PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998651

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998651

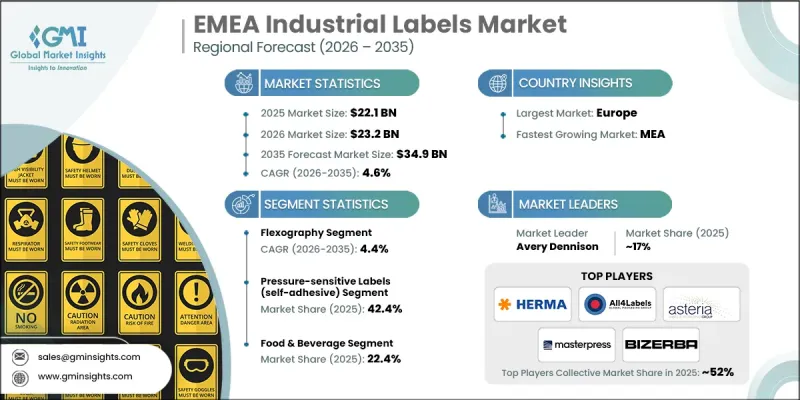

EMEA Industrial Labels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

EMEA Industrial Labels Market was valued at USD 22.1 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 34.9 billion by 2035.

A major factor supporting the expansion of the EMEA industrial labels market is the implementation of strict product identification and safety labeling regulations across multiple countries in the region. Regulatory authorities require manufacturers to ensure that products carry precise identification details and safety information across packaging and operational materials. These requirements have increased the need for durable labeling solutions capable of maintaining clarity and readability even after prolonged exposure to challenging industrial environments. Compliance frameworks also emphasize the importance of traceability systems that allow manufacturers to monitor the movement of goods throughout the supply chain. As regulatory monitoring activities and compliance assessments become more frequent, organizations are increasingly investing in certified and standardized labeling solutions. Additionally, cross-border trade across the region requires labeling that aligns with diverse regional regulatory requirements, which has increased operational complexity for manufacturers. Companies must therefore prioritize high-quality labeling solutions that meet strict compliance criteria, as regulatory non-compliance can lead to financial penalties, operational disruption, and reputational risk. As a result, industrial producers often collaborate with specialized labeling providers to ensure full compliance with evolving regulatory frameworks.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $22.1 Billion |

| Forecast Value | $34.9 Billion |

| CAGR | 4.6% |

The flexography printing segment generated USD 7.95 billion in 2025 and is projected to grow at a CAGR of 4.4% between 2026 and 2035. Flexographic printing has established a strong position in the EMEA industrial labels market due to its ability to deliver high-speed production and cost-efficient operations. The technology supports large-scale printing requirements while maintaining consistent output quality and clear visual results. Its adaptability across multiple labeling materials increases its usefulness across various industrial applications. Long operational life of printing components further reduces production costs over extended manufacturing cycles. The technology also supports strict labeling standards required across multiple regulated industries. In addition, fast setup processes and the ability to scale production efficiently make flexography well-suited for large-volume industrial labeling operations, reinforcing its widespread adoption across packaging and manufacturing sectors.

The pressure-sensitive labels segment held 42.4% share and is expected to grow at a CAGR of 3.9% from 2026 to 2035. These labels have gained significant popularity due to their simple application process and reliable adhesion across various surfaces. The self-adhesive design enables quick placement without the need for additional equipment or complex installation procedures. Strong resistance to environmental factors such as temperature variations, moisture, and chemical exposure enhances their durability in industrial settings. Compatibility with multiple printing technologies further supports customization and design flexibility, enabling manufacturers to adjust labeling formats according to operational needs. In addition, efficient application helps reduce labor requirements and improves productivity along industrial production lines.

Germany Industrial Labels Market reached USD 3.2 billion in 2025 and is projected to grow at a CAGR of 4.2% from 2026 to 2035. The country's strong industrial base continues to support consistent demand for advanced labeling solutions. Manufacturing sectors require reliable labeling systems to support product identification, operational efficiency, and supply chain visibility. Regulatory requirements across several industries are also encouraging the adoption of certified labeling materials that meet strict compliance standards. Expansion of automated logistics operations and modern warehouse infrastructure is further increasing demand for advanced labeling technologies that support inventory tracking and operational transparency. At the same time, growing awareness of environmental sustainability is encouraging companies to adopt recyclable and environmentally responsible labeling materials. Ongoing technological innovation is also supporting the adoption of automated and digital labeling systems designed to enhance efficiency and production accuracy.

Prominent companies participating in the EMEA Industrial Labels Market include Avery Dennison, HERMA GmbH, All4Labels Global Packaging Group, Asteria Group, Masterpress S.A., Schafer Etiketten GmbH, Nordic Label Oy, Uhler & Schaar GmbH & Co. KG, Labelcraft Ltd., Eurografica S.p.A., Etiketten Stierli AG, CS Labels Ltd., Euro Labels AG, MD Labels, and Etisoft Group. Companies operating within the EMEA Industrial Labels Market are adopting a range of strategic initiatives to strengthen their competitive position and expand their regional presence. Many manufacturers are increasing investment in research and development to create advanced labeling materials that deliver higher durability, improved print quality, and stronger compliance with regulatory requirements. Product innovation also focuses on developing environmentally sustainable labeling solutions that align with evolving environmental standards. Businesses are strengthening partnerships with industrial manufacturers and packaging companies to expand long-term supply agreements and distribution networks. In addition, companies are adopting advanced printing technologies and automation systems to enhance production efficiency and reduce operational costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regions

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regions

- 2.2.2 Product Type

- 2.2.3 Material

- 2.2.4 Mechanism

- 2.2.5 Printing Technology

- 2.2.6 End Use Industry

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of manufacturing and industrial operations

- 3.2.1.2 Rising adoption of RFID and smart label technologies

- 3.2.1.3 Stringent regulatory and compliance requirements

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Raw material cost volatility

- 3.2.2.2 Complex and fragmented regulatory environment

- 3.2.3 Opportunities

- 3.2.3.1 Anti-counterfeit and security labeling technologies

- 3.2.3.2 Sustainable and eco-friendly labeling materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS Code - 4821)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Regions

- 4.2.1.1 Europe

- 4.2.1.2 MEA

- 4.2.1 By Regions

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Warning & Security Labels

- 5.3 Branding Labels

- 5.4 Tracking & Logistics Labels

- 5.5 Identification Labels

- 5.6 Regulatory & Compliance Labels

- 5.7 Smart Labels

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Metal Labels

- 6.3 Plastic & Polymer Labels

- 6.4 Paper Labels

- 6.5 Sustainable & Recyclable Materials

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Mechanism, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Pressure-Sensitive Labels (Self-Adhesive)

- 7.3 Glue-Applied Labels (Wet-Glued)

- 7.4 Heat Transfer Labels

- 7.5 In-Mold Labels (IML)

- 7.6 Sleeve Labels (Shrink & Stretch)

- 7.7 Multi-Part Tracking Labels

- 7.8 Linerless Labels

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Printing Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Digital Printing

- 8.3 Flexography

- 8.4 Lithography & Offset Printing

- 8.5 Screen Printing

- 8.6 Gravure Printing

- 8.7 Letterpress Printing

- 8.8 Laser Marking & Coding

- 8.9 Thermal Transfer Printing

- 8.10 Hybrid Printing Technologies

- 8.11 Others

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Transportation & Logistics

- 9.3 Automotive Industry

- 9.4 Healthcare & Pharmaceuticals

- 9.5 Food & Beverage

- 9.6 Electronics & Consumer Goods

- 9.7 Chemicals & Industrial Manufacturing

- 9.8 Personal Care & Cosmetics

- 9.9 Retail & E-Commerce

- 9.10 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.1.1 Europe

- 10.1.1.1 Germany

- 10.1.1.2 UK

- 10.1.1.3 France

- 10.1.1.4 Italy

- 10.1.1.5 Spain

- 10.1.1.6 Netherlands

- 10.1.1.7 Turkey

- 10.1.1.8 Russia

- 10.1.1.9 Nordic Countries

- 10.1.1.10 Rest of Europe

- 10.1.2 MEA

- 10.1.2.1 Saudi Arabia

- 10.1.2.2 UAE

- 10.1.2.3 South Africa

- 10.1.1 Europe

Chapter 11 Company Profiles

- 11.1 All4Labels Global Packaging Group

- 11.2 Asteria Group

- 11.3 Avery Dennison

- 11.4 CS Labels Ltd.

- 11.5 Etiketten Stierli AG

- 11.6 Etisoft Group

- 11.7 Euro Labels AG

- 11.8 Eurografica S.p.A.

- 11.9 HERMA GmbH

- 11.10 Labelcraft Ltd.

- 11.11 Masterpress S.A.

- 11.12 MD Labels

- 11.13 Nordic Label Oy

- 11.14 Schafer Etiketten GmbH

- 11.15 Uhler & Schaar GmbH & Co. KG