PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998797

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998797

North America Carpet and Rug Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

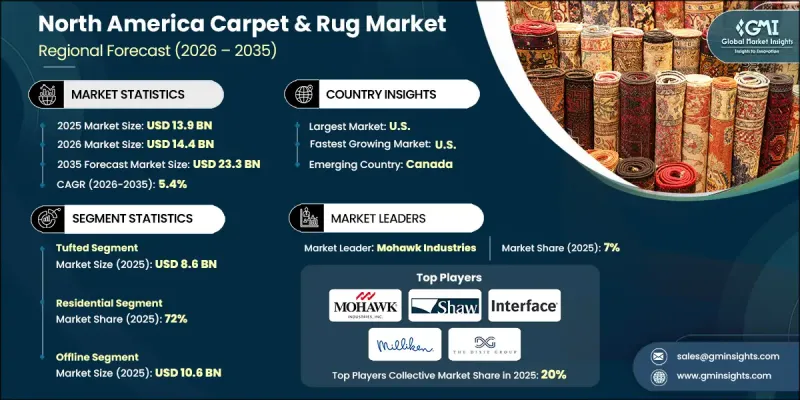

North America Carpet & Rug Market was valued at USD 13.9 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 23.3 billion by 2035.

Market expansion is supported by sustained growth in residential remodeling and interior upgrades, as homeowners increasingly prioritize visual appeal, comfort, and functionality. Textile flooring solutions are widely recognized as an accessible way to transform interior spaces without extensive structural modifications. Greater exposure to digital design platforms and simplified installation methods has accelerated consumer interest in carpets and area rugs. These products allow households to refresh living environments efficiently while reflecting personal style preferences. Rising consumer inclination toward customized interiors is further encouraging purchases, as buyers seek flooring options that align with evolving lifestyle needs. In addition, improvements in manufacturing techniques have expanded choices in textures, patterns, and materials, strengthening product appeal. As homeowners continue investing in property enhancement, carpets and rugs remain integral components of interior design strategies across the region.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.9 Billion |

| Forecast Value | $23.3 Billion |

| CAGR | 5.4% |

The expansion of remote and hybrid work arrangements has further stimulated demand for flooring solutions that enhance comfort and indoor acoustics. As residential spaces are adapted for multipurpose use, consumers are selecting carpeting and rugs to create quieter, warmer, and more comfortable environments. Textile flooring contributes to sound reduction, thermal insulation, and overall underfoot comfort, making it a practical choice for modern living requirements. These lifestyle adjustments are reinforcing the importance of carpets and rugs in renovation decisions across diverse consumer segments.

The tufted products segment accounted for USD 8.6 billion in 2025. Their popularity is driven by cost-effectiveness, production efficiency, and design flexibility. The tufting process enables manufacturers to deliver a broad range of textures, pile variations, and aesthetic styles at competitive price points, appealing to a wide customer base. These products provide an upscale appearance comparable to more intricate constructions while maintaining affordability. The balance of value, availability, and visual versatility positions tufted carpets and rugs as a leading flooring choice across income groups.

The offline distribution channels segment generated USD 10.6 billion in 2025. Physical retail outlets remain essential because many consumers prefer to evaluate texture, craftsmanship, and color accuracy in person before making significant flooring investments. Brick-and-mortar stores offer hands-on interaction, personalized guidance, and professional consultation, which strengthens buyer confidence. The ability to provide expert recommendations and installation advice continues to make offline retail a dominant sales avenue, particularly for long-lasting flooring products.

United States North America Carpet & Rug Market accounted for 75% share in 2025, generating USD 10.4 billion. Strong consumer purchasing power, recurring renovation cycles, and a mature retail infrastructure contribute to national market leadership. Ongoing interior refresh trends support consistent demand for both broadloom carpeting and area rugs. Diverse housing styles across the country create varied product requirements, encouraging manufacturers to offer extensive selections in textures, constructions, and performance features. Despite rising interest in alternative flooring materials, consumer preference for comfort in residential living spaces sustains steady demand for carpet and rug solutions.

Major companies operating in the North America Carpet & Rug Market include Mohawk Industries, Shaw Industries Group, Interface, Milliken & Company, The Dixie Group, Bentley Mills, Engineered Floors, Nourison, Oriental Weavers, Stanton Carpet, Stark Carpet, J&J Flooring, Masland Carpets, Marquis Industries, and Couristan. Companies in the North America Carpet & Rug Market are strengthening their competitive position through product innovation, sustainable manufacturing, and omnichannel expansion. Leading players are investing in advanced fiber technologies and eco-friendly materials to meet the rising demand for durable and environmentally responsible flooring. Strategic partnerships with designers and builders are expanding project-based sales opportunities. Manufacturers are also enhancing customization capabilities to address evolving aesthetic preferences. Digital visualization tools and e-commerce integration are improving customer engagement while complementing traditional retail networks.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 Price

- 2.2.5 End use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Strong home renovation & remodeling activity

- 3.2.1.2 Urbanization & residential construction

- 3.2.1.3 Increasing interest in sustainable textiles

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Maintenance concerns & allergies

- 3.2.2.2 Volatile raw material prices

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of sustainable & natural fiber rugs

- 3.2.3.2 Premium & custom-designed segments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By country

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By country

- 4.2.1.1 U.S.

- 4.2.1.2 Canada

- 4.2.1 By country

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Million Square Meters)

- 5.1 Key trends

- 5.2 Woven

- 5.3 Tufted

- 5.4 Knotted

- 5.5 Needle-punched

- 5.6 Flat weave

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion) (Million Square Meters)

- 6.1 Key trends

- 6.2 Nylon

- 6.3 Wool

- 6.4 Silk

- 6.5 Polyester

- 6.6 Acrylic

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Price, 2022 - 2035 (USD Billion) (Million Square Meters)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Billion) (Million Square Meters)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Million Square Meters)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Company websites

- 9.3 Offline

- 9.3.1 Supermarket/hypermarket

- 9.3.2 Specialty stores

- 9.3.3 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Million Square Meters)

- 10.1 Key trends

- 10.2 U.S.

- 10.3 Canada

Chapter 11 Company Profiles

- 11.1 Bentley Mills

- 11.2 Couristan

- 11.3 Engineered Floors

- 11.4 Interface

- 11.5 J&J Flooring

- 11.6 Marquis Industries

- 11.7 Masland Carpets

- 11.8 Milliken & Company

- 11.9 Mohawk Industries

- 11.10 Nourison

- 11.11 Oriental Weavers

- 11.12 Shaw Industries Group

- 11.13 Stanton Carpet

- 11.14 Stark Carpet

- 11.15 The Dixie Group