PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998652

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998652

Europe Passenger Electric Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

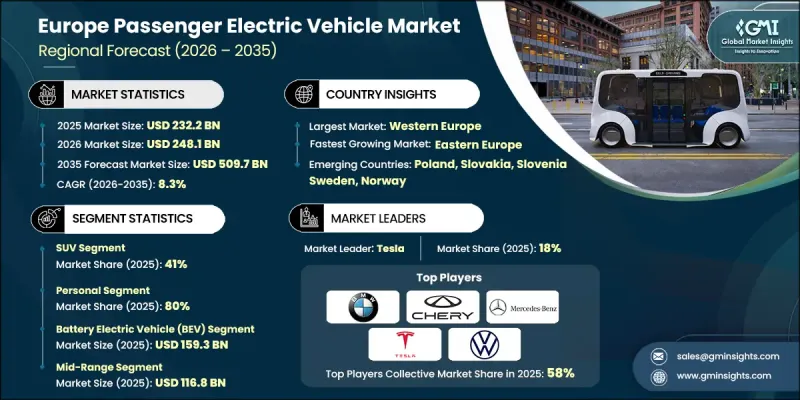

Europe Passenger Electric Vehicle Market was valued at USD 232.2 billion in 2025 and is estimated to grow at a CAGR of 8.3% to reach USD 509.7 billion by 2035.

Europe currently represents one of the most mature and rapidly evolving regions for passenger electric mobility due to comprehensive climate policies and ambitious emissions reduction objectives established by regional governments. Stringent carbon emission limits for passenger vehicles, commercial fleets, and public transportation systems are encouraging a widespread transition toward electrified mobility solutions. Governments across the region have also introduced national strategies aimed at accelerating the adoption of electric vehicles through regulatory support, infrastructure development, and consumer incentives. What initially began as strong early adoption within certain European countries has now evolved into widespread acceptance across multiple major automotive markets throughout the region. The expansion of charging infrastructure, rising environmental awareness among consumers, and improvements in battery technology have further strengthened the momentum of electric mobility. In addition, automotive manufacturers are accelerating the electrification of their vehicle portfolios, investing heavily in battery innovation and large-scale production capabilities. These combined factors continue to shape a competitive and technologically advanced environment for passenger electric vehicles throughout Europe.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $232.2 Billion |

| Forecast Value | $509.7 Billion |

| CAGR | 8.3% |

Automotive manufacturers across Europe are increasing their commitments to electric vehicle production by expanding manufacturing capacity and investing in battery technology development. Companies are focusing on improving battery efficiency, extending driving range, and lowering production costs in order to make electric vehicles more competitive with traditional combustion engine vehicles. These initiatives are also intensifying competition among automakers as they race to strengthen their positions within the rapidly expanding electric mobility landscape. In Western Europe, electric vehicle registrations have reached unprecedented levels in recent years. This growth is supported by the availability of a wider selection of competitively priced electric vehicle models targeted at mainstream consumers. In addition, continued expansion of public charging networks across urban areas and transportation corridors is improving accessibility and convenience for electric vehicle owners.

The SUV segment held a 41% share in 2025, and the segment is expected to grow at a CAGR of 9.6% between 2026 and 2035. Sport utility vehicles continue to dominate the passenger vehicle category because they combine spacious design, advanced features, and strong consumer appeal. As demand increases, vehicle manufacturers are prioritizing the development of electric SUVs due to their strong profit margins and popularity among buyers. This growing preference is encouraging automakers to allocate significant resources toward the electrification of larger passenger vehicles. Manufacturers are investing in production facilities, upgrading assembly systems, and strengthening battery manufacturing capabilities to support the rising demand for electric SUVs across European markets.

The personal passenger electric vehicle segment accounted for 80% share in 2025 and is projected to grow at a CAGR of 7.7% from 2026 to 2035. Demand for electric vehicles among individual consumers continues to rise steadily as battery electric vehicles become more integrated into everyday transportation. Increasing environmental awareness, improved driving range capabilities, and enhanced charging infrastructure are encouraging more consumers to adopt electric vehicles for personal use. Additionally, supportive government policies and financial incentives in several European countries are helping reduce the upfront purchase costs associated with electric vehicles, making them more accessible to a wider consumer base and accelerating adoption among private vehicle owners.

Germany Passenger Electric Vehicle Market generated USD 62.1 billion in 2025. The country's leadership position is supported by strong policy initiatives, a well-established automotive manufacturing ecosystem, and high consumer awareness regarding electric mobility. Germany hosts numerous global automotive manufacturers and maintains a strong industrial base dedicated to electric vehicle development and production. Government support programs designed to encourage electric vehicle adoption have also played a significant role in driving market growth. Financial incentives aimed at supporting households purchasing new electric vehicles have helped lower the cost barrier for consumers, encouraging broader participation in the Europe passenger electric vehicle market and strengthening Germany's position as a central hub for electric mobility within Europe.

Key companies operating in the Europe Passenger Electric Vehicle Market include Tesla, BMW, Volkswagen, Audi, Renault, Ford, Volvo, Skoda, Mercedes-Benz, and Chery. Companies participating in the Europe Passenger Electric Vehicle Market are adopting multiple strategic initiatives to strengthen their competitive positions and expand market presence. Automotive manufacturers are heavily investing in research and development to improve battery performance, extend driving range, and enhance vehicle efficiency. Many companies are expanding electric vehicle production capacity through new manufacturing facilities and advanced assembly technologies to meet rising demand. Strategic partnerships with battery suppliers and technology firms are also becoming increasingly common as companies aim to accelerate innovation and reduce production costs. In addition, automakers are focusing on expanding their electric vehicle portfolios across multiple vehicle categories to attract a broader consumer base. Continuous investment in charging infrastructure collaborations, digital connectivity features, and sustainable manufacturing practices further supports long term growth and competitiveness in the Europe passenger electric vehicle market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Drive

- 2.2.3 Propulsion

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 Price

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Battery Manufacturer

- 3.1.1.2 Component Supplier

- 3.1.1.3 OEM (Original Equipment Manufacturer)

- 3.1.1.4 Distributor / Dealer

- 3.1.1. 5 End user

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Accelerates EV adoption, pressures OEMs to electrify fleets.

- 3.2.1.2 Improves convenience, reduces range anxiety, boosts sales.

- 3.2.1.3 Lowers vehicle prices improve affordability

- 3.2.1.4 Rapid adoption potential in underpenetrated markets.

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Slows large-scale charging deployment in some regions.

- 3.2.2.2 High upfront cost

- 3.2.3 Market opportunities

- 3.2.3.1 Premium EV segment expansion

- 3.2.3.2 Local battery production & supply chain development

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.2 Emerging technologies

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 Western Europe

- 3.5.2 Eastern Europe

- 3.5.3 Northern Europe

- 3.5.4 Southern Europe

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.1.1 Predictive Maintenance & Operations Optimization

- 3.13.1.2 Automated design optimization

- 3.13.1.3 Supply chain AI for demand forecasting

- 3.13.1.4 GenAI use cases & adoption roadmap by segment

- 3.13.1.4.1 Tread pattern design generation

- 3.13.1.4.2 Customer service chatbots & technical support

- 3.13.1.4.3 Marketing content creation

- 3.13.1.4.4 Risks, limitations & regulatory considerations

- 3.13.1.4.4.1 Data privacy in IoT-enabled smart products

- 3.13.1.4.4.2 AI algorithm transparency requirements

- 3.13.1.4.4.3 Liability in AI-driven product failures

- 3.13.1 AI-driven disruption of existing business models

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Western Europe

- 4.2.2 Eastern Europe

- 4.2.3 Northern Europe

- 4.2.4 Southern Europe

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Hatchback

- 5.3 Sedan

- 5.4 SUV

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Drive , 2022 - 2035 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Front-wheel drive

- 6.3 Rear-wheel drive

- 6.4 All-wheel drive

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($ Bn, Units)

- 7.1 Key trends

- 7.2 Battery Electric Vehicle (BEV)

- 7.3 Fuel Cell Electric Vehicle (FCEV)

- 7.4 Plug-in Hybrid Electric Vehicle (PHEV)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($ Bn, Units)

- 8.1 Key trends

- 8.2 Personal

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast By Price, 2022 - 2035 ($ Bn, Units)

- 9.1 Key trends

- 9.2 Entry

- 9.3 Mid-Range

- 9.4 Luxury

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn, Units)

- 10.1 Key trends

- 10.2 Western Europe

- 10.2.1 Germany

- 10.2.2 France

- 10.2.3 Netherlands

- 10.2.4 Belgium

- 10.2.5 Switzerland

- 10.2.6 Austria

- 10.2.7 Ireland

- 10.2.8 Luxembourg

- 10.3 Eastern Europe

- 10.3.1 Poland

- 10.3.2 Czech Republic

- 10.3.3 Portugal

- 10.3.4 Serbia

- 10.3.5 Albania

- 10.3.6 Slovakia

- 10.3.7 Romania

- 10.4 Northern Europe

- 10.4.1 UK

- 10.4.2 Denmark

- 10.4.3 Sweden

- 10.4.4 Norway

- 10.4.5 Iceland

- 10.4.6 Faroe Islands

- 10.5 Southern Europe

- 10.5.1 Italy

- 10.5.2 Spain

- 10.5.3 Vatican City

- 10.5.4 San Marino

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Tesla

- 11.1.2 Volkswagen

- 11.1.3 BMW

- 11.1.4 Mercedes-Benz

- 11.1.5 Hyundai

- 11.1.6 Kia

- 11.1.7 Ford

- 11.1.8 Volvo

- 11.1.9 Renault

- 11.1.10 Stellantis

- 11.2 Regional players

- 11.2.1 Škoda

- 11.2.2 Audi

- 11.2.3 Cupra

- 11.2.4 Opel

- 11.2.5 Aehra

- 11.2.6 Rimac Automobili

- 11.3 Emerging players

- 11.3.1 BYD

- 11.3.2 Polestar

- 11.3.3 MG Motor

- 11.3.4 Nissan