PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936671

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936671

Motor Driver IC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

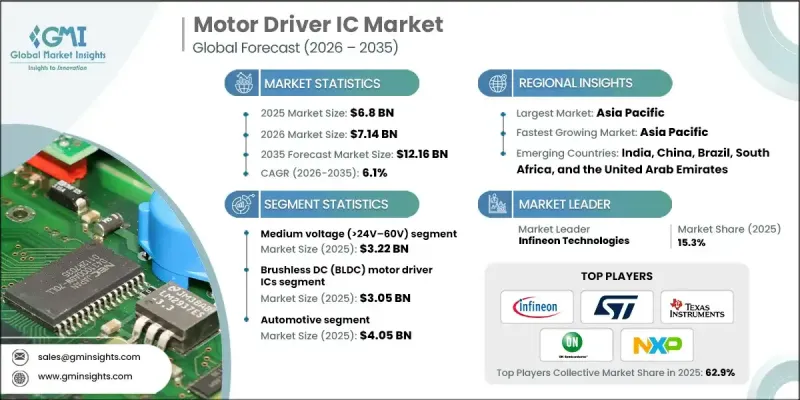

The Global Motor Driver IC Market was valued at USD 6.8 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 12.16 billion by 2035.

Market growth is driven by rapid electrification across industries, rising motor density in electric and hybrid vehicles, stricter energy efficiency mandates, and increasing adoption of automation and smart motion control technologies. Motor driver ICs play a critical role by acting as the interface between control electronics and electric motors, enabling precise regulation of speed, torque, and direction. Expanding use of smart appliances and connected systems is further accelerating demand, as motor driver ICs support variable-speed operation and energy optimization. Industrial automation, robotics, and intelligent manufacturing continue to increase reliance on efficient motor control solutions. The market is also benefiting from the transition toward advanced motor technologies that enhance system performance, reliability, and operational efficiency across automotive, industrial, and consumer applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.8 Billion |

| Forecast Value | $12.16 Billion |

| CAGR | 6.1% |

The medium-voltage segment, ranging from above 24V to 60V, accounted for USD 3.22 billion in 2025. These motor driver ICs are adopted due to their balance of power capability, efficiency, and cost-effectiveness. Demand is driven by increased deployment in automation systems, electrified transport solutions, and industrial environments that require scalable and reliable motion control. Manufacturers are focusing on delivering medium-voltage ICs with integrated protection features and diagnostic capabilities to meet growing performance and safety expectations across industrial and automotive platforms.

The brushless DC motor driver ICs segment generated USD 3.05 billion in 2025. Strong adoption of brushless motor technology has fueled demand for advanced driver ICs capable of delivering precise control, higher efficiency, and enhanced system protection. As adoption of intelligent motion systems accelerates, manufacturers are emphasizing compact designs with integrated diagnostics and energy-optimized control functions to support a wide range of applications across multiple end-use sectors.

North America Motor Driver IC Market accounted for 21% share in 2025 and continues to demonstrate steady growth. Regional expansion is supported by advanced manufacturing infrastructure, accelerating electrification trends, and increased automation investments. Strong demand from automotive, industrial, and technology-driven sectors is sustaining adoption. Ongoing digital transformation initiatives and investments in semiconductor innovation further reinforce long-term growth opportunities, positioning North America as a key regional market with diversified demand.

Key companies operating in the Global Motor Driver IC Market include Infineon Technologies, Texas Instruments (TI), STMicroelectronics (ST), NXP Semiconductors, ON Semiconductor (onsemi), Analog Devices (ADI), Renesas Electronics, Toshiba Corporation, ROHM Semiconductor, Microchip Technology, Allegro MicroSystems, Monolithic Power Systems (MPS), Mitsubishi Electric, Panasonic Corporation, and Fuji Electric. Companies in the motor driver IC market are deploying a combination of innovation-driven and expansion-focused strategies to strengthen their competitive position. Significant investments in research and development are enabling the creation of high-efficiency ICs with advanced control, protection, and diagnostic capabilities. Firms are expanding product portfolios to address low-, medium-, and high-voltage applications across automotive, industrial, and consumer sectors. Strategic collaborations with OEMs and system integrators help accelerate adoption and ensure design wins in next-generation platforms. Geographic expansion and capacity investments improve supply resilience and reduce lead times.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Motor type trends

- 2.2.2 Voltage range trends

- 2.2.3 Power semiconductor material trends

- 2.2.4 Level of integration trends

- 2.2.5 Application trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electrification of vehicles increasing motor count

- 3.2.1.2 Energy efficiency regulations boosting motor upgrades

- 3.2.1.3 Growth in industrial automation and robotics

- 3.2.1.4 Shift toward BLDC and servo motors

- 3.2.1.5 Rising motor usage in smart appliances

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 Automotive qualification complexity and long cycles

- 3.2.2.2 Thermal limits in high power applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Initiatives

- 3.11 Supply Chain Resilience

- 3.12 Geopolitical Analysis

- 3.13 Digital Transformation

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Motor Type, 2022 - 2035 (USD Million & Million Units)

- 5.1 Key trends

- 5.2 Brushed DC motor driver ICs

- 5.3 Brushless DC (BLDC) motor driver ICs

- 5.4 Stepper motor driver ICs

- 5.5 Servo motor driver ICs

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Voltage Range, 2022 - 2035 (USD Million & Million Units)

- 6.1 Key trends

- 6.2 Low voltage (≤24V)

- 6.3 Medium voltage (>24V-60V)

- 6.4 High voltage (>60V)

Chapter 7 Market Estimates and Forecast, By Power Semiconductor Material, 2022 - 2035 (USD Million & Million Units)

- 7.1 Key trends

- 7.2 Silicon (Si)

- 7.3 Silicon Carbide (SiC)

- 7.4 Gallium Nitride (GaN)

Chapter 8 Market Estimates and Forecast, By Level of Integration, 2022 - 2035 (USD Million & Million Units)

- 8.1 Key trends

- 8.2 Gate driver ICs

- 8.3 Integrated power drivers

- 8.4 Fully integrated motor driver SoCs

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million & Million Units)

- 9.1 Key trends

- 9.2 Automotive

- 9.2.1 Powertrain control

- 9.2.2 Body electronics

- 9.2.3 Infotainment

- 9.2.4 Others

- 9.3 Consumer electronics

- 9.3.1 Home appliances

- 9.3.2 Personal devices

- 9.4 Healthcare

- 9.5 Chemical

- 9.6 Military and defense

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Texas Instruments (TI)

- 11.1.2 Infineon Technologies

- 11.1.3 STMicroelectronics (ST)

- 11.1.4 NXP Semiconductors

- 11.1.5 Analog Devices (ADI)

- 11.1.6 ON Semiconductor (onsemi)

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 Microchip Technology

- 11.2.1.2 Monolithic Power Systems (MPS)

- 11.2.1.3 Allegro MicroSystems

- 11.2.2 Europe

- 11.2.2.1 ROHM Semiconductor

- 11.2.2.2 Renesas Electronics

- 11.2.3 Asia Pacific

- 11.2.3.1 Toshiba Corporation

- 11.2.3.2 Mitsubishi Electric

- 11.2.3.3 Panasonic Corporation

- 11.2.3.4 Fuji Electric

- 11.2.1 North America