PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998792

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998792

Chickpeas Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

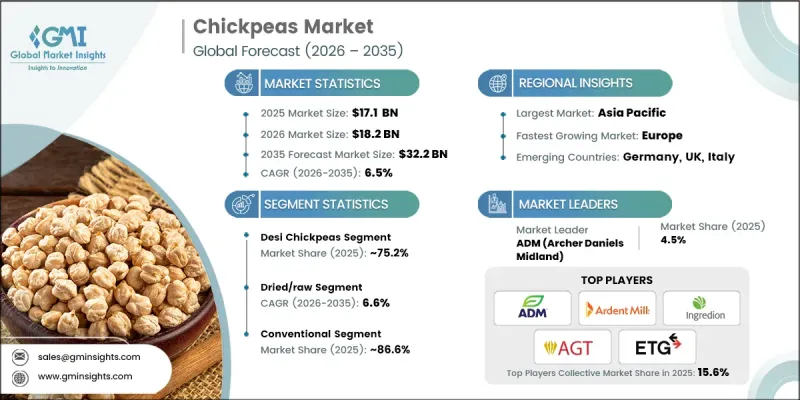

The Global Chickpeas Market was valued at USD 17.1 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 32.2 billion by 2035.

Chickpeas, also known as garbanzo beans, are widely recognized for their nutritional profile, offering protein, fiber, vitamins, and essential minerals. The increasing global focus on plant-based diets, along with rising awareness of the health benefits of chickpeas, is driving market growth. Consumers are seeking protein-rich, gluten-free, and non-GMO foods, boosting demand for chickpeas as a natural, versatile ingredient. Vegetarian, vegan, and flexitarian diets have gained significant traction, further increasing the consumption of chickpeas in various forms. The market growth is also fueled by the demand for chickpeas in processed foods, snacks, and other plant-based products, making them an integral part of modern dietary patterns. Sustainable farming practices and investment in storage and processing infrastructure are helping maintain quality, availability, and long-term growth of the industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.1 Billion |

| Forecast Value | $32.2 Billion |

| CAGR | 6.5% |

The dried and raw chickpeas segment held a 70.5% share in 2025 and is expected to grow at a CAGR of 6.6% between 2026 and 2035. This segment benefits from consumer preference for minimally processed, natural ingredients. Dried chickpeas are versatile and allow consumers to cook meals at home while maintaining a protein-rich and fiber-filled diet. Farmers and suppliers are increasingly adopting sustainable cultivation methods and building modern processing and storage facilities to ensure consistent quality and supply.

The conventional chickpeas segment accounted for 86.6% share in 2025 and is projected to grow at a CAGR of 6.6% through 2035. Their cost-effectiveness and widespread availability make them the preferred choice for consumers seeking budget-friendly options. Conventional chickpeas are commonly used in processed foods such as flours, snacks, and ready-to-eat meals. Meanwhile, organic chickpeas are gaining traction as consumer interest in health-conscious, sustainable, and certified organic products grows. Both conventional and organic segments are essential to meet the diverse needs of the market.

North America Chickpeas Market accounted for 7.1% share in 2025. The region is experiencing growth driven by rising awareness of plant-based nutrition, increasing demand for chickpea-based snacks, gluten-free products, and healthy food alternatives. The established food processing and retail sectors support market expansion, while product innovation and distribution network growth continue to strengthen market presence. Vegan and vegetarian dietary trends, along with convenient, nutritious offerings, are further bolstering market adoption across the U.S. and Canada.

Key players operating in the Global Chickpeas Market include Agrocorp Processing Australia, Bean Growers Australia, Diefenbaker Spice & Pulse (DSP), MT Royal, ETG Group, ADM (Archer Daniels Midland), Ingredion Incorporated, Vad Industries, Superior Pulses, Ardent Mills, Avena Foods, Nutriati Inc., and AGT Food & Ingredients Inc. Companies in the Global Chickpeas Market are adopting strategies to strengthen their position by investing in modern processing and storage facilities, expanding distribution networks, and improving supply chain efficiency. Product innovation, including ready-to-cook, ready-to-eat, and fortified chickpea offerings, helps cater to evolving consumer preferences. Firms are emphasizing sustainable and certified farming practices to appeal to environmentally conscious buyers. Strategic partnerships with retailers, food service providers, and international distributors allow for broader market reach and recurring demand. Companies are also focusing on marketing campaigns highlighting health benefits, protein content, and dietary versatility to reinforce brand presence and encourage adoption among plant-based consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Form

- 2.2.3 Nature

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.2.6 End user

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Kabuli chickpeas

- 5.3 Desi chickpeas

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dried/raw

- 6.3 Flour & powder

- 6.4 Ready-to-eat products

Chapter 7 Market Estimates and Forecast, By Nature, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Conventional

- 7.3 Organic

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverages

- 8.2.1 Home cooking/traditional meals

- 8.2.2 Ready meals & prepared foods

- 8.2.3 Bakery & confectionery

- 8.2.4 Snacks & savories

- 8.2.5 Plant-based protein products

- 8.2.6 Others

- 8.3 Animal feed

- 8.4 Nutraceuticals

- 8.5 Industrial

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Wholesale & direct sales

- 9.3 Supermarkets & hypermarkets

- 9.4 Specialty stores

- 9.5 Online retail

- 9.6 Convenience stores

Chapter 10 Market Estimates and Forecast, By End User, 2022-2035 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Food processors & manufacturers

- 10.3 Household/retail consumers

- 10.4 Food service operators

- 10.5 Institutional buyers

Chapter 11 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 ADM (Archer Daniels Midland)

- 12.2 Agrocorp Processing Australia

- 12.3 AGT Food & Ingredients Inc.

- 12.4 Ardent Mills

- 12.5 Avena Foods

- 12.6 Bean Growers Australia

- 12.7 Diefenbaker Spice & Pulse (DSP)

- 12.8 ETG Group

- 12.9 Grain Processing Corporation (GPC)

- 12.10 Ingredion Incorporated

- 12.11 MT Royal

- 12.12 Nutriati Inc.

- 12.13 Superior Pulses

- 12.14 Vad Industries