PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998676

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998676

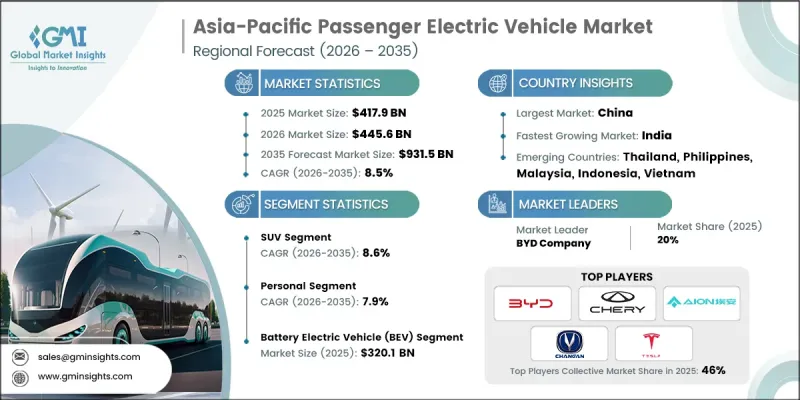

Asia-Pacific Passenger Electric Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

Asia-Pacific Passenger Electric Vehicle Market was valued at USD 417.9 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 931.5 billion by 2035.

The Asia-Pacific passenger electric vehicle market continues to evolve rapidly as governments across the region implement supportive policies aimed at accelerating the transition toward low-emission transportation systems. Public initiatives designed to encourage clean mobility are strengthening the adoption of passenger electric vehicles and supporting long-term industry growth. Continuous improvements in battery technology have also played a vital role in enhancing the performance and efficiency of electric vehicles. Higher energy density and longer driving capabilities have made electric vehicles more practical and appealing to a broader consumer base. In addition, the global health crisis created both temporary challenges and long-term opportunities for the industry. Initial manufacturing interruptions and supply chain disruptions slowed vehicle production in the early stages of the pandemic. However, the situation also reinforced the importance of sustainable mobility and encouraged governments to incorporate green transportation policies into economic recovery plans. As a result, policy support, technological advancement, and growing consumer awareness of environmental sustainability are collectively strengthening the growth outlook for the Asia-Pacific passenger electric vehicle market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $417.9 Billion |

| Forecast Value | $931.5 Billion |

| CAGR | 8.5% |

Across the Asia-Pacific region, several major economies continue to play a significant role in shaping the development of the Asia-Pacific passenger electric vehicle market. China has emerged as the largest contributor to market expansion, supported by its vast population base and ongoing urban development initiatives. Meanwhile, the Asia-Pacific passenger electric vehicle market in India is witnessing notable growth as government programs designed to promote cleaner transportation gain traction. Increasing environmental awareness among consumers and steady technological improvements are encouraging greater adoption of electric vehicles throughout the country. Public sector initiatives aimed at expanding the electric mobility ecosystem are also supporting long-term development of the passenger electric vehicle industry across India and the wider Asia-Pacific region.

The SUV segment accounted for 57% share in 2025 and is anticipated to grow at a CAGR of 8.6% from 2026 to 2035. Demand for electric sport utility vehicles continues to increase as manufacturers introduce models designed to combine driving performance, extended travel capability, and competitive pricing. Within the Asia-Pacific region, automotive companies are placing strong emphasis on developing vehicles that meet the lifestyle needs of both urban and suburban consumers. As consumer preferences increasingly favor larger vehicles that offer comfort, space, and advanced technologies, the electric SUV segment continues to gain strong market traction. Automakers are also focusing on introducing regionally tailored features and improved energy efficiency to enhance the appeal of these vehicles across diverse markets.

The personal vehicle segment held an 80% share and is expected to grow at a CAGR of 7.9% between 2026 and 2035. Growing environmental awareness among individuals and the desire to reduce long-term transportation costs are encouraging more consumers to adopt electric vehicles for personal mobility. Increased domestic manufacturing, competitive pricing strategies, and improved charging infrastructure are helping expand accessibility for a wider group of consumers. In addition, automakers are continuously integrating advanced digital systems, improved battery capacity, and intelligent connectivity features to enhance the ownership experience. These innovations are strengthening consumer confidence and encouraging greater adoption of personal electric vehicles across the Asia-Pacific region.

China Passenger Electric Vehicle Market generated USD 284.9 billion in 2025. The rapid expansion of the Chinese electric vehicle ecosystem has played a central role in shaping the broader regional market. Strong consumer demand, continuous policy support, and intense competition among domestic and international manufacturers are driving innovation and large-scale production within the country. The competitive environment has encouraged companies to develop vehicles that combine advanced technologies with cost-effective pricing strategies. As manufacturers work to meet growing consumer demand while improving product capabilities, China continues to influence the pace of innovation and expansion across the Asia-Pacific passenger electric vehicle market.

Key companies operating in the Asia-Pacific Passenger Electric Vehicle Market include Tesla, BYD, SAIC Motor, Geely, Changan, Wuling, XPeng Motors, Kia, Chery, and GAC Aion. Companies participating in the Asia-Pacific Passenger Electric Vehicle Market are implementing several strategic initiatives to strengthen their market presence and expand their competitive advantage. Automakers are heavily investing in research and development to enhance battery performance, extend driving range, and improve overall vehicle efficiency. Expanding localized manufacturing capabilities is another important strategy, allowing companies to reduce production costs while meeting regional demand more effectively. Strategic collaborations with technology providers and battery manufacturers are also helping companies accelerate innovation and strengthen supply chain resilience. Many manufacturers are introducing diverse vehicle portfolios that cater to different consumer segments and price ranges. Additionally, businesses are focusing on improving charging infrastructure partnerships and digital connectivity features to enhance the overall customer experience and increase long-term adoption of passenger electric vehicles across the Asia-Pacific region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Drive

- 2.2.3 Propulsion

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 Price

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Battery Manufacturer

- 3.1.1.2 Component Supplier

- 3.1.1.3 OEM (Original Equipment Manufacturer)

- 3.1.1.4 Distributor / Dealer

- 3.1.1. 5 End user

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Aggressive government incentives & policy mandates

- 3.2.1.2 rapid expansion of charging infrastructure

- 3.2.1.3 declining battery costs & localized supply chains

- 3.2.1.4 urban pollution & fuel cost pressure

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High upfront vehicle cost in emerging

- 3.2.2.2 Uneven infrastructure outside Tier-1 cities

- 3.2.3 Market opportunities

- 3.2.3.1 Premium EV segment expansion

- 3.2.3.2 Local battery production & supply chain development

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Battery localization & vertical integration expansion

- 3.3.2 Affordable small EV & urban mobility segment growth

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 China - New Energy Vehicle (NEV) Dual-Credit Policy

- 3.5.2 India - Faster Adoption and Manufacturing of Electric Vehicles (FAME) Scheme

- 3.5.3 Japan - Green Growth Strategy (GGS)

- 3.5.4 South Korea - Electric Vehicle Subsidy and Incentive Program

- 3.5.5 Australia - New Vehicle Efficiency Standard (NVES)

- 3.5.6 New Zealand - Clean Car Standard (CCS)

- 3.5.7 Taiwan - Electric Vehicle Promotion Policy

- 3.5.8 Indonesia - Government Regulation No. 74 of 2021 on Low-Carbon Emission Vehicles

- 3.5.9 Thailand - EV 3.5 Policy

- 3.5.10 Singapore - Early Turnover Scheme (ETS) and Green Vehicle Rebate (GVR)

- 3.5.11 Philippines - Electric Vehicle Industry Development Act (EVIDA)

- 3.5.12 Vietnam - Resolution No. 98/2023 on EV Registration Fee Exemption

- 3.5.13 Malaysia - Low Carbon Mobility Blueprint (LCMB) 2021-2030

- 3.5.14 Myanmar - National Electromobility Policy Framework (Early Development Stage)

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.11 Trade Data Analysis (Driven by Paid Database)

- 3.11.1 Import/Export Volume & Value Trends

- 3.11.2 Key Trade Corridors & Tariff Impact

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Impact of AI & generative AI on the market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.1.1 Predictive Maintenance & Operations Optimization

- 3.13.1.2 Automated design optimization

- 3.13.1.3 Supply chain AI for demand forecasting

- 3.13.1.4 GenAI use cases & adoption roadmap by segment

- 3.13.1.4.1 Tread pattern design generation

- 3.13.1.4.2 Customer service chatbots & technical support

- 3.13.1.4.3 Marketing content creation

- 3.13.1.4.4 Risks, limitations & regulatory considerations

- 3.13.1.4.4.1 Data privacy in IoT-enabled smart products

- 3.13.1.4.4.2 AI algorithm transparency requirements

- 3.13.1.4.4.3 Liability in AI-driven product failures

- 3.13.1 AI-driven disruption of existing business models

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 China

- 4.2.2 India

- 4.2.3 Japan

- 4.2.4 South Korea

- 4.2.5 Australia

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Hatchback

- 5.3 Sedan

- 5.4 SUV

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Drive , 2022 - 2035 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Front-wheel drive

- 6.3 Rear-wheel drive

- 6.4 All-wheel drive

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($ Bn, Units)

- 7.1 Key trends

- 7.2 Battery Electric Vehicle (BEV)

- 7.3 Fuel Cell Electric Vehicle (FCEV)

- 7.4 Plug-in Hybrid Electric Vehicle (PHEV)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($ Bn, Units)

- 8.1 Key trends

- 8.2 Personal

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast By Price, 2022 - 2035 ($ Bn, Units)

- 9.1 Key trends

- 9.2 Entry

- 9.3 Mid-Range

- 9.4 Luxury

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn, Units)

- 10.1 Key trends

- 10.2 China

- 10.3 India

- 10.4 Japan

- 10.5 South Korea

- 10.6 Australia

- 10.7 New Zealand

- 10.8 Taiwan

- 10.9 Indonesia

- 10.10 Thailand

- 10.11 Singapore

- 10.12 Philippines

- 10.13 Vietnam

- 10.14 Malaysia

- 10.15 Myanmar

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 BYD Auto

- 11.1.2 Geely Automobile

- 11.1.3 Hyundai Motor

- 11.1.4 Kia

- 11.1.5 Li Auto

- 11.1.6 Nissan Motor

- 11.1.7 SAIC Motor

- 11.1.8 Tesla

- 11.1.9 Toyota Motor

- 11.1.10 XPeng Motors

- 11.2 Regional players

- 11.2.1 Aion

- 11.2.2 Changan

- 11.2.3 Honda Motor

- 11.2.4 Mahindra Electric Mobility

- 11.2.5 Maruti Suzuki India

- 11.2.6 Mitsubishi Motors

- 11.2.7 Tata Motors

- 11.2.8 Wuling

- 11.3 Emerging players

- 11.3.1 BAIC Motor (BJEV)

- 11.3.2 Chery Automobile

- 11.3.3 VinFast