PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998804

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998804

Folding Carton Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

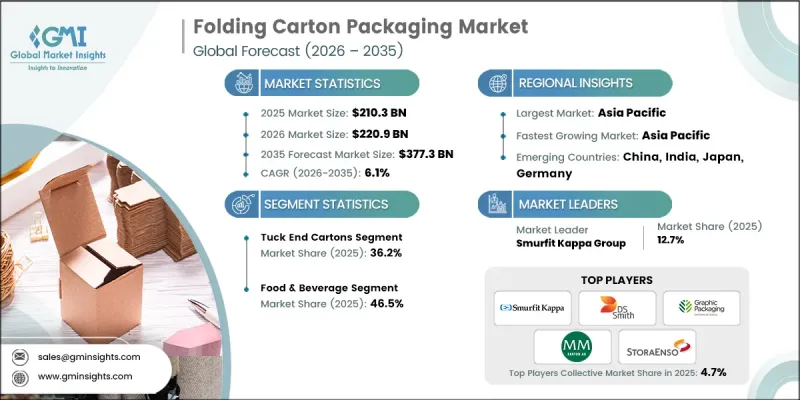

The Global Folding Carton Packaging Market was valued at USD 210.3 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 377.3 billion by 2035.

Growth in the folding carton packaging market is largely driven by the global transition toward sustainable packaging materials and the increasing adoption of recyclable fiber-based solutions. Governments and regulatory authorities across many regions are introducing stricter packaging regulations aimed at reducing environmental impact and encouraging circular economy practices. These policies are accelerating the shift away from rigid plastic packaging toward paperboard-based alternatives that offer recyclability and lower environmental footprints. In addition, the rapid growth of e-commerce and modern retail distribution channels has created a stronger demand for secondary packaging formats that protect products while maintaining strong branding visibility. Industries such as pharmaceuticals, healthcare, cosmetics, and personal care are also increasing their reliance on high-quality folding cartons to meet packaging safety requirements and regulatory standards. At the same time, brands are placing greater emphasis on premium packaging designs that enhance product appeal and strengthen brand identity. These evolving requirements, combined with continuous technological improvements in carton manufacturing and printing processes, continue to support long-term expansion of the global folding carton packaging market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $210.3 Billion |

| Forecast Value | $377.3 Billion |

| CAGR | 6.1% |

The folding carton packaging market is also influenced by strong regulatory momentum encouraging companies to adopt recyclable fiber-based packaging solutions. Governments and environmental organizations are implementing stricter waste management policies and sustainability targets that require manufacturers to reduce packaging waste and improve recyclability. As a result, many industries are shifting toward lightweight paperboard cartons that offer both environmental benefits and efficient material utilization. This approach allows companies to optimize packaging structures while lowering overall material consumption. Rising costs of raw materials and increased focus on carbon footprint reporting are further motivating organizations to improve packaging efficiency and reduce environmental impact.

The display-ready cartons segment is projected to grow at a CAGR of 8.6% during 2026-2035, reflecting strong demand across modern retail environments. These packaging formats are gaining popularity because they simplify product handling and merchandising processes within retail stores. Display-ready cartons allow products to be transported and presented on retail shelves using a single packaging structure, which improves operational efficiency for retailers and reduces labor requirements during product stocking. Retailers and consumer goods companies increasingly prefer packaging formats that combine logistical efficiency with strong visual presentation. As organized retail continues to expand and consumer competition intensifies across store environments, the demand for display-ready carton packaging solutions is expected to increase steadily.

The coated recycled paperboard (CRB) segment reached USD 69.9 billion in 2025. This material remains widely used due to its cost efficiency and high recycled fiber content, making it an attractive option for companies seeking environmentally responsible packaging solutions. CRB offers reliable structural performance for various packaging applications where a premium visual appearance is not a primary requirement. Increasing regulatory pressure to incorporate higher levels of recycled materials into packaging products has strengthened the adoption of CRB across multiple industries. Companies aiming to enhance their sustainability performance while maintaining cost control often prioritize recycled paperboard materials, which continues to support the leading position of this segment within the folding carton packaging market.

North America Folding Carton Packaging Market accounted for 29.1% share in 2025. The industry in this region continues to expand due to strict environmental regulations and growing demand for recyclable packaging materials across several consumer industries. Businesses operating in North America are increasingly adopting paperboard-based packaging solutions as alternatives to conventional plastic packaging. In addition, retailers are encouraging suppliers to transition toward recyclable packaging formats that align with sustainability commitments. The region has also seen increasing investment in advanced manufacturing technologies designed to improve carton converting efficiency and support higher levels of product customization.

Key companies operating in the Global Folding Carton Packaging Market include Graphic Packaging International, DS Smith Plc, Smurfit Kappa Group, Stora Enso Oyj, Mayr-Melnhof Karton AG, Huhtamaki Oyj, Georgia-Pacific LLC, Oji Holdings Corporation, Rengo Co., Ltd., Green Bay Packaging Inc., American Carton Company, Diamond Packaging, Meyers, Schur Pack Germany GmbH, August Faller GmbH & Co. KG, Seaboard Folding Box Company Inc., Wynalda Packaging, All Packaging Company, and Plastech Group Ltd. Companies active in the Global Folding Carton Packaging Market are implementing several strategic initiatives to strengthen their competitive position and expand their market presence. Many organizations are investing in advanced converting technologies and automated production lines to improve manufacturing efficiency and reduce operational costs. Expanding sustainable packaging portfolios has become a major priority, with companies developing recyclable and lightweight paperboard materials that align with environmental regulations. Strategic partnerships with consumer goods brands and retail companies allow packaging manufacturers to create customized solutions that meet evolving product packaging requirements. Businesses are also increasing investments in digital printing and design technologies to offer flexible packaging customization and faster product launches.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Carton structure trends

- 2.2.2 Paperboard grade trends

- 2.2.3 Printing technology trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Regulatory push toward fiber-based recyclable packaging

- 3.2.1.2 Growth of e-commerce secondary packaging demand

- 3.2.1.3 Shift from plastic clamshells to paperboard cartons

- 3.2.1.4 Pharmaceutical serialization and compliance requirements

- 3.2.1.5 Premiumization in cosmetics and personal care cartons

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in virgin pulp and paperboard prices

- 3.2.2.2 High capital costs for advanced die-cutting equipment

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of barrier-coated recyclable paperboard

- 3.2.3.2 Smart packaging integration with QR/NFC features

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Trade Data Analysis (Based on Paid Databases)

- 3.13.1 Import/Export Volume & Value Trends

- 3.13.2 Key Trade Corridors & Tariff Impact

- 3.14 Impact of AI & Generative AI on the Market

- 3.14.1 AI-Driven Disruption of Existing Business Models

- 3.14.2 GenAI Use Cases & Adoption Roadmap by Segment

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Carton Structure, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Tuck end cartons

- 5.3 Auto-lock / crash bottom cartons

- 5.4 Sleeve cartons

- 5.5 Lock-bottom cartons

- 5.6 Display-ready cartons

- 5.7 Other folding structures

Chapter 6 Market Estimates and Forecast, By Paperboard Grade, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Solid bleached sulfate (SBS)

- 6.3 Coated unbleached kraft (CUK)

- 6.4 Coated recycled paperboard (CRB)

- 6.5 Uncoated paperboard

Chapter 7 Market Estimates and Forecast, By Printing Technology, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Offset lithography

- 7.3 Flexographic printing

- 7.4 Digital printing

- 7.5 Gravure

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.3 Personal care & cosmetics

- 8.4 Pharmaceuticals & healthcare

- 8.5 Household & consumer goods

- 8.6 Tobacco

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 DS Smith Plc

- 10.1.2 Graphic Packaging International

- 10.1.3 Huhtamaki Oyj

- 10.1.4 Mayr-Melnhof Karton AG

- 10.1.5 Oji Holdings Corporation

- 10.1.6 Rengo Co., Ltd.

- 10.1.7 Smurfit Kappa Group

- 10.1.8 Stora Enso Oyj

- 10.2 Regional key players

- 10.2.1 North America

- 10.2.1.1 All Packaging Company

- 10.2.1.2 American Carton Company

- 10.2.1.3 Diamond Packaging

- 10.2.1.4 Georgia-Pacific LLC

- 10.2.1.5 Green Bay Packaging Inc.

- 10.2.1.6 Meyers

- 10.2.1.7 Seaboard Folding Box Company Inc.

- 10.2.1.8 Wynalda Packaging

- 10.2.2 Asia Pacific

- 10.2.2.1 Plastech Group Ltd.

- 10.2.3 Europe

- 10.2.3.1 Schur Pack Germany GmbH

- 10.2.1 North America

- 10.3 Niche Players/Disruptors

- 10.3.1 August Faller GmbH & Co. KG