PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019209

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019209

North America Energy as a Service (EaaS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

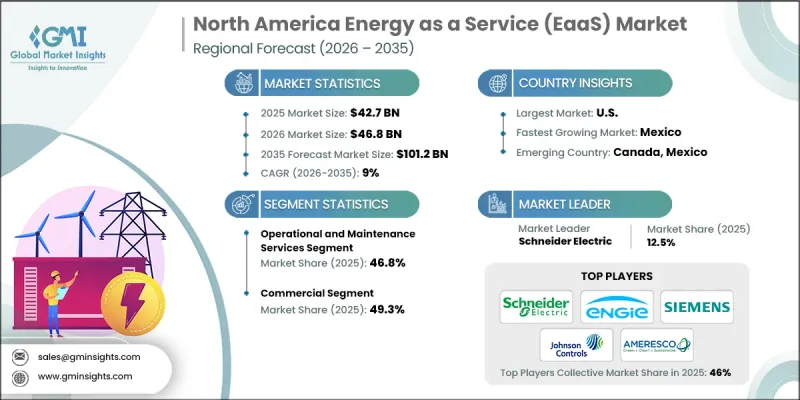

North America Energy as a Service (EaaS) Market was valued at USD 42.7 billion in 2025 and is estimated to grow at a CAGR of 9% to reach USD 101.2 billion by 2035.

Businesses are increasingly moving away from owning and managing energy systems, opting for service-based models that handle procurement, maintenance, and performance upgrades. This approach allows organizations to focus on core operations while minimizing upfront costs and leveraging the expertise of experienced operators. Pressure to manage long-term energy expenses, ensure operational resilience against grid instability, and meet sustainability goals is driving widespread EaaS adoption. The proliferation of smart meters, on-site generation, and remote monitoring has made these services more practical for commercial and industrial users. Companies can now rely on EaaS providers to integrate rooftop solar, battery storage, and analytics into a cohesive solution, reflecting a larger shift toward flexible, distributed, and technology-enabled energy systems that improve efficiency while reducing operational risk.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $42.7 Billion |

| Forecast Value | $101.2 Billion |

| CAGR | 9% |

The energy efficiency and optimization services segment is anticipated to grow at a CAGR of 9.5% by 2035. Increasing state-level efficiency requirements, updated building codes, performance standards, and decarbonization policies are prompting organizations to adopt services that optimize HVAC systems, lighting, and overall load management. Businesses are leveraging external experts to meet compliance standards, reduce energy waste, and upgrade legacy facilities without expanding internal engineering resources. The growing adoption of digital tools across the energy grid further fuels demand for optimization services that improve forecasting, reliability, and operational efficiency.

The residential segment is expected to grow at a CAGR of 9.6% through 2035, driven by the need for intelligent home energy management. Homeowners are seeking predictable costs, remote control of energy systems, and reduced dependence on aging infrastructure. Demand flexibility programs and dynamic rate participation are also supporting growth, helping households better manage peak energy consumption.

U.S. Energy as a Service (EaaS) Market is projected to reach USD 86 billion by 2035, propelled by stricter environmental regulations, renewable energy mandates, and increasing interest in sustainable energy solutions. Extreme weather events have highlighted vulnerabilities in traditional energy infrastructure, accelerating investments in resilient, technology-enabled systems. Canada is also witnessing rising adoption as organizations focus on energy efficiency and cost reduction, further supporting North American market growth.

Key players operating in the North America Energy as a Service (EaaS) Market include Schneider Electric, Siemens AG, ABB Ltd, Enel X, Ameresco, Inc., Johnson Controls, ENGIE, Edison Energy, Centrica Business Solutions, Honeywell International Inc., OpTerra Energy Services, Noresco LLC, METRUS ENERGY, REDAPTIVE, SOLMICROGRID, Unison Energy, Energy Systems Group, Budderfly, and Bernhard Energy Solutions. Companies in the North America Energy as a Service (EaaS) Market are strengthening their presence by expanding their service portfolios to include integrated energy solutions such as solar, storage, and smart analytics. They focus on forming strategic partnerships with commercial, industrial, and residential clients to increase adoption and long-term contracts. Investments in advanced digital platforms for real-time monitoring and predictive maintenance enhance customer satisfaction and operational reliability. Firms also leverage government incentives and sustainability programs to drive market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Type trends

- 2.4 End use trends

- 2.5 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Technology provider

- 3.1.2 Equipment manufacturers

- 3.1.3 Digital solution providers

- 3.1.4 Financial enablers

- 3.1.5 Policy & regulatory bodies

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization & IoT integration

- 3.7.2 Emerging market penetration

- 3.8 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2025

- 4.2.1 U.S.

- 4.2.2 Canada

- 4.2.3 Mexico

- 4.3 Competitive benchmarking

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Energy supply service

- 5.3 Operational and maintenance services

- 5.4 Energy efficiency and optimization services

Chapter 6 Market Size and Forecast, By End use, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

- 6.5 Utility

Chapter 7 Market Size and Forecast, By Country, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 U.S.

- 7.3 Canada

- 7.4 Mexico

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Ameresco, Inc.

- 8.3 Bernhard Energy Solutions

- 8.4 Budderfly

- 8.5 Centrica Business Solutions

- 8.6 Edison Energy

- 8.7 Enel X

- 8.8 Energy Systems Group

- 8.9 ENGIE

- 8.10 Honeywell International Inc

- 8.11 Johnson Controls

- 8.12 METRUS ENERGY

- 8.13 Noresco LLC

- 8.14 OpTerra Energy Services

- 8.15 REDAPTIVE

- 8.16 Schneider Electric

- 8.17 Siemens AG

- 8.18 SOLMICROGRID

- 8.19 Unison Energy

- 8.20 VEREGY