PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1928929

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1928929

Low Speed Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

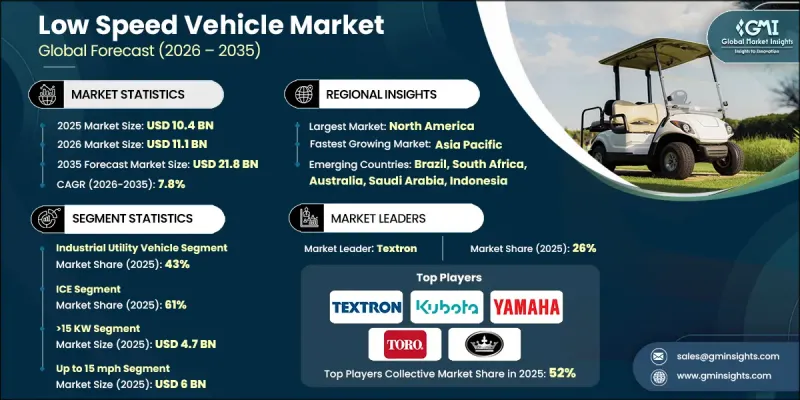

The Global Low Speed Vehicle Market was valued at USD 10.4 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 21.8 billion by 2035.

Rising urbanization worldwide is intensifying traffic congestion, air pollution, and noise, creating an urgent demand for sustainable, efficient transportation alternatives. LSVs are emerging as a practical solution for short-distance travel in densely populated urban areas, gated communities, resorts, campuses, and industrial facilities. These vehicles, powered by electricity or alternative fuels, produce minimal emissions, supporting cleaner air and reduced environmental impact. Their compact design and speed limitations make them safe and maneuverable in crowded settings. Advances in EV battery technology, including higher energy density, faster charging, and longer lifecycle, have significantly increased LSV efficiency and appeal. These improvements lower operating costs and enhance performance, making LSVs attractive for personal mobility, commercial logistics, and industrial applications. While the COVID-19 pandemic created mixed market effects, demand for low-emission and cost-effective transportation solutions continues to grow globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.4 Billion |

| Forecast Value | $21.8 Billion |

| CAGR | 7.8% |

The industrial utility vehicle segment held a 43% share in 2025 and is projected to grow at a CAGR of 8.9% from 2026 to 2035. Industrial LSVs are essential in manufacturing, construction, logistics, and other commercial applications due to their rugged design, extended duty cycles, and payload capacities of 1,500-2,500 lbs.

The internal Combustion Engine (ICE) vehicles segment held a 61% share in 2025, expected to grow at a CAGR of 7.1% through 2035. ICE LSVs retain a significant market presence because of operational range advantages, ease of refueling, and suitability for specific applications, typically powered by 3-10 horsepower engines with automated or continuously variable transmissions.

United States Low Speed Vehicle Market generated USD 3.8 billion in 2025. The demand is driven by widespread adoption in gated communities, recreational spaces, campuses, and industrial facilities, supported by regulations permitting LSVs on select public roads and increasing electrification efforts in logistics and materials handling operations.

Key players in the Global Low Speed Vehicle Market include Bradshaw EV, Columbia Vehicle, Polaris GEM, EVolution Electric Vehicles, Yamaha Motor, Textron, Deere & Company, Star EV, The Toro Company, and KUBOTA. Companies in the Global Low Speed Vehicle Market are strengthening their positions through continuous innovation in battery technology, enhancing vehicle efficiency, and extending lifecycle performance. Manufacturers are expanding product lines to target industrial, commercial, and personal mobility sectors. Strategic partnerships, acquisitions, and collaborations enable faster market penetration and global reach. Firms are also investing in digital marketing, e-commerce channels, and localized distribution to increase brand visibility. Electrification initiatives, after-sales support, and customized solutions for logistics and gated communities further solidify market foothold and long-term competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Power Output

- 2.2.5 Speed Class

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel

- 3.1.1.6 End Use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Urban mobility inside gated/controlled areas

- 3.2.1.2 Tourism, hospitality & leisure expansion

- 3.2.1.3 Electrification push & sustainability mandates

- 3.2.1.4 Operational cost savings

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Range & performance limitations

- 3.2.2.2 Limited road access & regulatory inconsistencies

- 3.2.3 Market opportunities

- 3.2.3.1 Lithium-ion replacing lead-acid

- 3.2.3.2 Connected / telematics-enabled LSV fleets

- 3.2.3.3 Customization & modular utility bodies

- 3.2.3.4 Premium & lifestyle LSVs for residential use

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 U.S. NHTSA Low-Speed Vehicle (LSV) Standards (FMVSS 500)

- 3.5.1.2 U.S. State-Level Street-Legal LSV Rules

- 3.5.1.3 Canada Transport Canada LSV Regulations

- 3.5.2 Europe

- 3.5.2.1 EU Quadricycle Category L6e / L7e

- 3.5.2.2 UNECE Vehicle Safety Regulations

- 3.5.2.3 EU Battery Regulation

- 3.5.2.4 EU End-of-Life Vehicle Directive

- 3.5.3 Asia-Pacific

- 3.5.3.1 China GB Standards for NEVs and LSVs

- 3.5.3.2 India CMVR Rules for Electric Vehicles

- 3.5.3.3 Japan MLIT Micro-Mobility Regulations

- 3.5.4 Latin America

- 3.5.4.1 Brazil CONTRAN Standards

- 3.5.4.2 Argentina IRAM Standards

- 3.5.4.3 Mexico NOM Vehicle Standards

- 3.5.5 Middle East & Africa

- 3.5.5.1 Saudi Arabia SASO Standards

- 3.5.5.2 UAE ESMA Regulations

- 3.5.5.3 GSO Gulf Standards for Electric Vehicles

- 3.5.5.4 South Africa SANS Regulations

- 3.5.1 North America

- 3.6 Porter';s analysis

- 3.7 PESTEL analysis

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Patent analysis

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Vehicle Architecture & Platform Strategy

- 3.12.1 Chassis & skateboard platforms

- 3.12.2 Modular body & utility attachment strategy

- 3.12.3 Platform reuse across applications

- 3.13 OEM vs Regional Assembler Landscape

- 3.13.1 Local assemblers vs branded OEMs

- 3.13.2 White-label / private-label manufacturing

- 3.13.3 CKD/SKD assembly trends

- 3.14 Fleet Ownership & Buying Behavior Analysis

- 3.14.1 Fleet buyers vs individual buyers

- 3.14.2 Purchase vs lease vs managed fleet models

- 3.14.3 Replacement cycles and utilization rates

- 3.15 Feasibility & adoption of low-speed vehicles assessment

- 3.15.1 Total Cost of Ownership (TCO) benchmarking

- 3.15.2 Battery, charging & powertrain viability

- 3.15.3 Street-legality & compliance economics

- 3.15.4 Application-level ROI & payback

- 3.15.5 Infrastructure readiness & operating risk

- 3.16 Distribution & Go-To-Market Models

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Golf Cart

- 5.3 Commercial utility vehicle

- 5.4 Industrial utility vehicle

- 5.5 Personal mobility vehicle

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

Chapter 7 Market Estimates & Forecast, By Power Output, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 >15 KW

- 7.3 6-15KW

- 7.4 <15KW

Chapter 8 Market Estimates & Forecast, By Speed Class, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Up to 15 mph

- 8.3 15-25 mph

- 8.4 Above 25 mph

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Golf courses

- 9.3 Hotels & resorts

- 9.4 Airports

- 9.5 Industrial facilities

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Columbia Vehicle

- 11.1.2 Deere & Company

- 11.1.3 Garia

- 11.1.4 ICON Electric Vehicles

- 11.1.5 Kandi Technologies

- 11.1.6 KUBOTA

- 11.1.7 Polaris GEM

- 11.1.8 Star EV

- 11.1.9 Textron

- 11.1.10 The Toro Company

- 11.1.11 Tomberlin

- 11.1.12 Yamaha Motor

- 11.2 Regional players

- 11.2.1 American Landmaster

- 11.2.2 Bradshaw EV

- 11.2.3 Moto Electric Vehicles

- 11.2.4 Motrec International

- 11.2.5 Suzhou Eagle Electric Vehicle Manufacturing

- 11.2.6 EVolution Electric Vehicles

- 11.2.7 Melex

- 11.2.8 Bintelli

- 11.3 Emerging players

- 11.3.1 Stealth

- 11.3.2 Tropos Motors

- 11.3.3 Marshell

- 11.3.4 Durable EV

- 11.3.5 Eco Vehicle brands