PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959601

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959601

Synchronous Condenser Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

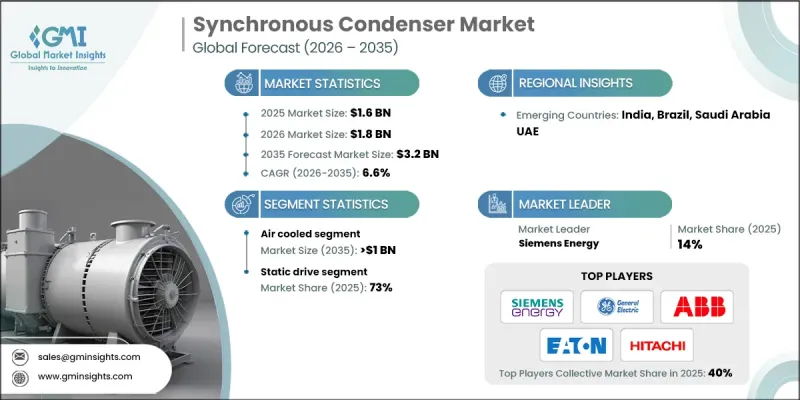

The Global Synchronous Condenser Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 3.2 billion by 2035.

The growth is driven by the retirement of fossil-fuel-based power plants, which traditionally supplied grid inertia and reactive power, leaving a critical gap that synchronous condensers effectively address. Grid modernization initiatives, including smart grid development and high-voltage direct current (HVDC) transmission projects, are accelerating the demand for these devices. Governments and utilities are investing heavily to upgrade aging infrastructure, meet stricter reliability standards, and integrate distributed energy resources. The rapid deployment of wind and solar power introduces variable outputs that can destabilize voltage and frequency. Synchronous condensers provide fast and reliable reactive power support, stabilizing the grid and enhancing power quality. Rising electricity demand, coupled with large-scale investments in renewable energy projects, is further driving the adoption of these systems, as modern grids require advanced solutions to manage intermittent energy sources efficiently.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 6.6% |

The air-cooled segment is expected to reach USD 1 billion by 2035. Air-cooled synchronous condensers are favored for their cost-effectiveness and simpler installation process compared to water- or hydrogen-cooled systems. Their design reduces infrastructure requirements, lowering upfront capital expenditure and operational complexity. This makes them particularly suitable for regions with limited water resources or strict safety regulations. Technological advancements have further improved efficiency and reliability, increasing the adoption of air-cooled systems across industrial and utility applications worldwide.

The static drive segment accounted for 73% share in 2025 and is projected to grow at a CAGR of 6% from 2026 to 2035. Static drives, which leverage power electronic components like thyristors and IGBTs, provide superior efficiency over traditional starting methods. They allow precise control of starting current and torque, minimizing mechanical stress, reducing equipment wear, and ensuring more reliable operation in large-scale electrical networks.

U.S. Synchronous Condenser Market is expected to reach USD 188 million by 2035. Stringent regulations focused on grid reliability and the integration of renewable energy necessitate advanced reactive power compensation devices like synchronous condensers. Industrial growth, including demand from sectors such as oil and gas, further drives adoption. The U.S. also plays a significant role in global trade, where electricity infrastructure investments impact both domestic and international energy markets.

Leading players in the Global Synchronous Condenser Market include ABB, Hitachi Energy Ltd., Toshiba Energy Systems & Solutions Corporation, Mitsubishi Electric Power Products, Inc., Alstom SA, Eaton, Siemens Energy, Doosan, NIDEC Corporation, Bharat Heavy Electricals Limited, Ansaldo Energia, Power Systems & Controls, Inc., BRUSH, Voith GmbH & Co., ANDRITZ, Shanghai Electric, Baker Hughes, and Ingeteam. Companies in the synchronous condenser market are adopting multiple strategies to strengthen their market position. Investment in research and development focuses on enhancing efficiency, reliability, and integration with renewable energy grids. Strategic partnerships with utilities and independent power producers help expand deployment and service networks globally. Firms are developing modular, scalable solutions tailored to industrial, renewable, and grid stabilization applications. Focusing on digital monitoring, predictive maintenance, and remote control capabilities improves operational performance and customer trust.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability landscape

- 3.1.2 Factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Emerging opportunities & trends

- 3.8 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Cooling, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Hydrogen Cooled

- 5.3 Air Cooled

- 5.4 Water Cooled

Chapter 6 Market Size and Forecast, By Starting Method, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Static Drive

- 6.3 Pony motors

- 6.4 Others

Chapter 7 Market Size and Forecast, By End User, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Utility

- 7.3 Industrial

Chapter 8 Market Size and Forecast, By Reactive Power Rating, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 ≤ 100 MVAr

- 8.3 > 100 MVAr to ≤ 200 MVAr

- 8.4 > 200 MVAr

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 Italy

- 9.3.3 France

- 9.3.4 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Alstom SA

- 10.3 ANDRITZ

- 10.4 Ansaldo Energia

- 10.5 Baker Hughes

- 10.6 Bharat Heavy Electricals Limited

- 10.7 BRUSH

- 10.8 Doosan

- 10.9 Eaton

- 10.10 General Electric

- 10.11 Hitachi Energy Ltd.

- 10.12 Ingeteam

- 10.13 Mitsubishi Electric Power Products, Inc.

- 10.14 NIDEC Corporation

- 10.15 Power Systems & Controls, Inc.

- 10.16 Shanghai Electric

- 10.17 Siemens Energy

- 10.18 Toshiba Energy Systems & Solutions Corporation

- 10.19 Voith GmbH & Co.

- 10.20 WEG