PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1913331

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1913331

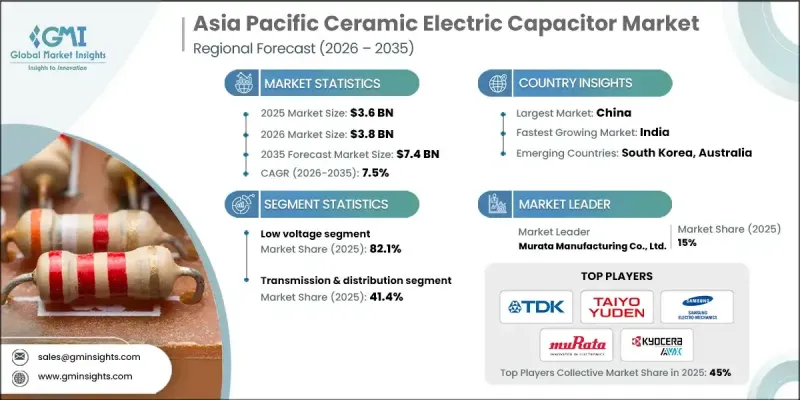

Asia Pacific Ceramic Electric Capacitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

Asia Pacific Ceramic Electric Capacitor Market was valued at USD 3.6 billion in 2025 and is estimated to grow at a CAGR of 7.5% to reach USD 7.4 billion by 2035.

The region's rapid shift toward vehicle electrification and deployment of high-voltage power electronics is significantly shaping market dynamics. As automakers and industrial players embrace electrified mobility, demand for ceramic capacitors capable of withstanding higher voltages, rapid switching, and tight thermal conditions is surging. Applications such as on-board chargers, traction inverters, and DC-DC converters increasingly rely on SiC MOSFET technologies, driving the adoption of C0G/X7R MLCCs that offer high stability, low losses, and robust voltage endurance. Standard features like AEC-Q200 automotive reliability, miniaturization without capacitance compromise, and soft terminations are essential to reduce ESR and withstand mechanical stress. Concurrently, the ongoing 5G and 5G-A rollout across APAC is boosting requirements for RF front ends, small cells, edge computing, and power regulation modules, all of which depend on high-performance ceramic capacitors for decoupling, noise suppression, and timing. Expansion of network infrastructure, coupled with emerging 5G-A applications such as industrial private networks and low-latency control, further strengthens multi-year demand for MLCCs in base stations and connected devices.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.6 Billion |

| Forecast Value | $7.4 Billion |

| CAGR | 7.5% |

The low-voltage segment held an 82.1% share in 2025 and is expected to grow at a CAGR of 7% through 2035. Low-voltage MLCCs are crucial across consumer electronics, automotive controls, and power-supply decoupling, as designers require higher capacitance in smaller footprints to support miniaturization in smartphones, wearables, and sensor modules.

The consumer electronics segment is anticipated to grow at a CAGR of 6.5% by 2035, driven by OEM demand for capacitors with high capacitance per unit volume, precise tolerances, temperature stability, and dielectric reliability to support faster processors and AI accelerators in compact devices.

China Ceramic Electric Capacitor Market accounted for 37.9% share in 2025, generating USD 1.3 billion. The country's advanced manufacturing initiatives, including industrial automation, smart factories, and integrated digital infrastructure, are driving MLCC demand across RF modules, edge devices, robotics, and power conversion systems.

Leading players in the Asia Pacific Ceramic Electric Capacitor Market include Murata Manufacturing Co., Ltd., Panasonic, TDK Corporation, Vishay, ABB, Wima, Nichicon, KYOCERA AVX Components Corporation, ROHM, Samsung Electro-Mechanics, Elna, Schneider Electric, Taiyo Yuden, Havells, Xuansn, Kemet, Cornell Dubilier, Siemens, Walsin, and Yageo Corporation. To strengthen their presence, companies in the Asia Pacific Ceramic Electric Capacitor Market are focusing on continuous R&D to enhance dielectric materials, voltage tolerance, and thermal stability. Strategic investments in automation and smart manufacturing enable higher production efficiency and product consistency. Firms are expanding regional distribution networks and collaborating with OEMs to secure long-term supply contracts, while adopting cost-effective production techniques to remain competitive.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Voltage trends

- 2.1.3 End use trends

- 2.1.4 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Voltage, 2022 - 2035 (USD Million, ‘000 Units)

- 5.1 Key trends

- 5.2 Low

- 5.3 Medium

- 5.4 High

Chapter 6 Market Size and Forecast, By End use, 2022 - 2035 (USD Million, ‘000 Units)

- 6.1 Key trends

- 6.2 Consumer electronics

- 6.3 Automotive

- 6.4 Communications & technology

- 6.5 Transmission & distribution

- 6.6 Others

Chapter 7 Market Size and Forecast, By Country, 2022 - 2035 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 China

- 7.3 India

- 7.4 Japan

- 7.5 South Korea

- 7.6 Australia

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Cornell Dubilier

- 8.3 Elna

- 8.4 Havells

- 8.5 Kemet

- 8.6 KYOCERA AVX Components Corporation

- 8.7 Murata Manufacturing Co., Ltd.

- 8.8 Nichicon

- 8.9 Panasonic

- 8.10 ROHM

- 8.11 Samsung Electro-Mechanics

- 8.12 Schneider Electric

- 8.13 Siemens

- 8.14 Taiyo Yuden

- 8.15 TDK Corporation

- 8.16 Vishay

- 8.17 Walsin

- 8.18 Wima

- 8.19 Xuansn

- 8.20 Yageo Corporation