PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982266

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982266

Middle East Third-Party Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

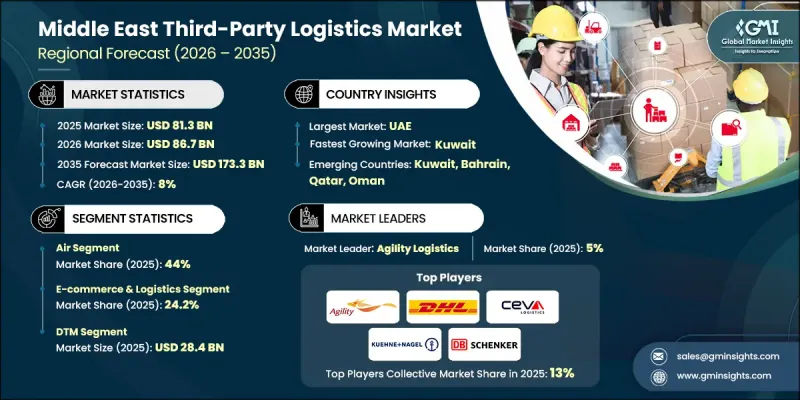

Middle East Third-Party Logistics Market was valued at USD 81.3 billion in 2025 and is estimated to grow at a CAGR of 8% to reach USD 173.3 billion by 2035.

The industry is experiencing sustained structural expansion, supported by large-scale infrastructure investments, expanding trade routes, and accelerating e-commerce activity. Regional governments are positioning logistics as a strategic pillar for economic diversification beyond hydrocarbons, channeling significant capital into transport networks, ports, airports, and digital trade platforms. The UAE and Saudi Arabia continue to serve as primary logistics anchors within the region, benefiting from advanced infrastructure and pro-business policies. The development of integrated supply chain ecosystems is attracting manufacturers, retailers, and cross-border merchants seeking reliable third-party logistics solutions. Growth in online retail, rising consumer expectations for faster fulfillment, and the increasing complexity of regional distribution networks are further strengthening demand for outsourced logistics services. As competition intensifies, scalability, operational efficiency, and technology integration are becoming decisive factors for market leadership across the Middle East 3PL landscape.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $81.3 Billion |

| Forecast Value | $173.3 Billion |

| CAGR | 8% |

The region is expanding special economic zones, bonded storage facilities, multimodal logistics parks, and digital customs frameworks to enhance trade facilitation. The UAE represents the largest third-party logistics market in the Middle East and is supported by major logistics clusters in Abu Dhabi and Dubai. Large-scale facilities equipped with advanced warehousing systems, automation capabilities, and seamless connectivity across air, sea, and land transport are fueling both business-to-business and direct-to-consumer logistics growth. Providers lacking infrastructure depth may struggle to compete as customers increasingly demand speed, scale, and reliability. Ongoing investments in port modernization and transport corridors are further strengthening regional and global trade integration.

The air freight segment accounted for 44% share in 2025 and is projected to grow at a CAGR of 7.1% from 2026 to 2035. Air logistics continues to lead due to the rising volume of high-value, time-sensitive shipments and strong demand for rapid delivery solutions across commercial sectors. Service providers are modernizing cargo management systems, enhancing digital tracking capabilities, and improving operational transparency to deliver faster response times and higher service standards across regional and intercontinental routes.

The e-commerce and logistics segment held 24.2% share in 2025 and is expected to grow at a CAGR of 10% through 2035. Rapid urban expansion, widespread internet adoption, and increasing cross-border transactions are reinforcing the dominance of this segment. Leading providers are investing in automated fulfillment centers, last-mile distribution networks, and real-time shipment visibility platforms to meet evolving customer expectations. E-commerce remains the most strategically significant contributor to regional 3PL revenue and will continue shaping infrastructure upgrades and digital transformation initiatives across GCC markets.

Middle East Third-Party Logistics Market reached USD 39.6 billion in 2025. The country maintains its position as the most advanced and mature 3PL ecosystem in the region, supported by strong trade volumes, expanding online retail, and globally competitive infrastructure. As a critical gateway connecting Asia, Europe, and Africa, the UAE continues to attract multinational logistics providers seeking access to free zones, modern port facilities, and integrated multimodal transport systems.

Key companies operating in the Middle East Third-Party Logistics Market include DHL, Aramex, Kuehne + Nagel, DB Schenker, Agility Logistics, CEVA Logistics, UPS, FedEx, Expeditors International, and Gulf Agency Company. Companies in the Middle East Third-Party Logistics Market are reinforcing their competitive positioning through infrastructure expansion, digital transformation, and strategic partnerships. Major providers are investing in advanced warehouse automation, AI-driven route optimization, and integrated supply chain management platforms to enhance operational efficiency and service reliability. Expansion into free zones and logistics parks is enabling firms to scale capacity and strengthen regional coverage. Strategic alliances with e-commerce platforms and industrial clients are securing long-term contracts and recurring revenue streams. Firms are also prioritizing sustainability initiatives, including fleet electrification and energy-efficient facilities, to align with regional environmental objectives.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Solution

- 2.2.3 Mode

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid e-commerce growth

- 3.2.1.2 Infrastructure investment & connectivity

- 3.2.1.3 Government initiatives & free zones

- 3.2.1.4 Demand for specialized logistics

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Market fragmentation & competition

- 3.2.2.2 Infrastructure bottlenecks

- 3.2.3 Market opportunities

- 3.2.3.1 Technology adoption & digitalization

- 3.2.3.2 Expansion of regional hubs

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technological trends

- 3.3.1.1 Automation & robotics

- 3.3.1.2 AI & machine learning

- 3.3.1.3 Internet of things (IOT)

- 3.3.1.4 Cloud-based supply chain platforms

- 3.3.2 Emerging technologies

- 3.3.2.1 Hyper-connected supply chains

- 3.3.2.2 Robotics-as-a-service (RAAS)

- 3.3.2.3 AI-driven dynamic pricing & capacity management

- 3.3.2.4 Augmented reality (AR) & wearables

- 3.3.1 Current technological trends

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 UAE - UAE Customs, Free Zone & Logistics Licensing Framework for 3PL Operators

- 3.5.2 Turkey - Turkish Transportation of Goods Law & Standard Trading Conditions for Freight and Logistics Services

- 3.5.3 Saudi Arabia - Saudi Transport & Logistics Regulatory Compliance Regime (Transport Law Enforcement & Licensing)

- 3.5.4 Oman - Logistics Services Regulatory Rules, 2022 (Ministry of Transport, Communications & IT)

- 3.5.5 Israel - Israel Ministry of Transport & Road Safety Regulatory Framework (Import/Transport Standards)

- 3.5.6 Qatar - Qatar Maritime Transport Licensing & Shipping Brokerage Regulation (MOT/MTLD 2025)

- 3.5.7 Kuwait - Kuwait Logistics Regulation under Kuwait Port & Municipality Clearance Regime

- 3.5.8 Bahrain - Bahrain National Logistics Strategy & Halal Logistics Regulation (2023)

- 3.5.9 Cyprus - EU Logistics & Transport Regulation (EU Single Market Compliance)

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

- 3.12.1 Regional Infrastructure & Deployment Trends

- 3.12.1.1 Transportation & logistics infrastructure scoring

- 3.12.1.2 Digital & connectivity readiness

- 3.12.1.3 Port, rail & intermodal capacity trends

- 3.12.1.4 Smart logistics hubs & free zones

- 3.12.2 Demand and Supply-Side Assessment

- 3.12.2.1 Supply-Side Analysis

- 3.12.2.1.1 Provider capacity, infrastructure, and capabilities

- 3.12.2.1.2 Technology adoption & operational efficiency

- 3.12.2.1.3 Cost structures and profitability

- 3.12.2.2 Demand-Side Analysis

- 3.12.2.2.1 End-user industry requirements

- 3.12.2.2.2 Volume, frequency, and service-level expectations

- 3.12.2.2.3 Pricing sensitivity and adoption trends

- 3.12.2.1 Supply-Side Analysis

- 3.12.1 Regional Infrastructure & Deployment Trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 UAE

- 4.2.2 Turkey

- 4.2.3 Saudi Arabia

- 4.2.4 Oman

- 4.2.5 Israel

- 4.2.6 Qatar

- 4.2.7 Kuwait

- 4.2.8 Bahrain

- 4.2.9 Cyprus

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Premium positioning strategies

- 4.7 Competitive analysis and USPs

Chapter 5 Market Estimates & Forecast, By Solution, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Dedicated contract carriage (DCC)

- 5.3 Dedicated transportation management (DTM)

- 5.4 International transportation management (ITM)

- 5.5 Warehousing & distribution

- 5.6 Logistics software

Chapter 6 Market Estimates & Forecast, By Mode, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Air

- 6.3 Sea

- 6.4 Rail & Road

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Healthcare

- 7.4 Retail

- 7.5 Automotive

- 7.6 Manufacturing

- 7.7 E-commerce & Logistics

- 7.8 Chemicals & Petrochemicals

- 7.9 Pharmaceuticals

- 7.10 Others

Chapter 8 Market Estimates & Forecast, By Country, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 UAE

- 8.3 Turkey

- 8.4 Saudi Arabia

- 8.5 Oman

- 8.6 Israel

- 8.7 Qatar

- 8.8 Kuwait

- 8.9 Bahrain

- 8.10 Cyprus

- 8.11 Rest of Middle East

Chapter 9 Company Profiles

- 9.1 Global players

- 9.1.1 Bollore Logistics

- 9.1.2 CEVA Logistics

- 9.1.3 DB Schenker

- 9.1.4 DHL

- 9.1.5 DSV (Panalpina)

- 9.1.6 Expeditors International

- 9.1.7 FedEx

- 9.1.8 Kuehne + Nagel

- 9.1.9 Nippon Express

- 9.1.10 UPS

- 9.2 Region players

- 9.2.1 Agility Logistics

- 9.2.2 Al-Falak Logistics

- 9.2.3 Al-Futtaim Logistics

- 9.2.4 Almajdouie Logistics

- 9.2.5 Aramex

- 9.2.6 Gulf Agency Company (GAC)

- 9.3 Emerging players

- 9.3.1 Al-Bahar Logistics

- 9.3.2 Alghanim Industries Logistics

- 9.3.3 Hafeet Logistics

- 9.3.4 Rak Logistics