PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959320

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959320

Food-grade Excipients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

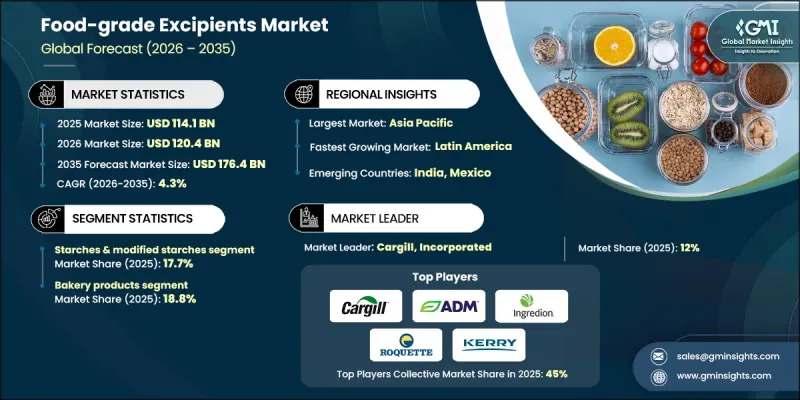

The Global Food-grade Excipients Market was valued at USD 114.1 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 176.4 billion by 2035.

The market is described as undergoing a strategic shift as food manufacturers, nutraceutical developers, and functional ingredient producers increasingly prioritize formulation safety, stability, and transparency. Ingredients once regarded as secondary inputs are now positioned as critical to meeting regulatory expectations, improving formulation performance, and enabling product differentiation. Food-grade excipients are widely recognized for their ability to support structural integrity, improve texture, regulate release behavior, and enhance processing efficiency. Advances in formulation science are enabling excipients to deliver enhanced functional performance, supporting the design and innovation of complex food systems. The industry is also described as placing strong emphasis on clean-label positioning, ingredient traceability, and full disclosure practices to strengthen consumer confidence. Sustainability considerations are increasingly integrated into sourcing and production strategies, shaping competitive positioning across the global market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $114.1 Billion |

| Forecast Value | $176.4 Billion |

| CAGR | 4.3% |

The starches and modified starches segment held a share of 17.7% in 2025 and is anticipated to grow at a CAGR of 3.1% through 2035. This segment is supported by a broad functional role in enhancing structure, consistency, and binding performance across multiple food systems. Other excipient categories continue to gain relevance due to their ability to manage moisture, stabilize formulations, improve sensory characteristics, and ensure uniformity across both legacy and reformulated products.

The bakery-related applications segment held 18.8% share in 2025 and is expected to grow at a CAGR of 4% during the 2026-2035 period. Food manufacturers rely on excipients to maintain consistency, structural stability, and sensory balance during processing and storage. These ingredients are also widely used to replicate traditional product attributes in reformulated offerings while maintaining stability and overall performance.

North America Food-grade Excipients Market held a 27.7% share in 2025. The region benefits from a mature regulatory environment that emphasizes safety, quality assurance, and ingredient transparency. As dietary preferences continue to evolve, manufacturers in the region increasingly depend on high-performance excipients to maintain texture, flavor delivery, stability, and consistency across diverse product portfolios.

Key companies active in the Global Food-grade Excipients Market include Ingredion Incorporated, Cargill, Incorporated, Roquette Freres, Kerry Group plc, DSM-Firmenich, Archer Daniels Midland Company, Corbion N.V., DuPont de Nemours, Inc., BENEO GmbH, Jungbunzlauer Suisse AG, Ashland Global Holdings Inc., J. Rettenmaier & Sohne GmbH + Co KG, CP Kelco, Palsgaard A/S, TIC Gums, and Silvateam S.p.A. Companies operating in the food-grade excipients market are reinforcing their market positions through targeted investments in research and formulation science. Many players are expanding clean-label and multifunctional excipient portfolios to address evolving regulatory and consumer expectations. Strategic partnerships with food manufacturers and ingredient developers are being used to accelerate innovation and application-specific customization. Firms are also strengthening supply chain transparency and sustainability credentials to support brand trust. Capacity expansion, geographic diversification, and process optimization remain central strategies, while digital quality control and traceability systems are increasingly adopted to improve compliance, efficiency, and customer engagement across global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for processed & convenience foods

- 3.2.1.2 Growth of plant-based food industry

- 3.2.1.3 Clean label & natural ingredient trends

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory requirements & approval delays

- 3.2.2.2 Consumer skepticism toward synthetic additives

- 3.2.3 Market opportunities

- 3.2.3.1 Microencapsulation for controlled release applications

- 3.2.3.2 Bio-based & fermentation-derived excipients

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Starches & modified starches

- 5.3 Hydrocolloids (gums)

- 5.4 Emulsifiers

- 5.5 Sweeteners & polyols

- 5.6 Cellulose & cellulose derivatives

- 5.7 Preservatives & antimicrobials

- 5.8 Fibers & bulking agents

- 5.9 Colorants

- 5.10 Anticaking agents

- 5.11 Acidulants & ph regulators

- 5.12 Proteins & enzymes

- 5.13 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Bakery products

- 6.3 Beverages

- 6.4 Confectionery

- 6.5 Dairy & dairy alternatives

- 6.6 Meat & meat alternatives

- 6.7 Sauces, dressings & condiments

- 6.8 Snacks & convenience foods

- 6.9 Infant & baby food

- 6.10 Nutraceuticals & dietary supplements

- 6.11 Frozen foods

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Cargill, Incorporated

- 8.2 Ingredion Incorporated

- 8.3 Kerry Group plc

- 8.4 Archer Daniels Midland Company (ADM)

- 8.5 DuPont de Nemours, Inc.

- 8.6 DSM-Firmenich

- 8.7 Ashland Global Holdings Inc.

- 8.8 BENEO GmbH (Sudzucker Group)

- 8.9 Roquette Freres

- 8.10 Corbion N.V.

- 8.11 Jungbunzlauer Suisse AG

- 8.12 J. Rettenmaier & Sohne GmbH + Co KG (JRS)

- 8.13 Palsgaard A/S

- 8.14 CP Kelco (J.M. Huber Corporation)

- 8.15 TIC Gums (Ingredion)

- 8.16 Silvateam S.p.a.