PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027518

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027518

Wastewater Treatment Aerators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

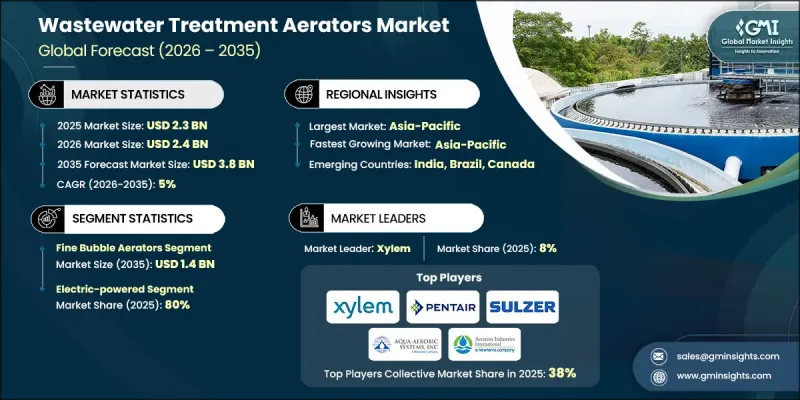

The Global Wastewater Treatment Aerators Market was valued at USD 2.3 billion in 2025 and is estimated to grow at a CAGR of 5% to reach USD 3.8 billion by 2035.

Market growth is supported by the increasing emphasis on automated process control and stricter environmental regulations governing wastewater discharge quality. Industries and municipalities are prioritizing efficient and precise aeration systems to meet compliance standards and improve operational performance. At the same time, rising consolidation across the water technology sector is accelerating innovation, as companies pursue acquisitions to broaden their product portfolios and strengthen operational capabilities. These developments are contributing to advancements in materials, system efficiency, and overall performance. Demand is also being reinforced across multiple end-use sectors, where effective wastewater management remains critical. In addition, the shift toward modernized infrastructure and digital integration is driving the adoption of next-generation aeration systems. As treatment facilities aim to optimize energy use while maintaining high efficiency, advanced aerators are emerging as essential components in achieving both environmental and economic objectives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.3 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 5% |

Conventional mechanical aerators, with fixed-speed operation and high maintenance requirements, are increasingly being replaced by technologically advanced systems. Modern aerators incorporate digital monitoring capabilities that enable improved performance and operational consistency. The integration of smart sensors, IoT-enabled connectivity, and Variable Frequency Drives allows for accurate regulation of dissolved oxygen levels, even under fluctuating wastewater conditions. These innovations contribute significantly to energy savings and system optimization, making advanced aerators a key factor in overall market expansion.

The fine bubble aerators segment generated USD 800 million in 2025 and is expected to reach USD 1.4 billion by 2035. This segment is gaining strong traction due to its high oxygen transfer efficiency, achieved through the release of numerous small bubbles that enhance oxygen diffusion. The improved efficiency supports reduced energy consumption, making these systems highly attractive for modern treatment facilities. Advanced membrane technologies further enhance precision and durability, ensuring consistent long-term performance. These features make fine bubble aerators particularly suitable for applications where maintaining stable oxygen levels is critical for treatment effectiveness.

The electric-powered segment held 80% share in 2025. Its leading position is driven by dependable performance, strong output capabilities, and seamless integration with centralized control systems used in large-scale treatment operations. These aerators offer a balanced combination of efficiency, durability, and scalability, making them a preferred choice for extensive installations requiring consistent and reliable performance.

United States Wastewater Treatment Aerators Market accounted for 88.43% share in 2025, maintaining a dominant position. Growth in this region is largely supported by strict regulatory frameworks that enforce high standards for water quality. Increasing investment in wastewater infrastructure, along with expanding industrial activities, is further driving demand for advanced aeration solutions. Additionally, the growing adoption of digital monitoring and automation technologies is reinforcing the need for high-performance aeration systems, contributing to sustained market expansion.

Key players operating in the Global Wastewater Treatment Aerators Market include Aeration Industries International, Aqua Aerobic Systems, Envirotech Systems, GE Water & Process Technologies, Hach Company, Hydroflo Pumps, Koch Membrane Systems, Nijhuis Industries, Pentair, Severn Trent Services, SPX Corporation, SUEZ Water Technologies & Solutions, Sulzer, Tetra Tech, and Xylem. Companies in the Wastewater Treatment Aerators Market are focusing on technological innovation, strategic partnerships, and capacity expansion to strengthen their competitive position. They are investing in advanced aeration technologies that incorporate automation, smart monitoring, and energy-efficient designs to meet evolving industry requirements. Collaborations and acquisitions are being used to expand product offerings and enhance global reach. Market participants are also prioritizing research and development to improve system performance and durability. In addition, companies are aligning their solutions with regulatory standards and sustainability goals to address growing environmental concerns.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Power Source

- 2.2.4 End User

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Labor shortages & remote operations

- 3.2.1.2 Stricter effluent standards & energy mandates

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High integration complexity

- 3.2.2.2 Risks related to data privacy & cybersecurity

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for Aeration-as-a-Service (AaaS)

- 3.2.3.2 Shift toward circular economy & resource recovery

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade Data Analysis (Driven by Primary Research)

- 3.8.1 Import/Export Volume & Value Trends (Driven by Primary Research) (2022-2025)

- 3.8.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.12 Distribution Infrastructure & Channel Penetration Landscape (Driven by Primary Research)

- 3.12.1 Channel Coverage by Region & Format (Modern vs. Traditional Trade) (Driven by Primary Research)

- 3.12.2 Last-Mile Infrastructure Gaps & Emerging Channel Shifts (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Diffused aerator

- 5.3 Mechanical aerator

- 5.4 Surface aerator

- 5.5 Fine bubble aerator

- 5.6 Others (coarse bubble aerator, etc.)

Chapter 6 Market Estimates & Forecast, By Power Source, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Electric-powered

- 6.3 Solar powered

Chapter 7 Market Estimates & Forecast, By End-use, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Municipal

- 7.3 Industrial

- 7.4 Others (agricultural, etc.)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Aeration Industries International

- 10.2 Aqua Aerobic Systems

- 10.3 Envirotech Systems

- 10.4 GE Water & Process Technologies

- 10.5 Hach Company

- 10.6 Hydroflo Pumps

- 10.7 Koch Membrane Systems

- 10.8 Nijhuis Industries

- 10.9 Pentair

- 10.10 Severn Trent Services

- 10.11 SPX Corporation

- 10.12 SUEZ Water Technologies & Solutions

- 10.13 Sulzer

- 10.14 Tetra Tech

- 10.15 Xylem