PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027497

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027497

Chemical Resistant Coating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

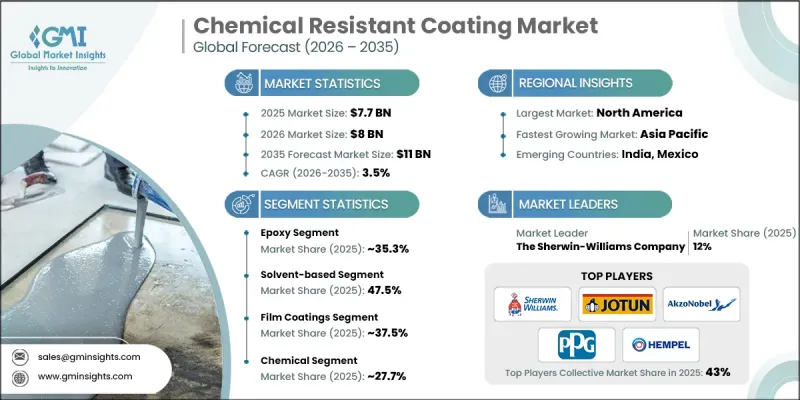

The Global Chemical Resistant Coating Market was valued at USD 7.7 billion in 2025 and is estimated to grow at a CAGR of 3.5% to reach USD 11 billion by 2035.

Market growth is driven by the increasing need across industries for durable protective solutions that can withstand aggressive chemical exposure and extend the service life of critical assets. These coatings have evolved beyond basic protection and are now essential in maintaining operational efficiency, minimizing maintenance interruptions, and improving equipment longevity across sectors such as manufacturing, energy, and heavy engineering. Market dynamics are strongly influenced by the growing emphasis on sustainability and responsible industrial practices. Companies are prioritizing environmentally compliant coating solutions that reduce emissions while maintaining high performance standards. Manufacturers are shifting toward innovative product development strategies that focus on eco-friendly formulations capable of delivering durability and cost efficiency. In addition, North America continues to foster innovation through advanced research capabilities and industrial modernization, enabling the development of specialized coating technologies tailored for complex operating conditions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.7 Billion |

| Forecast Value | $11 Billion |

| CAGR | 3.5% |

The epoxy-based coatings accounted for 35.3% share in 2025 and is expected to grow at a CAGR of 3.4% through 2035. These coatings are widely recognized for their superior adhesion, strong barrier protection, and resistance to chemical, mechanical, and thermal stress. Their structural strength makes them a reliable choice for safeguarding essential industrial equipment that requires consistent and long-term protection. Coating systems that combine epoxy and polyurethane technologies offer enhanced flexibility, impact resistance, and abrasion protection, making them suitable for applications involving dynamic structures and complex surfaces. In addition, silicone-based formulations continue to play an important role in environments exposed to prolonged heat, oxidation, and demanding atmospheric conditions due to their stability under extreme temperatures.

The solvent-based coatings segment held 47.5% share in 2025 and is anticipated to grow at a CAGR of 3.3% from 2026 to 2035. Their strong film-forming capabilities, excellent adhesion, and durability in chemically aggressive environments contribute to their continued dominance. These systems are particularly suited for operations that require reliable protection against corrosive substances and fluctuating temperature conditions. At the same time, water-based coatings are gaining traction as organizations increasingly focus on sustainability and regulatory compliance. These alternatives offer reduced emissions while maintaining effective performance, improving workplace safety, and supporting environmental goals. Powder coatings are also strengthening the market landscape by minimizing material waste and delivering efficient, environmentally responsible coating solutions with long-term operational benefits.

North America Chemical Resistant Coating Market accounted for 35% share in 2025 and continues to demonstrate strong growth potential. The region has established itself as a key hub for advanced coating technologies, supported by a well-developed industrial base, modern manufacturing infrastructure, and stringent environmental regulations. These factors encourage the adoption of high-performance and eco-friendly coating systems, enabling companies to align with safety standards while improving operational efficiency.

Leading companies operating in the Global Chemical Resistant Coating Market include PPG Industries, Inc., AkzoNobel N.V., The Sherwin-Williams Company, Hempel A/S, Jotun A/S, Axalta Coating Systems, RPM International Inc., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Asian Paints Limited, Carboline Company, and Tnemec Company, Inc. Companies in the chemical resistant coating market are adopting strategies such as expanding production capacity and strengthening global distribution networks to meet increasing demand across industries. Significant investments in research and development are enabling the creation of advanced formulations that offer enhanced durability, improved chemical resistance, and reduced environmental impact. Strategic collaborations and partnerships are helping firms access new markets and broaden their customer base. Many companies are also focusing on sustainable innovation by developing low-emission and eco-friendly coating solutions to comply with evolving regulatory standards. In addition, mergers and acquisitions are being utilized to consolidate market position, enhance technological capabilities, and diversify product portfolios, while branding and marketing efforts emphasize performance reliability and long-term cost efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Resin Type

- 2.2.3 Technology

- 2.2.4 Film Thickness

- 2.2.5 End-Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand in industrial applications

- 3.2.1.2 Stringent environmental regulations

- 3.2.1.3 Growing infrastructure development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Fluctuating raw material prices

- 3.2.3 Market opportunities

- 3.2.3.1 Transition to powder coating technologies in heavy industry

- 3.2.3.2 Sustainable & bio-based resin development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By resin type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Resin Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Epoxy

- 5.3 Polyester

- 5.4 Fluoropolymers

- 5.5 Polyurethane

- 5.6 Other resins

Chapter 6 Market Estimates and Forecast, By Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solvent-based

- 6.3 Water-based

- 6.4 Powder Coating

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Film Thickness, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Thin Film Coatings

- 7.3 Medium Build Coatings

- 7.4 Heavy Duty Coatings

- 7.5 Ultra-Heavy Duty Systems

Chapter 8 Market Estimates and Forecast, By End-User, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Chemical

- 8.2.1 Chemical Processing Plants

- 8.2.2 Petrochemical Facilities

- 8.2.3 Fertilizer Manufacturing

- 8.2.4 Others

- 8.3 Oil & gas

- 8.4 Marine

- 8.5 Construction & infrastructural

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 The Sherwin-Williams Company

- 10.2 Jotun A/S

- 10.3 AkzoNobel N.V.

- 10.4 PPG Industries, Inc.

- 10.5 Hempel A/S

- 10.6 Axalta Coating Systems

- 10.7 RPM International Inc.

- 10.8 Kansai Paint Co., Ltd.

- 10.9 Nippon Paint Holdings Co., Ltd.

- 10.10 Asian Paints Limited

- 10.11 Carboline Company

- 10.12 Tnemec Company, Inc.