PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019243

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019243

Smart Vehicle Architecture Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

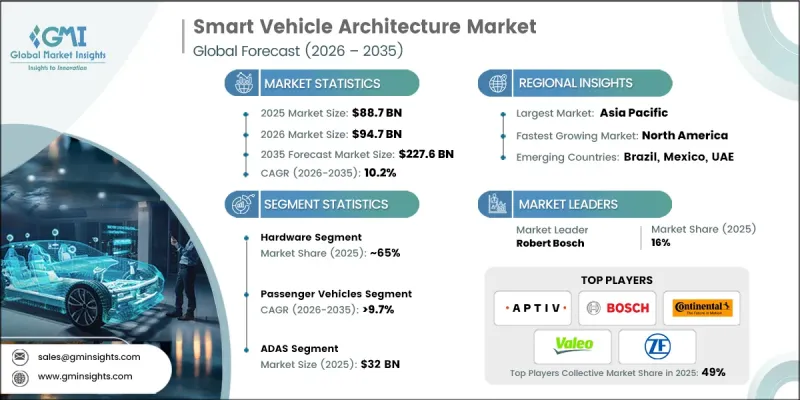

The Global Smart Vehicle Architecture Market was valued at USD 88.7 billion in 2025 and is estimated to grow at a CAGR of 10.2% to reach USD 227.6 billion by 2035.

The robust growth is fueled by the accelerating adoption of electric vehicles, the rising integration of advanced driver-assistance systems (ADAS), and the increasing demand for software-defined vehicles and connected mobility solutions. Automakers and technology providers are heavily investing in centralized and zonal E/E architectures to support high-performance computing, over-the-air software updates, and seamless integration of autonomous and connected vehicle features. Expanding EV platforms, intelligent cockpit systems, and next-generation telematics are driving the need for modular, scalable vehicle architectures. OEMs and mobility providers are under growing pressure to reduce vehicle complexity, optimize wiring harnesses, strengthen cybersecurity, and enable faster feature deployment, which is prompting a shift from conventional distributed architectures to domain and zonal-based systems. Innovations such as high-performance computing units, AI-integrated processors, automotive Ethernet networks, service-oriented architectures, and middleware layers are transforming traditional E/E systems, improving efficiency, lowering latency, and enabling continuous software upgrades across the vehicle lifecycle.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $88.7 Billion |

| Forecast Value | $227.6 Billion |

| CAGR | 10.2% |

The hardware segment held a 65% share in 2025 and is expected to grow at a CAGR of 10% from 2026 to 2035. Hardware remains central to smart vehicle architecture, as components like high-performance computing units, AI-enabled management modules, and domain controllers actively manage vehicle electronics, data flow, and system integration. These components are critical for real-time data processing, low-latency communication, and the integration of ADAS, infotainment, and powertrain systems in passenger vehicles, commercial EVs, and autonomous mobility platforms globally.

The passenger vehicles segment accounted for 76% share in 2025 and is projected to grow at a CAGR of 9.7% during 2026-2035. Passenger vehicle adoption of electric, hybrid, and autonomous vehicles is driving demand for centralized and zonal architectures, high-performance computing, and AI-enabled modules. Rising consumer expectations for software-defined features, advanced connectivity, and seamless ADAS and infotainment integration are accelerating deployment. OEMs are standardizing scalable, modular, and software-centric architectures across economy, mid-size, and premium passenger EVs, reinforcing the segment's market dominance in Europe, North America, and Asia Pacific.

China Smart Vehicle Architecture Market held 55% share, generating USD 19.6 billion in 2025. Growth in China is supported by strong EV production, rapid electrification initiatives, and the presence of leading automotive OEMs, semiconductor providers, and technology developers. High EV penetration, expanding production of software-defined and connected vehicles, and supportive government policies drive demand for advanced smart vehicle architecture solutions, including domain controllers, centralized and zonal computing platforms, AI-enabled management systems, ADAS modules, and high-speed automotive Ethernet networks across passenger EVs, commercial EVs, and autonomous mobility platforms.

Key players in the Global Smart Vehicle Architecture Market include Aptiv PLC, Continental AG, Delphi Technologies, Harman International, Infineon Technologies, Mahle, Qualcomm Technologies, Robert Bosch, Valeo, and ZF Friedrichshafen AG. Companies in the Smart Vehicle Architecture Market strengthen their position by investing in next-generation computing platforms, developing AI-enabled domain controllers, and expanding automotive Ethernet networks. They focus on partnerships with OEMs and tech providers to integrate autonomous, connected, and software-defined vehicle features. Firms are standardizing modular, scalable architectures to support multiple vehicle platforms, enhancing R&D for cybersecurity, OTA software updates, and real-time data processing. Expansion into emerging EV markets, acquisitions of specialized tech firms, and collaboration with telematics and infotainment providers further enhance market presence, improve operational efficiency, and ensure a competitive advantage in both passenger and commercial vehicle segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Architecture

- 2.2.5 Technology layer

- 2.2.6 Propulsion

- 2.2.7 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid Electrification of Vehicles

- 3.2.1.2 Rise of Software-Defined Vehicles

- 3.2.1.3 Growing ADAS & Autonomous Integration

- 3.2.1.4 Demand for Reduced Vehicle Complexity & Weight

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Development & Integration Costs

- 3.2.2.2 Cybersecurity & Data Privacy Risks

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of Centralized & Zonal Architectures

- 3.2.3.2 Integration of AI & Edge Computing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA, CARB, NHTSA Standards

- 3.4.1.2 Canada: Transport Canada, CMVSS Regulation

- 3.4.2 Europe

- 3.4.2.1 Germany: BMDV, Euro 6/7

- 3.4.2.2 France: Ministry of Transport, Euro 6/7

- 3.4.2.3 UK: Department for Transport, Euro 6/7

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport

- 3.4.3 Asia Pacific

- 3.4.3.1 China: MIIT, China 6/7 Standards

- 3.4.3.2 Japan: MLIT, JIS Regulations

- 3.4.3.3 South Korea: MOLIT, KS Standards

- 3.4.3.4 India: MoRTH, BS6 Norms

- 3.4.4 Latin America

- 3.4.4.1 Brazil: DENATRAN, CONAMA Standards

- 3.4.4.2 Mexico: Ministry of Communications & Transport

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: RTA, ESMA Regulations

- 3.4.5.2 Saudi Arabia: Ministry of Transport, SASO

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.12.1 Base Case - Key Macro & Industry Variables Driving CAGR

- 3.12.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.12.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company Tier Benchmarking

- 4.6.1 Tier Classification Criteria & Qualifying Thresholds

- 4.6.2 Tier Positioning Matrix by Revenue, Geography & Innovation

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Centralized computing units

- 5.2.2 Adas modules

- 5.2.3 Vehicle communication interfaces

- 5.2.4 Power distribution units (PDUS)

- 5.2.5 Smart sensors & actuators

- 5.3 Software

- 5.3.1 Embedded vehicle software

- 5.3.2 Cloud-based vehicle software

- 5.3.3 Cybersecurity solutions

- 5.3.4 Over-the-air (OTA) update systems

- 5.3.5 Vehicle operating systems

- 5.4 Services

- 5.4.1 Vehicle diagnostics & maintenance services

- 5.4.2 Connected vehicle data services

- 5.4.3 Software-as-a-service (SAAS) for automotive

- 5.4.4 Remote monitoring & fleet management services

- 5.4.5 Integration & customization services

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCV)

- 6.3.2 Medium commercial vehicles (MCV)

- 6.3.3 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Architecture, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Centralized Architectures

- 7.2.1 Domain Controllers

- 7.2.2 Central Computing Platforms

- 7.3 Zonal Architectures

- 7.3.1 Zone Controllers

- 7.3.2 Gateway Modules

- 7.4 Modular Platforms

- 7.4.1 Scalable Hardware Platforms

- 7.4.2 Software-Defined Modules

- 7.5 Distributed Architectures

- 7.5.1 Traditional ECU Networks

- 7.5.2 Point-to-Point Communication Systems

Chapter 8 Market Estimates & Forecast, By Technology Layer, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 ADAS

- 8.3 Infotainment & Connectivity

- 8.4 Over-the-Air (OTA) Updates

- 8.5 Cybersecurity Solutions

- 8.6 AI & Machine Learning

Chapter 9 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 ICE

- 9.2.1 Gasoline

- 9.2.2 Diesel

- 9.2.3 Hybrid

- 9.3 EV (Electric Vehicles)

- 9.3.1 BEV (Battery Electric Vehicle)

- 9.3.2 PHEV (Plug-in Hybrid Electric Vehicle)

- 9.3.3 FCEV (Fuel Cell Electric Vehicle)

Chapter 10 Market Estimates & Forecast, By End-Use, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 Automotive OEMs

- 10.3 Tier 1 & Tier 2 Suppliers

- 10.4 Autonomous Vehicle Developers

- 10.5 Fleet Management Companies

- 10.6 Mobility Service Providers

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Belgium

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 Singapore

- 11.4.6 South Korea

- 11.4.7 Vietnam

- 11.4.8 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Global Player

- 12.1.1 Aptiv PLC

- 12.1.2 Continental AG

- 12.1.3 Delphi Technologies

- 12.1.4 Harman International

- 12.1.5 Infineon Technologies

- 12.1.6 Mahle

- 12.1.7 Qualcomm Technologies

- 12.1.8 Robert Bosch

- 12.1.9 Valeo

- 12.1.10 ZF Friedrichshafen AG

- 12.2 Regional Player

- 12.2.1 Aisin Seiki

- 12.2.2 Autoliv

- 12.2.3 BorgWarner

- 12.2.4 Dana

- 12.2.5 Denso

- 12.2.6 Hanon Systems

- 12.2.7 Hitachi Astemo

- 12.2.8 Lear Corporation

- 12.2.9 Magneti Marelli

- 12.2.10 NXP Semiconductors