PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038355

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038355

Europe Plastic Waste Pyrolysis Oil Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

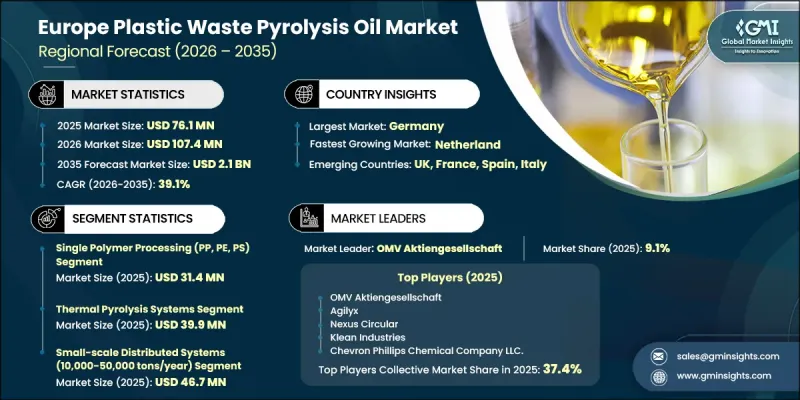

Europe Plastic Waste Pyrolysis Oil Market was valued at USD 76.1 million in 2025 and is estimated to grow at a CAGR of 39.1% share to reach USD 2.1 billion by 2035.

The Europe plastic waste pyrolysis oil industry continues to gain strong momentum as it offers a viable pathway for converting plastic waste into usable energy and chemical resources through oxygen-free thermal processing. This method allows difficult-to-recycle plastic materials to be transformed into a liquid output with fuel-like properties, supporting regional efforts to reduce waste volumes and improve resource recovery. The produced oil is widely regarded as an intermediate product that requires further refinement before end-use, aligning with regulatory frameworks and industrial standards. It plays a growing role across energy generation, refining processes, and chemical manufacturing, depending on technical compatibility and policy alignment. Advancements in system design and operational technologies are improving efficiency, safety, and environmental performance, enabling more consistent output quality. Enhanced feedstock preparation and monitoring systems are also supporting scalable production, positioning pyrolysis as a key contributor to circular economy initiatives and sustainable waste management practices across Europe.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $76.1 Million |

| Forecast Value | $2.1 Billion |

| CAGR | 39.1% |

The single polymer processing segment, including PP, PE, and PS, accounted for a market value of USD 31.4 million in 2025 owing to its ability to generate higher oil yields and maintain consistent product quality suitable for downstream processing. Operators prioritize controlled polymer streams to ensure predictable performance and reduce operational complexity. The availability of industrial plastic waste and production residues further supports reliable feedstock sourcing, enabling manufacturers to scale operations efficiently while maintaining quality standards. The focus on streamlined processing and improved output consistency continues to strengthen the position of this segment.

The chemical feedstock segment reached a USD 26.7 million in 2025 and is emerging as a high-growth area within the Europe plastic waste pyrolysis oil industry. Increasing adoption is driven by the shift toward alternative raw materials in petrochemical production, where pyrolysis oil is being integrated into manufacturing processes as a substitute input. At the same time, energy-related applications remain relevant for operational requirements, while additional use cases involving upgraded materials and refined outputs are gaining traction due to ongoing technological advancements and regulatory alignment. This diversification of applications is supporting broader market expansion and enhancing the overall value proposition of pyrolysis-derived products.

Germany Plastic Waste Pyrolysis Oil Market accounted for USD 24.6 million in 2025 and is anticipated to reach USD 683.6 million by 2035, reinforcing its leadership within the Europe plastic waste pyrolysis oil market. The country's strong regulatory framework, combined with strict waste management policies and advanced sorting infrastructure, creates a favorable environment for market growth. Established industrial networks and collaboration between processing facilities and downstream industries support continuous development of advanced recycling systems. Government support and alignment with sustainability goals further accelerate the adoption of pyrolysis technologies, enabling consistent expansion and strengthening Germany's role as a key regional hub.

Key companies operating in the Europe Plastic Waste Pyrolysis Oil Market include Agilyx, OMV Aktiengesellschaft, Chevron Phillips Chemical Company LLC., Nexus Circular, Klean Industries, Niutech Environment Technology Corporation, ETIA S.A.S., Ecomation Oy, Kingtiger (Shanghai) Environmental Technology Co., Ltd., and Agile Process Chemicals LLP. Companies in the Europe plastic waste pyrolysis oil market are focusing on strategic innovation and capacity expansion to strengthen their competitive positioning. Investments in advanced reactor technologies and process optimization are helping improve efficiency, scalability, and output consistency. Firms are actively forming partnerships with chemical producers and energy companies to secure long-term demand and integrate pyrolysis outputs into existing value chains. Emphasis on feedstock management and supply chain stability ensures reliable production at scale. Sustainability remains a central focus, with companies aligning operations to regulatory standards and circular economy goals. Additionally, businesses are expanding geographically and enhancing technical capabilities to meet rising demand, while improving cost efficiency and environmental performance across their operations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Feedstock type

- 2.2.2 Technology

- 2.2.3 Processing type

- 2.2.4 Application

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising plastic waste generation across Europe

- 3.2.1.2 Limitations of conventional recycling methods

- 3.2.1.3 Supportive waste management and sustainability policies

- 3.2.2 Pitfalls/challenge

- 3.2.2.1 Utilization of mixed plastic waste streams

- 3.2.2.2 Demand for alternative feedstock sources

- 3.2.3 Opportunities

- 3.2.3.1 Variability in plastic waste composition

- 3.2.3.2 High initial investment and operating costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Europe

- 3.4.1.1 Germany

- 3.4.1.2 France

- 3.4.1.3 Netherlands

- 3.4.1.4 Italy

- 3.4.1.5 UK

- 3.4.1.6 Spain

- 3.4.1.7 Rest of Europe

- 3.4.1 Europe

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By feedstock type

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 Europe

- 4.2.1.1.1 Germany

- 4.2.1.1.2 France

- 4.2.1.1.3 Netherlands

- 4.2.1.1.4 Italy

- 4.2.1.1.5 UK

- 4.2.1.1.6 Spain

- 4.2.1.1.7 Rest of Europe

- 4.2.1.1 Europe

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Feedstock Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Mixed plastic waste streams

- 5.3 Single polymer processing (PP, PE, PS)

- 5.4 Industrial plastic waste and manufacturing residues

- 5.5 Municipal solid waste plastic fractions

Chapter 6 Market Estimates and Forecast, By Technology, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Thermal pyrolysis systems

- 6.3 Catalytic pyrolysis

- 6.4 Advanced and hybrid technologies

Chapter 7 Market Estimates and Forecast, By Processing Scale, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Large-scale centralized facilities (200,000+ tons/year)

- 7.3 Medium-scale regional processing (50,000-200,000 tons/year)

- 7.4 Small-scale distributed systems (10,000-50,000 tons/year)

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Industrial fuel

- 8.3 Marine fuel

- 8.4 Chemical feedstock

- 8.5 Electricity generation

- 8.6 Heating

- 8.7 Other

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Europe

- 9.2.1 Germany

- 9.2.2 France

- 9.2.3 Netherlands

- 9.2.4 Italy

- 9.2.5 UK

- 9.2.6 Spain

- 9.2.7 Rest of Europe

Chapter 10 Company Profiles

- 10.1 Agile Process Chemicals LLP

- 10.2 Agilyx

- 10.3 Chevron Phillips Chemical Company LLC.

- 10.4 Ecomation Oy

- 10.5 ETIA S.A.S.

- 10.6 Kingtiger (Shanghai) Environmental Technology Co., Ltd.

- 10.7 Klean Industries

- 10.8 Nexus Circular

- 10.9 Niutech Environment Technology Corporation

- 10.10 OMV Aktiengesellschaft