PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027494

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027494

Liquid Hydrogen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

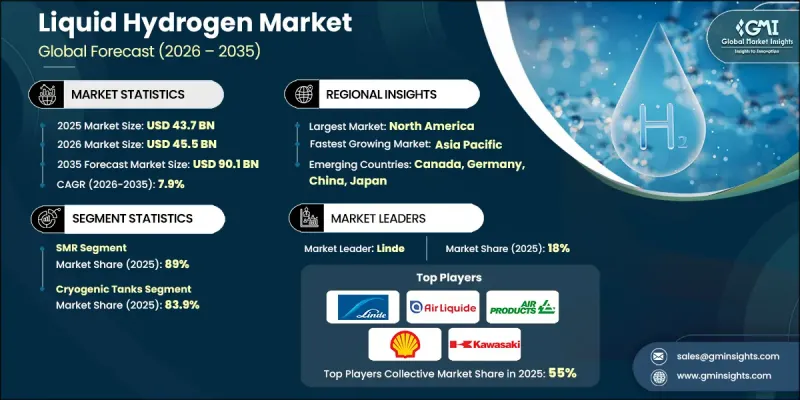

The Global Liquid Hydrogen Market was valued at USD 43.7 billion in 2025 and is estimated to grow at a CAGR of 7.9% to reach USD 90.1 billion by 2035.

Market expansion is supported by the emergence of hydrogen hubs that enable centralized production, storage, and distribution, thereby improving operational efficiency and accelerating adoption across industries. Increasing emphasis on decarbonization targets, along with the growing implementation of hydrogen-focused strategies across major economies, is further strengthening demand. Industry participants are actively deploying hydrogen solutions across transportation, industrial operations, and energy systems while simultaneously expanding infrastructure and making long-term strategic investments. Advancements in hydrogen technologies and increasing collaboration among technology providers and energy companies are shaping the competitive landscape. At the same time, cross-border partnerships and global alliances are enhancing supply chain integration and accelerating infrastructure development. Rising public-private collaborations and strategic investments are further supporting industry expansion. Progress in liquefaction and cryogenic storage technologies is improving scalability and deployment efficiency. In addition, evolving production methods, including steam methane reforming, coal-based processes, and electrolysis, are enhancing supply capabilities. These developments, combined with regulatory incentives, cost optimization strategies, and the integration of cleaner feedstocks and carbon capture technologies, are contributing to lower emissions and broader market adoption.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $43.7 Billion |

| Forecast Value | $90.1 Billion |

| CAGR | 7.9% |

The steam methane reforming segment accounted for 89% share in 2025 and is expected to grow at a CAGR of 7.5% through 2035. Increasing focus on expanding and upgrading production facilities is driving the growth of this segment. The development of large-scale production plants to meet rising hydrogen demand across industries is gaining momentum, while the integration of carbon capture technologies is improving environmental performance. The recognition of hydrogen as a key energy carrier is further encouraging the adoption of this production method as part of long-term energy transition strategies.

The pipeline segment is anticipated to grow at a CAGR of 8.5% by 2035. Expanding hydrogen infrastructure networks, supported by interconnected industrial facilities and multiple end users, are driving segment growth. These distribution systems are enhancing supply efficiency within defined regions while supporting large-scale deployment. Increasing attention to safety standards and regulatory frameworks, along with continuous technological improvements, is strengthening the reliability and performance of hydrogen transportation systems. The need to manage hydrogen under specialized conditions is also encouraging innovation in pipeline design and operational practices.

United States Liquid Hydrogen Market held a share of 77.5% in 2025, generating USD 16.7 billion. Market growth in the country is supported by the expanding transportation sector and the increasing adoption of hydrogen-powered mobility solutions aimed at reducing reliance on conventional fuels. Government initiatives and financial incentives are playing a crucial role in accelerating adoption, while investments in large-scale infrastructure projects are further strengthening market expansion. Support for advanced hydrogen ecosystems is encouraging the integration of hydrogen technologies into multiple industrial and energy applications, contributing to sustained demand growth.

Key players operating in the Global Liquid Hydrogen Market include Air Products & Chemicals, Linde Plc, Shell, ENGIE, Cummins, Mitsubishi Heavy Industries, Air Liquide, Iwatani Corporation, Chart Industries, Plug Power, Messer, Kawasaki Heavy Industries, Cryostar, Cryospain, GenH2, HTEC, Matheson Tri-Gas, Ayrton Energy, Sarnia-Lambton, and GE Appliances. Key strategies adopted by companies in the Liquid Hydrogen Market focus on expanding production capacity through large-scale facility development and enhancing technological capabilities in liquefaction and storage systems. Companies are actively forming strategic alliances and joint ventures to strengthen global supply chains and accelerate infrastructure deployment. Significant investments in research and development are enabling advancements in efficient production methods and carbon capture integration to reduce emissions. Market players are also focusing on geographic expansion by establishing hydrogen hubs and distribution networks to improve accessibility. Additionally, firms are prioritizing cost optimization strategies and adopting cleaner feedstocks to enhance sustainability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Production method trends

- 2.4 Distribution method trends

- 2.5 End use trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Supply chain resilience & risk factors

- 3.1.3 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis

- 3.8 Price trend analysis, 2022-2035

- 3.8.1 By Production Method

- 3.8.2 By Country

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Production Method, 2022 - 2035 (USD Billion & MT)

- 5.1 Key trends

- 5.2 Coal Gasification

- 5.3 SMR

- 5.4 Electrolysis

Chapter 6 Market Size and Forecast, By Distribution Method, 2022 - 2035 (USD Billion & MT)

- 6.1 Key trends

- 6.2 Pipelines

- 6.3 Cryogenic Tanks

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Billion & MT)

- 7.1 Key trends

- 7.2 Transportation

- 7.3 Chemical

- 7.4 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion & MT)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Rest of World

Chapter 9 Company Profiles

- 9.1 Air Products and Chemicals

- 9.2 Air Liquide

- 9.3 Chart Industries

- 9.4 Cryospain

- 9.5 Cryostar

- 9.6 Cummins

- 9.7 ENGIE

- 9.8 GE Appliances

- 9.9 GENH2

- 9.10 HTEC

- 9.11 INOX India Limited

- 9.12 Iwatani Corporation

- 9.13 Kawasaki Heavy Industries

- 9.14 Linde plc

- 9.15 Matheson Tri-Gas

- 9.16 Messer

- 9.17 Plug Power

- 9.18 Sarnia-Lambton

- 9.19 Salzburger Aluminium Group

- 9.20 Shell plc