PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019220

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019220

Zirconia-based Dental Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

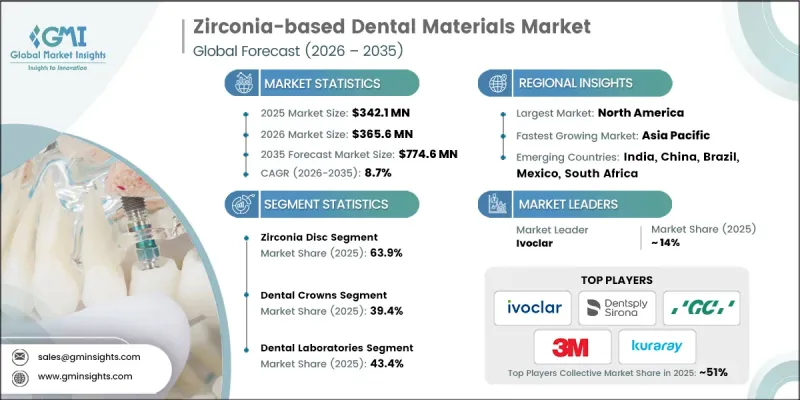

The Global Zirconia-based Dental Materials Market was valued at USD 342.1 million in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 774.6 million by 2035.

Market growth is fueled by rising demand for aesthetic, long-lasting dental restorations, increasing prevalence of dental disorders and tooth loss, and technological advancements in digital dentistry and CAD/CAM systems. Zirconia-based materials are prized for their mechanical strength, durability, and biocompatibility, making them suitable for crowns, bridges, implants, and other restorative applications. The adoption of CAD/CAM workflows enhances precision, reduces chairside time, and improves laboratory efficiency, further encouraging zirconia use. Innovations such as multi-layered, high-translucency zirconia and the shift toward monolithic restorations are expanding applications. The growing trend of chairside milling and same-day dentistry is also driving global adoption of zirconia-based dental materials, reinforcing their status as a preferred option for modern dental practices worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $342.1 Million |

| Forecast Value | $774.6 Million |

| CAGR | 8.7% |

The zirconia discs segment held a 63.9% share in 2025, owing to their seamless integration with CAD/CAM milling systems and high efficiency in fabricating crowns, bridges, and implant restorations. These discs are engineered to meet the precision demands of modern digital dentistry, allowing dental laboratories to achieve superior fit and finish while minimizing errors and material waste. Their uniform density and customizable sizes enable consistent milling results, supporting both standard and complex restorative cases. Additionally, zirconia discs are compatible with a wide range of digital scanners and milling machines, making them versatile for clinics and labs of all sizes.

The dental crowns segment accounted for 39.4% share in 2025 and is projected to reach USD 298.2 million, fueled by the growing preference for zirconia crowns in restoring damaged, discolored, or weakened teeth. Zirconia crowns are highly favored due to their exceptional structural strength, resistance to wear, and natural tooth-like aesthetics, which provide patients with long-lasting and visually appealing restorations. The segment's growth is further supported by increasing patient awareness and demand for cosmetic dental solutions, as well as dentists' focus on minimizing replacement frequency through durable materials.

North America Zirconia-based Dental Materials Market captured 38.9% share in 2025. The region benefits from advanced dental care infrastructure, widespread use of intraoral scanners, and CAD/CAM systems that enable precise fabrication of crowns, bridges, and implants. Frequent upgrades in dental clinics and laboratories, coupled with continuous product launches and clinical training programs, support the adoption of zirconia restorations. Leading dental material manufacturers and distributors actively promote zirconia products, ensuring strong market penetration.

Key players in the Global Zirconia-based Dental Materials Market include 3M, Aidite, Argen, B&D Dental Technologies, Dental Direkt, Dentsply Sirona, GC International, Henry Schein, HUGE Dental, Ivoclar, KURARAY, Pritidenta, Straumann Holding, Upcera, and VITA Zahnfabrik. To strengthen their market foothold, companies are expanding their product portfolios with multi-layered, high-translucency zirconia and monolithic restoration solutions to meet diverse clinical needs. Strategic investments in research and development enhance material performance, aesthetic quality, and milling compatibility. Collaborations with dental laboratories and universities support training programs that increase clinician adoption. Market participants are also focusing on digital dentistry integration, providing chairside milling systems and CAD/CAM-compatible discs. Geographic expansion, targeted marketing campaigns, and partnerships with distributors further improve supply chain reach. Innovation in faster milling techniques, same-day dentistry solutions, and aesthetic customization helps companies differentiate their offerings, increase client loyalty, and sustain long-term growth in the zirconia based dental materials market.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for aesthetic and tooth-colored dental restorations

- 3.2.1.2 Increasing prevalence of dental disorders and tooth loss

- 3.2.1.3 Advancements in CAD/CAM and digital dentistry technologies

- 3.2.1.4 Increasing adoption of metal-free restorative dentistry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of zirconia materials and processing equipment

- 3.2.2.2 Competition from alternative dental materials such as lithium disilicate

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of digital dentistry and chairside CAD/CAM systems

- 3.2.3.2 Development of highly translucent and multilayer zirconia materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Customer insights (Driven by primary research)

- 3.10 Start-up scenarios (Driven by primary research)

- 3.11 Impact of AI and its future assessment

- 3.12 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Zirconia disc

- 5.3 Zirconia blocks

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Dental crowns

- 6.3 Dental bridges

- 6.4 Dentures

- 6.5 Dental implants

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Dental laboratories

- 7.3 Dental clinics

- 7.4 Academic and research institutes

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M

- 9.2 Aidite

- 9.3 Argen

- 9.4 B&D Dental Technologies

- 9.5 Dental Direkt

- 9.6 Dentsply Sirona

- 9.7 GC International

- 9.8 Henry Schein

- 9.9 HUGE Dental

- 9.10 Ivoclar

- 9.11 KURARAY

- 9.12 pritidenta

- 9.13 Straumann Holding

- 9.14 Upcera

- 9.15 VITA Zahnfabrik