PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062241

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062241

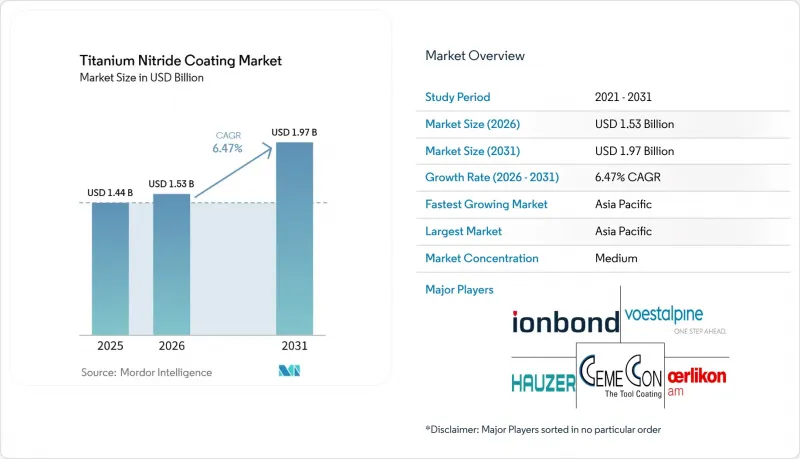

Titanium Nitride Coating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the titanium nitride coating market size was valued at USD 1.44 billion in 2025 and is estimated to grow from USD 1.53 billion in 2026 to reach USD 1.97 billion by 2031, at a CAGR of 6.47% during the forecast period (2026-2031).

This report is Segmented by Deposition Technology (Physical Vapor Deposition, Chemical Vapor Deposition, and Plasma-Spray PVD), Substrate Material (Metals, Ceramics, and More), Application (Cutting Tools and Machining Components, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Titanium Nitride Coating Market Trends and Insights

Growing Demand for Wear- and Corrosion-Resistant Coatings

Machinery owners now view TiN not as a premium option but as a cost-of-doing-business safeguard that triples cutting-tool life and halves downtime in injection-molding cells. Vickers hardness above 2,000 Hv and a friction coefficient near 0.4 allow piston rings, turbocharger shafts, and valve lifters to move away from carcinogenic hexavalent chromium layers while still meeting ISO 6507 hardness tests and ASTM G99 wear criteria. China's tooling exports exceeded USD 20 billion in 2025, and India's precision-parts sector grew 12% year-on-year, both undercutting European incumbents by pairing low-labor cost with TiN-enhanced durability. Nanocomposite TiSiCN variants further shave friction by 20%, yielding up to 2% fuel-economy gains as CAFE standards tighten.

Expansion of Precision Machining and Cutting-Tool Sectors

Five-axis CNC proliferation in Asia-Pacific and aerospace reshoring across North America heighten demand for TiN-coated carbide inserts that survive 200 m/min feed rates. High-power impulse magnetron sputtering (HiPIMS) packs denser TiN onto complex geometries; users routinely report 300% tool-life improvements when milling Ti-6Al-4V. Oerlikon's January 2026 Michigan plant is co-located with turbine-engine machining clusters, shortening qualification loops under AS9100 and Nadcap. India's machine-tool output reached USD 2.8 billion in fiscal 2025, bolstered by Production-Linked Incentives that offset coating-line capital outlays.

High Upfront Cost of PVD/CVD Equipment

A single Hauzer Flexicoat 1000, with CARC+ chambers rated for 1 X 1 m molds, costs more than USD 2 million and balloons past USD 5 million when pre-cleaning, masking, and post-processing are added. Indian SMEs (small and medium enterprises) pay 9-11% interest on capital-goods loans, stretching payback beyond seven years, whereas German rivals finance below 5%. The result is oligopolistic clustering around deep-pocketed incumbents, Oerlikon, Ionbond, Bodycote, who amortize gear across global centers and command premium coating tariffs.

Other drivers and restraints analyzed in the detailed report include:

- Rising Use in Biomedical Implants and Medical Devices

- Adoption in Decorative Finishes for Electronics and Luxury Goods

- Nano-TiN Workplace Safety and Environmental Scrutiny

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PVD represented 71.89% of the Titanium Nitride Coating market share in 2025, owing to its 1-5 µm films that marry greater than or equal to 2,000 HV hardness with decorative gold luster demanded by cutting-tool and consumer-electronics buyers. CVD retains footholds where 10-20 µm thickness or deep-hole conformality trump temperature limits, yet its 800°C cycles constrain aluminum and polymer substrates. Plasma-spray PVD's thick TiN skirts protect turbine compressor blades from sand and salt erosion; BryCoat's PS-PVD product portfolio, validated by 0.24% fatigue-strength drop versus bare Ti-6Al-4V, is scaling at 7.03% CAGR into 2031.

HiPIMS, an outgrowth of PVD, packs extra ion energy that yields dense, low-stress coatings; Ionbond's 2025 installation of Flexicoat machines in Sweden raised local capacity 40%, enabling 300% tool-life gains on aerospace-grade titanium alloys. Meanwhile, ALD TiN inside 3D-IC diffusion barriers remains a CVD sub-segment but commands wafer-level premiums. ISO 14577 hardness benchmarking now allows buyers to select suppliers by performance rather than process, fostering cross-technology substitution that chips PVD dominance.

Geography Analysis

Asia-Pacific dominated the Titanium Nitride Coating market with 41.87% revenue in 2025 and is projected to expand at 7.22% CAGR to 2031. China anchors the regional base with 220,000 tons of sponge output and more than USD 20 billion in tool exports, while Japan's JPY 39 billion Osaka Titanium project adds 10,000 tons of capacity by fiscal 2027. Taiwan and South Korea steer demand for ALD TiN diffusion barriers at 3 nm nodes, aided by TSMC's patented CMP-compatible barrier technology. ASEAN nations are erecting entry-level PVD lines, but high capital costs and financing gaps temper near-term throughput.

North America ranked second in 2025, propelled by aerospace reshoring and the Inflation Reduction Act hydrogen credits. Oerlikon's January 2026 Michigan hub is co-located with turbine-component machining centers, while Bodycote's USD 8 million Spectrum Thermal Processing buy enlarges Nadcap-accredited vacuum heat-treat and TiN capacity in the U.S. Northeast. Canadian and Mexican coaters gain under USMCA (United States-Mexico-Canada Agreement) rules, relocating deposition closer to OEM final assembly lines and trimming tariff exposure.

Europe retains a strong foothold via Germany's precision engineering, Italy's luxury-goods segment, and France's Toulouse aerospace corridor. Ionbond's 40% Sweden capacity boost and Toulouse DLC line expansion show incumbents clustering near Airbus and Tier-1 suppliers. EU REACH nano-material registration and Green Deal hydrogen targets both shape demand; larger coaters shoulder compliance costs, nudging fragmentation downward. South America and the Middle East remain smaller but rising; Brazil's double-digit orthopedic-implant growth and Saudi Vision 2030 industrial plans are early demand sparks.

- Acree Technologies Inc.

- Advanced Coating Technologies

- Bodycote plc

- BryCoat Inc.

- CemeCon AG

- IHI HAUZER TECHNO COATING B.V.

- Ion Vacuum (IVAC) Technologies Corp.

- Ionbond

- NISSIN ELECTRIC Co.

- Northeast Coating Technologies

- OC Oerlikon Management AG

- Platit AG

- Richter Precision Inc.

- Surface Engineering Technologies LLC

- Techmetals Inc.

- Teer Coatings Ltd.

- TS VTI

- voestalpine eifeler Group

- Wallwork Advanced Coatings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for wear- and corrosion-resistant coatings

- 4.2.2 Expansion of precision machining and cutting-tool sectors

- 4.2.3 Rising use in biomedical implants and medical devices

- 4.2.4 Adoption in decorative finishes for electronics and luxury goods

- 4.2.5 Hydrogen-electrolyser bipolar-plate conductivity needs

- 4.2.6 3D-IC packaging diffusion-barrier integration

- 4.3 Market Restraints

- 4.3.1 High upfront cost of PVD/CVD equipment

- 4.3.2 Performance limits under aggressive chemistries

- 4.3.3 Nano-TiN workplace safety and environmental scrutiny

- 4.3.4 High-purity titanium feedstock supply risk

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Deposition Technology

- 5.1.1 Physical Vapor Deposition (PVD)

- 5.1.2 Chemical Vapor Deposition (CVD)

- 5.1.3 Plasma-Spray PVD (PS-PVD)

- 5.2 By Substrate Material

- 5.2.1 Metals (Steel, Aluminium, and Ti-Alloys)

- 5.2.2 Ceramics

- 5.2.3 Plastics and Polymers

- 5.2.4 Other Substrates (Glass and Composites)

- 5.3 By Application

- 5.3.1 Cutting Tools and Machining Components

- 5.3.2 Molds and Dies

- 5.3.3 Medical and Dental Instruments

- 5.3.4 Automotive Components

- 5.3.5 Consumer Electronics and Decorative Hardware

- 5.3.6 Aerospace Parts

- 5.3.7 Other Applications (Energy, Watches, and Optical Devices)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)}

- 6.4.1 Acree Technologies Inc.

- 6.4.2 Advanced Coating Technologies

- 6.4.3 Bodycote plc

- 6.4.4 BryCoat Inc.

- 6.4.5 CemeCon AG

- 6.4.6 IHI HAUZER TECHNO COATING B.V.

- 6.4.7 Ion Vacuum (IVAC) Technologies Corp.

- 6.4.8 Ionbond

- 6.4.9 NISSIN ELECTRIC Co.

- 6.4.10 Northeast Coating Technologies

- 6.4.11 OC Oerlikon Management AG

- 6.4.12 Platit AG

- 6.4.13 Richter Precision Inc.

- 6.4.14 Surface Engineering Technologies LLC

- 6.4.15 Techmetals Inc.

- 6.4.16 Teer Coatings Ltd.

- 6.4.17 TS VTI

- 6.4.18 voestalpine eifeler Group

- 6.4.19 Wallwork Advanced Coatings

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment