PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027601

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2027601

Liquid-Cooled EV Charging Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

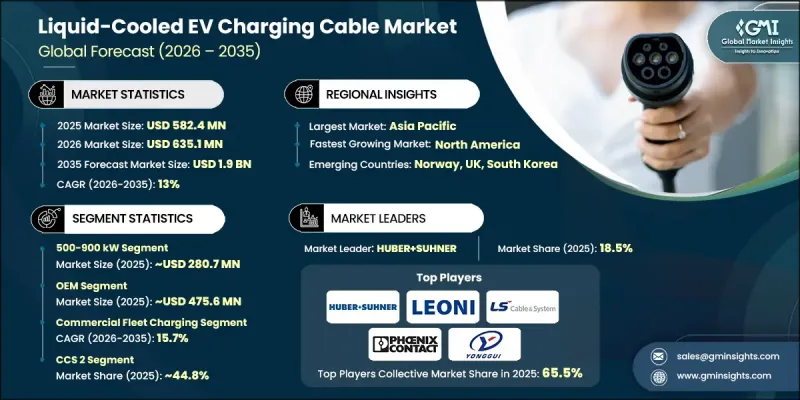

The Global Liquid-Cooled EV Charging Cable Market was valued at USD 582.4 million in 2025 and is estimated to grow at a CAGR of 13% to reach USD 1.9 billion by 2035.

Market expansion is fueled by the accelerating adoption of electric vehicles and the rising requirement for ultra-fast charging capabilities. As charging technologies evolve toward higher power outputs, the need for advanced cable systems capable of handling substantial electrical loads continues to intensify. Liquid-cooled cables are engineered to support these elevated power levels, ensuring efficiency, safety, and consistent performance during high-speed charging sessions. Increasing deployment of high-capacity charging infrastructure is reinforcing demand, particularly as next-generation charging systems aim to significantly reduce charging times. In parallel, supportive regulatory frameworks and policy initiatives are encouraging the development of advanced EV infrastructure. The transition toward high-voltage vehicle architectures is further amplifying the importance of these cables, as they enable faster energy transfer while maintaining thermal stability. Additionally, the expansion of electrified transportation across passenger and commercial segments is creating sustained demand for high-performance charging solutions, positioning liquid-cooled cable technology as a critical component of future-ready EV ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $582.4 Million |

| Forecast Value | $1.9 Billion |

| CAGR | 13% |

The 500-900 kW segment held a 48.2% share, generating USD 280.7 million in 2025. This segment is also projected to witness the fastest growth over the forecast period, supported by the increasing demand for high-capacity charging systems capable of meeting the energy needs of advanced electric vehicles equipped with larger battery systems. The growing emphasis on reducing charging duration has accelerated the deployment of high-power charging infrastructure, where liquid-cooled cables play a crucial role in managing heat and maintaining operational efficiency. As the electric vehicle landscape continues to expand, this segment is expected to remain a key contributor to overall market growth due to its ability to support rapid charging requirements.

The OEM segment accounted for 81.7% share in 2025 generating USD 475.6 million. Its dominance is primarily driven by the integral role of original equipment manufacturers in designing and delivering compatible charging solutions tailored to their vehicle platforms. These manufacturers are actively integrating advanced charging technologies to ensure optimal performance and user convenience. Liquid-cooled cables are increasingly being incorporated into these systems due to their capability to support high-power charging efficiently. As demand for high-performance electric vehicles continues to rise, OEMs are placing greater emphasis on aligning vehicle development with charging infrastructure, thereby strengthening their influence within the market.

U.S. Liquid-Cooled EV Charging Cable Market was valued at USD 113.3 million in 2025 and is anticipated to grow at a CAGR of 14% from 2026 to 2035. Growth in the United States is being supported by a strong policy environment focused on accelerating electric vehicle adoption and expanding charging infrastructure. Investments aimed at deploying high-speed charging networks are contributing significantly to market development. The increasing shift toward zero-emission mobility, along with the scaling production of electric vehicles, is further boosting the need for advanced charging solutions. Additionally, the rising electrification of commercial fleets is creating substantial demand for high-performance cables capable of supporting fast and efficient charging, reinforcing the country's position as a key market for liquid-cooled EV charging technologies.

Key companies operating in the Global Liquid-Cooled EV Charging Cable Market include ABB, Amphenol Energy, BRUGG eConnect, HUBER+SUHNER, LEONI, LS Cable & System, MIDA Power, Phoenix Contact, Sinbon Electronics, and Zhejiang Yonggui. Companies in the Global Liquid-Cooled EV Charging Cable Market are focusing on innovation, strategic partnerships, and infrastructure expansion to strengthen their market position. They are investing in advanced cooling technologies and high-performance materials to enhance cable efficiency and durability under extreme power conditions. Collaborations with automotive manufacturers and charging network providers are helping firms expand their reach and ensure compatibility with next-generation EV platforms. Many players are also scaling production capabilities to meet growing global demand while optimizing supply chains for cost efficiency. In addition, companies are targeting new geographic markets and aligning their offerings with evolving regulatory standards. Continuous research and development efforts, along with customization of solutions for specific applications, are enabling firms to differentiate themselves and maintain a competitive edge.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Cable power capacity

- 2.2.3 Cable length

- 2.2.4 Cable diameter

- 2.2.5 Conductor material

- 2.2.6 Connector

- 2.2.7 Application

- 2.2.8 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for ultrafast & megawatt charging infrastructure

- 3.2.1.2 Growing adoption of 800V EV platform architectures

- 3.2.1.3 Need for enhanced thermal management in high-power charging

- 3.2.1.4 Government mandates & incentives for EV charging infrastructure development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 System complexity & specialized maintenance requirements

- 3.2.2.2 Coolant leak risks & environmental concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit & upgrade market for existing charging stations

- 3.2.3.2 Increasing heavy-duty truck & commercial fleet electrification

- 3.2.3.3 Megawatt Charging System (MCS) development for long-haul transport

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US - SAE J3400

- 3.4.1.2 US - J1772

- 3.4.1.3 US - NEVI Program Requirements

- 3.4.2 Europe

- 3.4.2.1 European Union - EU TEN-T Regulations

- 3.4.2.2 European Union - CCS Mandates

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan - CHAdeMO 3.0

- 3.4.3.2 China - GB/T

- 3.4.4 Latin America

- 3.4.4.1 Brazil - ANEEL EV Charging Regulatory Framework

- 3.4.4.2 Mexico - EVSE Deployment Initiatives

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE - National Electric Vehicle Policy

- 3.4.5.2 UAE - Dubai/Abu Dhabi EV Charging Network Regulations

- 3.4.1 North America

- 3.5 Investment & funding analysis

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technologies

- 3.8.1.1 800V High-Voltage EV Platforms

- 3.8.1.2 Megawatt Charging Systems (MCS)

- 3.8.1.3 Advanced Thermal Management Systems

- 3.8.2 Emerging technologies

- 3.8.2.1 Dielectric Coolant-Based Charging Cables

- 3.8.2.2 Ultra-Fast Heavy-Duty Truck Charging Solutions

- 3.8.1 Current technologies

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.10 Patent landscape (Driven by Primary Research)

- 3.11 Use case analysis

- 3.12 Pricing analysis (Driven by Primary Research)

- 3.12.1 Historical price trend analysis

- 3.12.2 Pricing strategy by player type (Premium / Value / Cost-plus)

- 3.13 Trade data analysis (Driven by Paid Database)

- 3.13.1 Import/export volume & value trends

- 3.13.2 Key trade corridors & tariff impact

- 3.14 Patent landscape (Driven by Primary Research)

- 3.15 Cost breakdown analysis

- 3.16 Capacity & Production Landscape (Driven by Primary Research)

- 3.16.1 Installed Capacity by Region & Key Producer

- 3.16.2 Capacity Utilization Rates & Expansion Pipelines

- 3.17 Sustainability and environmental impact

- 3.17.1 Environmental impact assessment

- 3.17.2 Social impact & community benefits

- 3.17.3 Governance & corporate responsibility

- 3.17.4 Sustainable finance & investment trends

- 3.18 Impact of AI and Generative AI on the market

- 3.18.1 AI-driven disruption of existing business models

- 3.18.2 GenAI use cases & adoption roadmap by segment

- 3.18.3 Risks, limitations & regulatory considerations

- 3.19 Rapid expansion of ultra-fast charging networks

- 3.19.1 Highway corridor deployment strategies

- 3.19.2 Commercial and fleet-oriented ultra-fast hubs

- 3.19.3 Public-private partnerships (PPPs) and investment models

- 3.19.4 Technological standardization and interoperability

- 3.20 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.20.1 Base Case - Key macro & industry variables driving CAGR

- 3.20.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.20.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Cable Power Capacity, 2022 - 2035 ($ Million, Units)

- 5.1 Key trends

- 5.2 300-499 kW

- 5.3 500-900 kW

- 5.4 Above 900 kW

Chapter 6 Market Estimates and Forecast, By Cable Length, 2022 - 2035 ($ Million, Units)

- 6.1 Key trends

- 6.2 Upto 5 meters

- 6.3 6-10 meters

- 6.4 Above 10 meters

Chapter 7 Market Estimates and Forecast, By Cable Diameter, 2022 - 2035 ($ Million, Units)

- 7.1 Key trends

- 7.2 Below 30 mm

- 7.3 30-50 mm

- 7.4 Above 50 mm

Chapter 8 Market Estimates and Forecast, By Conductor Material, 2022 - 2035 ($ Million, Units)

- 8.1 Key trends

- 8.2 Copper

- 8.3 Aluminium

Chapter 9 Market Estimates and Forecast, By Connector, 2022 - 2035 ($ Million, Units)

- 9.1 Key trends

- 9.2 Type 1

- 9.3 Type 2

- 9.4 CCS1

- 9.5 CCS2

- 9.6 CHAdeMO

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Million, Units)

- 10.1 Key trends

- 10.2 Public Charging Stations

- 10.3 Commercial Fleet Charging

- 10.4 Residential / Private Charging

- 10.5 Highway and Long-Distance Charging Networks

Chapter 11 Market Estimates and Forecast, By Sales Channel, 2022 - 2035 ($ Million, Units)

- 11.1 Key trends

- 11.2 OEM

- 11.3 Aftermarket

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Million, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Netherlands

- 12.3.8 Norway

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Philippines

- 12.4.9 Vietnam

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global players

- 13.1.1 Phoenix Contact

- 13.1.2 HUBER+SUHNER

- 13.1.3 LEONI

- 13.1.4 Sinbon Electronics

- 13.1.5 KemPower

- 13.1.6 ABB

- 13.1.7 LS Cable & System

- 13.1.8 Southwire Company

- 13.1.9 ITT Canon

- 13.1.10 Colder Products Company

- 13.1.11 Amphenol Energy

- 13.1.12 Coroflex

- 13.2 Regional players

- 13.2.1 OMG EV Cable

- 13.2.2 MIDA Power

- 13.2.3 Zhejiang Yonggui

- 13.2.4 Suzhou Yihang

- 13.2.5 Qingdao Penoda Electrical

- 13.3 Emerging players

- 13.3.1 BRUGG eConnect

- 13.3.2 Teison Energy

- 13.3.3 Caledonian Cables