PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959330

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959330

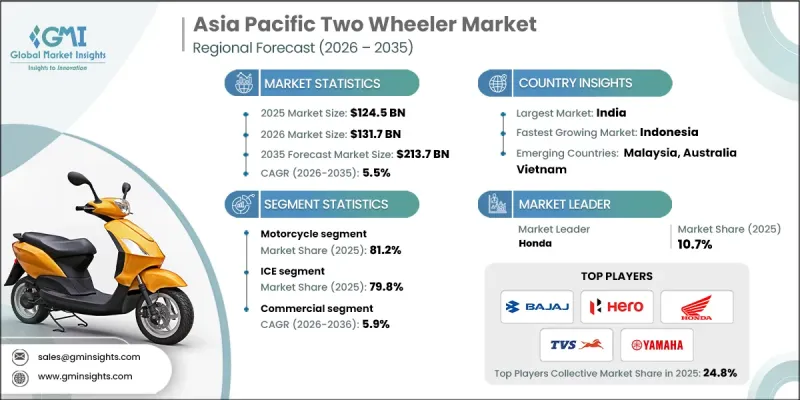

Asia Pacific Two Wheeler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

Asia Pacific Two Wheeler Market was valued at USD 124.5 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 213.7 billion by 2035.

Two-wheelers account for a substantial portion of annual vehicle sales across the region due to their affordability, fuel efficiency, and suitability for dense urban traffic. Nations with heavy congestion and relatively lower per capita income contribute significantly to volume demand, while economies with higher income levels are increasingly driving demand for premium motorcycles. The region has also emerged as a global hub for electric two-wheeler adoption, with China, India, and Vietnam collectively accounting for 95% of worldwide electric two-wheeler sales in 2025, according to the International Council on Clean Transportation. This rapid shift highlights the strong return potential for investments in electric motorcycles, scooters, and mopeds. Growth is further supported by expanding charging networks, improving after-sales ecosystems, rising environmental awareness among consumers, and active policy support through subsidies and incentives. These dynamics are accelerating the transition toward sustainable mobility while encouraging hesitant buyers to adopt electric two-wheelers.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $124.5 Billion |

| Forecast Value | $213.7 Billion |

| CAGR | 5.5% |

The motorcycles segment held 81.2% share in 2025 and generated USD 101.1 billion. Their dominance is driven by wide consumer acceptance across commuting, leisure, and performance-oriented use cases. Motorcycles appeal to a broad demographic range due to their design flexibility, performance options, and adaptability to different riding needs, which continues to strengthen their leadership over scooters across the region.

The internal combustion engine two-wheelers segment accounted for 79.8% share in 2025 and is projected to reach USD 158.6 billion by 2035. Conventional fuel-powered models continue to lead due to their long-standing presence, established manufacturing ecosystems, and widespread fuel availability. While electric alternatives are gaining momentum, limited charging accessibility in certain areas has sustained the relevance of ICE-powered motorcycles and scooters.

China Two Wheeler Market reached USD 28.9 billion in 2025, making it the second-largest market in the Asia Pacific region. Market strength is driven by high population density, strong electric vehicle policies, and the presence of domestic manufacturers. Urban mobility regulations, including restrictions on private car usage, have increased reliance on compact and efficient two-wheelers, particularly electric models, for short-distance travel.

Key companies actively operating in the Asia Pacific Two Wheeler Market include Yamaha, Bajaj Auto, Suzuki, Yadea, Hero, TVS, Honda, Royal Enfield, Kawasaki, and Loncin Motor. Companies across the Asia Pacific two-wheeler market focus on product innovation, electric portfolio expansion, and localized manufacturing to reinforce their market position. Manufacturers invest heavily in battery technology, range improvement, and cost optimization to make electric models more accessible. Strategic partnerships with component suppliers and charging solution providers help improve ecosystem readiness. Brands also emphasize expanding dealership networks, enhancing digital sales platforms, and strengthening after-sales support to improve customer retention. Customization options and premium model launches are used to capture higher-income segments, while competitive pricing strategies target mass-market buyers.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Displacement

- 2.2.5 Distribution Channel

- 2.2.6 End Use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising middle-class population

- 3.2.1.2 Traffic congestion in mega cities

- 3.2.1.3 Fuel efficiency advantages

- 3.2.1.4 Expanding e-commerce and delivery services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Safety concerns and accident rates

- 3.2.2.2 Volatility in fuel prices

- 3.2.3 Market opportunities

- 3.2.3.1 Rapid adoption of electric two wheelers

- 3.2.3.2 Development of battery swapping infrastructure

- 3.2.3.3 Growth of shared mobility services

- 3.2.3.4 Expansion of charging infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 China

- 3.4.1.1 Ministry of Industry and Information Technology (MIIT)

- 3.4.1.2 State Administration for Market Regulation (SAMR)

- 3.4.1.3 China Quality Certification Center (CQC)

- 3.4.1.4 National Standards Committee

- 3.4.2 India

- 3.4.2.1 Ministry of Road Transport & Highways (MoRTH)

- 3.4.2.2 Automotive Research Association of India (ARAI)

- 3.4.2.3 Bureau of Indian Standards (BIS)

- 3.4.2.4 State Transport Authorities

- 3.4.3 Japan

- 3.4.3.1 Ministry of Land, Infrastructure, Transport and Tourism (MLIT)

- 3.4.3.2 Ministry of Environment (MOE)

- 3.4.3.3 Ministry of Economy, Trade and Industry (METI)

- 3.4.3.4 Japan Automobile Federation (JAF)

- 3.4.4 South Korea

- 3.4.4.1 Ministry of Land, Infrastructure and Transport (MOLIT)

- 3.4.4.2 Ministry of Environment (MoE)

- 3.4.4.3 Korean Motor Vehicle Safety Standards (KMVSS)

- 3.4.5 Malaysia

- 3.4.5.1 Road Transport Department

- 3.4.5.2 Department of Standards Malaysia

- 3.4.5.3 Malaysian Institute of Road Safety Research

- 3.4.1 China

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By country

- 3.8.2 By vehicle

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact

- 3.11.1 Environmental impact assessment

- 3.11.2 Social impact & community benefits

- 3.11.3 Governance & corporate responsibility

- 3.11.4 Sustainable finance & investment trends

- 3.12 Electric Two-Wheeler Transition Readiness Index

- 3.12.1 Manufacturing readiness

- 3.12.2 Charging and swapping ecosystem maturity

- 3.12.3 Policy readiness and incentives

- 3.12.4 Consumer acceptance indicators

- 3.13 Dealer & Aftermarket Ecosystem Analysis

- 3.13.1 Dealer network economics and margins

- 3.13.2 Role of service centers and spare parts

- 3.13.3 Aftermarket parts penetration

- 3.13.4 Digital servicing and booking platforms

- 3.13.5 Warranty and extended service trends

- 3.14 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 China

- 4.2.2 India

- 4.2.3 Japan

- 4.2.4 South Korea

- 4.2.5 ANZ

- 4.2.6 Southeast Asia

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Motorcycle

- 5.2.1 Cruiser motorcycles

- 5.2.2 Sport motorcycles

- 5.2.3 Touring motorcycles

- 5.2.4 Standard/naked motorcycles

- 5.2.5 Adventure/dual-sport motorcycles

- 5.2.6 Off-road/dirt motorcycles

- 5.3 Scooter

- 5.3.1 Maxi scooters

- 5.3.2 Moped-style scooters

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

Chapter 7 Market Estimates & Forecast, By Displacement, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Under 250cc

- 7.3 250cc-500cc

- 7.4 500cc-1000cc

- 7.5 Above 1000cc

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Offline

- 8.3 Online

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Personal Use

- 9.3 Commercial

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 China

- 10.3 India

- 10.4 Japan

- 10.5 Australia

- 10.6 South Korea

- 10.7 Singapore

- 10.8 Vietnam

- 10.9 Thailand

- 10.10 Philippines

- 10.11 Malaysia

- 10.12 Indonesia

- 10.13 Rest of Asia Pacific

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Honda

- 11.1.2 Yamaha

- 11.1.3 Suzuki

- 11.1.4 Kawasaki

- 11.1.5 Harley-Davidson

- 11.1.6 BMW Motorrad

- 11.1.7 Ducati

- 11.1.8 KTM

- 11.1.9 Triumph

- 11.1.10 Piaggio

- 11.1.11 Royal Enfield

- 11.1.12 Yadea

- 11.1.13 NIU

- 11.1.14 Gogoro

- 11.2 Regional players

- 11.2.1 Hero

- 11.2.2 Bajaj

- 11.2.3 TVS

- 11.2.4 Kwang Yang

- 11.2.5 Benelli

- 11.2.6 CFMoto

- 11.2.7 Mahindra

- 11.2.8 Jiangmen Dachangjiang

- 11.2.9 Ola Electric

- 11.3 Emerging players

- 11.3.1 Ultraviolette

- 11.3.2 Ather Energy

- 11.3.3 Revolt

- 11.3.4 Okinawa

- 11.3.5 Ampere

- 11.3.6 BGauss

- 11.3.7 Dat Bike