PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038467

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038467

Water Treatment Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

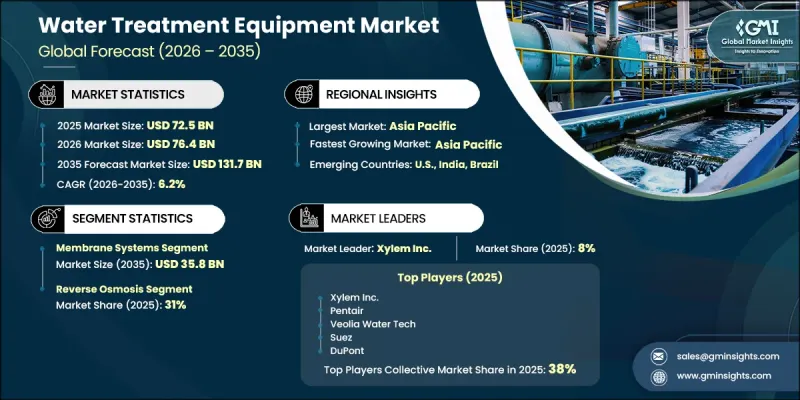

The Global Water Treatment Equipment Market was valued at USD 72.5 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 131.7 billion by 2035.

The market is experiencing expansion driven by rising concerns over water scarcity, tightening global regulations on water quality, and growing demand for efficient purification systems across industrial applications. Increasing pressure on industries to ensure safe and reusable process water is further strengthening the adoption of advanced treatment solutions. Consolidation within the industry through mergers and acquisitions is also accelerating technological progress, particularly in membrane-based filtration and separation technologies. These developments are enabling companies to expand their presence across multiple end-use sectors, including chemicals, food and beverage production, pharmaceuticals, and municipal water systems. At the same time, traditional treatment approaches are being replaced by smart systems that integrate sensors, automation, and digital monitoring capabilities. These modern solutions improve operational efficiency, enhance water quality control, and support energy-efficient treatment processes. Rapid urban development, increasing adoption of water recycling initiatives in developed regions, and growing infrastructure investments in emerging economies are further reinforcing demand for advanced water treatment equipment globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $72.5 Billion |

| Forecast Value | $131.7 Billion |

| CAGR | 6.2% |

The membrane systems segment reached USD 18.7 billion in 2025 and is projected to grow to USD 35.8 billion by 2035. This segment is gaining strong traction due to its high separation efficiency and ability to deliver superior water purification results. Its capability to eliminate dissolved impurities makes it highly suitable for advanced water reuse applications as well as desalination processes, strengthening its role in modern water treatment systems.

The reverse osmosis segment accounted for 31% share in 2025 and is expected to rise to 32.4% by 2035. Growth in this segment is supported by its strong performance in desalination, industrial water reuse, and high-purity water production applications. Its ability to effectively remove a wide range of contaminants makes it a preferred technology for both municipal and industrial water treatment systems.

United States Water Treatment Equipment Market held a 76% share in 2025, supported by stringent water quality regulations enforced by environmental authorities at both the federal and state levels. Increasing implementation of industrial water recycling programs and expansion of advanced manufacturing activities are further driving demand in the country. Growing investments in smart water infrastructure and digital monitoring systems are also enhancing the adoption of automated treatment technologies and advanced membrane solutions.

Key companies operating in the Global Water Treatment Equipment Market include Pentair, Veolia Water Tech, Xylem Inc., Suez, Grundfos, ITT Inc., DuPont Water, Ovivo Inc., AO Smith, Culligan, Ecowater, Kurita Europe, Pall (Danaher), Parkson, SAMCO Technologies, Smith & Loveless, and Trojan (Veralto). Companies in the Water Treatment Equipment Market are focusing on strengthening their competitive position through continuous technological advancement and system innovation. Many players are investing heavily in smart water solutions that integrate automation, IoT-enabled sensors, and real-time monitoring capabilities to enhance operational efficiency. Expansion of membrane-based technologies and advanced filtration systems remains a key strategic priority, enabling improved treatment performance and broader application coverage. Strategic mergers and acquisitions are also being used to expand geographic reach and strengthen technological capabilities. Firms are increasingly targeting industrial water reuse and sustainability-focused solutions to meet tightening environmental regulations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Technology

- 2.2.4 End User

- 2.2.5 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailors

- 3.2 Regulatory landscape

- 3.3 Industry Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing demand for effective water treatment solutions from end users

- 3.3.1.2 Strict regulations and policies for water treatment

- 3.3.1.3 Advancements in water treatment technology

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High initial cost

- 3.3.1 Growth drivers

- 3.4 Major market trends and disruptions

- 3.5 Future market trends

- 3.6 Risk and mitigation analysis

- 3.7 Growth potential analysis

- 3.8 Pricing analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis (Driven by Primary Research)

- 3.8.2 Pricing Strategy by Player Type (Premium / Mid-range / Budget) (Driven by Primary Research)

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Trade Data Analysis

- 3.11.1 Import & Export Volume & Value Trends (Driven by Primary Research)

- 3.11.2 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.12 Impact of AI & Generative AI on the Market

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.12.3 Risks, Limitations & Regulatory Considerations

- 3.12.4 Ecosystem Lock-In Effects: Samsung Galaxy vs Apple Ecosystem Analysis

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer (Modern vs. Traditional Trade) (Driven by Primary Research)

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Sedimentation tanks

- 5.3 Filtration systems

- 5.4 Disinfection equipment

- 5.5 Softening equipment

- 5.6 Membrane systems

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Reverse osmosis

- 6.3 Microfiltration

- 6.4 Clarifier

- 6.5 Distillation

- 6.6 Ion exchange

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By End User, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Agriculture

- 7.4 Chemical manufacturing

- 7.5 Food processing

- 7.6 Construction

- 7.7 Pharmaceutical production

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 10.1 Top Global Players

- 10.1.1 Xylem Inc.

- 10.1.2 Pentair

- 10.1.3 Veolia Water Tech

- 10.1.4 Suez

- 10.1.5 Grundfos

- 10.1.6 DuPont Water

- 10.1.7 Pall (Danaher)

- 10.1.8 Trojan (Veralto)

- 10.1.9 Kurita Europe

- 10.2 Regional Champions

- 10.2.1 AO Smith

- 10.2.2 Culligan

- 10.2.3 Ecowater

- 10.2.4 ITT Inc.

- 10.2.5 Parkson

- 10.3 Emerging & Specialized Players

- 10.3.1 Smith & Loveless

- 10.3.2 Ovivo Inc.

- 10.3.3 SAMCO Technologies