PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038340

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038340

Self-Monitoring Blood Glucose Monitoring Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

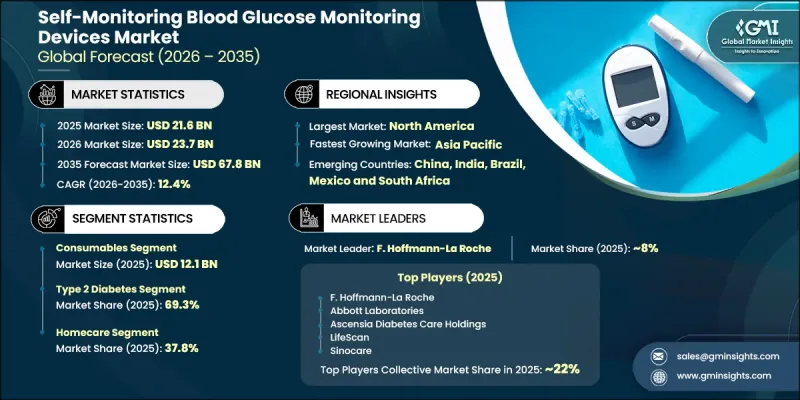

The Global Self-Monitoring Blood Glucose Monitoring Devices Market was valued at USD 21.6 billion in 2025 and is estimated to grow at a CAGR of 12.4% to reach USD 67.8 billion in 2035.

Market expansion is driven by the rising global burden of diabetes, continuous improvements in glucose monitoring technologies, and increasing government-led awareness programs focused on early diagnosis and disease management. Growing adoption of self-care-based diabetes management is further strengthening demand for home-use monitoring solutions. Technological progress in device accuracy, portability, and connectivity is also enhancing user convenience and compliance. Rising healthcare expenditure and broader access to diagnostic tools are further supporting market penetration across both developed and emerging economies. In addition, increasing lifestyle-related health risks, sedentary habits, and dietary changes are contributing to higher diabetes incidence, thereby reinforcing the need for continuous glucose monitoring. Expanding awareness regarding preventive healthcare and early intervention is also encouraging patients to adopt self-monitoring solutions for better glycemic control.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.6 Billion |

| Forecast Value | $67.8 Billion |

| CAGR | 12.4% |

The consumables segment was valued at USD 12.1 billion in 2025. Self-monitoring blood glucose monitoring systems rely heavily on consumable products such as test strips and lancets, which are essential for routine glucose testing. These single-use components are widely available through retail channels, ensuring easy access for users managing diabetes at home. Test strips represent a core consumable category as they are designed for single-use blood sample collection and glucose measurement. Their compact and portable nature allows patients to monitor glucose levels conveniently across different settings, including home and workplace environments.

The type 2 diabetes segment held a 69.3% share in 2025. This segment leads due to the widespread nature of type 2 diabetes, where the body either produces insufficient insulin or fails to utilize it effectively, resulting in elevated blood glucose levels. The rising incidence of this condition globally continues to drive sustained demand for regular glucose monitoring, reinforcing segment dominance.

U.S. Self-Monitoring Blood Glucose Monitoring Devices Market reached USD 7.6 billion in 2025. High diabetes-related healthcare expenditure and strong healthcare infrastructure support widespread adoption of advanced monitoring solutions. Continuous investment in innovative diabetes management technologies further strengthens market growth, improving accessibility and patient outcomes across the country.

Key companies operating in the Global Self-Monitoring Blood Glucose Monitoring Devices Market include Roche, Abbott Laboratories, LifeScan, Ascensia Diabetes Care Holdings, Sinocare, B. Braun Melsungen, Sanofi, Arkray, Nova Biomedical, AgaMatrix, DarioHealth, Ypsomed Holding, Bionime Corporation, All Medicus, and Omnis Health. Companies in the self-monitoring blood glucose monitoring devices market are focusing on continuous product innovation to improve accuracy, usability, and connectivity of glucose monitoring systems. Strategic investments in smart and digital health-integrated devices are strengthening real-time data tracking capabilities. Firms are also expanding product portfolios with user-friendly and minimally invasive solutions to enhance patient comfort and adherence. Partnerships with healthcare providers and digital health platforms are improving distribution reach and patient engagement. Increasing emphasis on affordability and accessibility is helping companies penetrate emerging markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.1.1 Key market trends

- 2.1.2 Regional trends

- 2.1.3 Product trends

- 2.1.4 Application trends

- 2.1.5 End use trends

- 2.2 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of diabetes worldwide

- 3.2.1.2 Government initiatives for increasing awareness among people

- 3.2.1.3 Technological advancements of self-monitoring blood glucose monitoring devices in developed countries

- 3.2.1.4 Rising shift toward home-based and self-care monitoring

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced devices and accessories in developing countries

- 3.2.2.2 Stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape (Driven by Primary Research)

- 3.5.1 Current technologies

- 3.5.1.1 Electrochemical finger prick glucose meters

- 3.5.1.2 Bluetooth enabled smart SMBG devices

- 3.5.1.3 Mobile applications linked to SMBG systems

- 3.5.2 Emerging technologies

- 3.5.2.1 AI enabled glucose pattern analysis and decision support

- 3.5.2.2 Non invasive and minimally invasive SMBG technologies

- 3.5.2.3 Advanced test strip chemistries and multi-parameter sensing

- 3.5.2.4 Integrated digital diabetes management ecosystems

- 3.5.1 Current technologies

- 3.6 Pricing analysis, 2025 (Driven by Primary Research)

- 3.7 Future market trends (Driven by Primary Research)

- 3.8 Impact of AI and Generative AI on the market (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Self-monitoring blood glucose meters

- 5.3 Consumables

- 5.3.1 Testing strips

- 5.3.2 Lancets

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Type 1 diabetes

- 6.3 Type 2 diabetes

- 6.4 Gestational diabetes

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital

- 7.3 Ambulatory surgical centers

- 7.4 Diagnostic centers

- 7.5 Homecare

- 7.6 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 UK

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AgaMatrix

- 9.3 All Medicus

- 9.4 Arkray

- 9.5 Ascensia Diabetes Care Holdings

- 9.6 B. Braun Melsungen

- 9.7 Bionime Corporation

- 9.8 DarioHealth

- 9.9 F. Hoffmann-La Roche

- 9.10 LifeScan

- 9.11 Nova Biomedical

- 9.12 Omnis Health

- 9.13 Sanofi

- 9.14 Sinocare

- 9.15 Ypsomed Holding