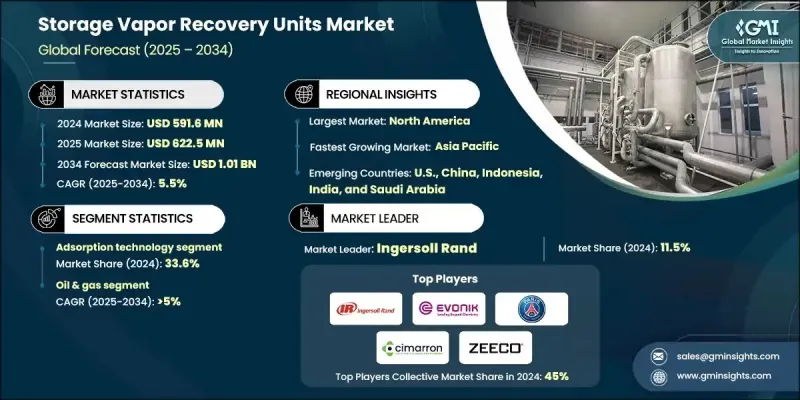

The Global Storage Vapor Recovery Units Market was valued at USD 591.6 million in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 1.01 billion by 2034.

The market's steady expansion is driven by advancements in modular and energy-efficient system design, coupled with the rising need for low-maintenance recovery solutions across industries. Storage vapor recovery units (VRUs) are engineered to capture and reclaim hydrocarbon vapors released from storage tanks during operations such as filling or temperature variations. These vapors contain volatile organic compounds that not only contribute to environmental pollution but also represent a loss of valuable hydrocarbons. The growing integration of smart sensors and remote monitoring systems is transforming the operational landscape by enabling predictive maintenance and improving transparency. Increasing emphasis on controlling VOC emissions in chemical and pharmaceutical storage facilities continues to propel the adoption of high-efficiency recovery technologies. Compact VRUs designed for small-scale and urban installations are witnessing rapid uptake, while activated carbon-based systems are gaining popularity due to their superior recovery efficiency and flexibility. Furthermore, the deployment of cryogenic condensation technologies in temperature-sensitive storage operations is creating new opportunities in specialized applications. Expanding regulatory frameworks addressing emission control beyond traditional oil and gas sectors are further driving demand for advanced vapor recovery infrastructure across multiple industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $591.6 Million |

| Forecast Value | $1.01 Billion |

| CAGR | 5.5% |

The condensation-based technology segment was valued at USD 137.1 million in 2024. Rising requirements for low-temperature vapor recovery are fueling the adoption of condensation-based VRUs, especially in chemical and pharmaceutical facilities. Continued innovation in mechanical and cryogenic condensation techniques is significantly improving vapor capture rates and enhancing the efficiency of industrial emission control.

The oil & gas sector is projected to grow at a CAGR of 5% between 2025 and 2034. The increasing development of upstream and midstream storage infrastructure is a major factor driving the need for vapor recovery units in oil and gas applications. Strengthening environmental regulations aimed at reducing hydrocarbon emissions from tank farms, refineries, and loading terminals has made the integration of VRUs a compliance imperative. With a growing emphasis on methane and VOC reduction strategies, these systems are becoming vital components in emission management frameworks throughout the energy industry.

Europe Storage Vapor Recovery Units Market was valued at USD 172.4 million in 2024. Strict regulatory standards under EU VOC directives are creating a robust environment for VRU adoption across industrial storage sites. Rising investment in sustainable logistics and environmentally responsible infrastructure continues to contribute to the region's market expansion. Ongoing adoption of advanced membrane and adsorption technologies is improving system efficiency and supporting the region's transition toward low-emission industrial practices.

Prominent companies operating in the Global Storage Vapor Recovery Units Market include Cimarron Energy, KAPPA GI, Koch Engineered Solutions, Cool Sorption, Ingersoll Rand, Tecam, ALMA Group, Kilburn Engineering, BORSIG, Evonik, Zeeco, VOCZero, Flogistix, SCS Technologies, S&S Technical, LeROI, PETROGAS, SYMEX Technologies, PSG, and Reynold India. Leading players in the Storage Vapor Recovery Units Market are focusing on product innovation, technological advancement, and strategic collaborations to strengthen their market position. Many companies are developing modular, plug-and-play VRUs equipped with smart sensors and digital monitoring to enhance operational efficiency and reduce maintenance needs. Firms are emphasizing energy optimization and system compactness to cater to space-constrained industrial settings. Strategic partnerships with end-users and EPC contractors are helping expand distribution networks and improve after-sales service.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 End Use trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of vapor recovery units

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization and IoT integration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Condensation

- 5.3 Adsorption

- 5.4 Absorption

- 5.5 Compression

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Oil & gas

- 6.3 Chemical & petrochemical

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.3.7 Norway

- 7.3.8 Poland

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Indonesia

- 7.4.6 Malaysia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Egypt

- 7.5.5 Oman

- 7.5.6 South Africa

- 7.5.7 Nigeria

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Mexico

- 7.6.3 Argentina

Chapter 8 Company Profiles

- 8.1 ALMA Group

- 8.2 BORSIG

- 8.3 Cimarron Energy

- 8.4 Cool Sorption

- 8.5 Evonik

- 8.6 Flogistix

- 8.7 Ingersoll Rand

- 8.8 KAPPA GI

- 8.9 Kilburn Engineering

- 8.10 Koch Engineered Solutions

- 8.11 LeROI

- 8.12 PETROGAS

- 8.13 PSG

- 8.14 Reynold India

- 8.15 S&S Technical

- 8.16 SCS Technologies

- 8.17 SYMEX Technologies

- 8.18 Tecam

- 8.19 VOCZero

- 8.20 Zeeco