PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038705

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038705

Battery Electric Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

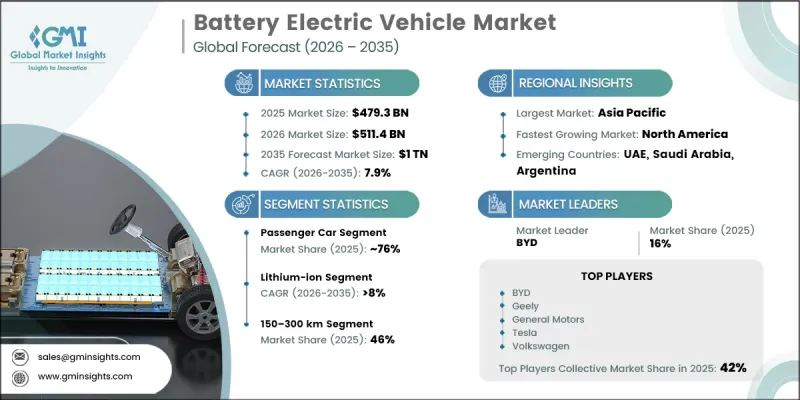

The Global Battery Electric Vehicle Market was valued at USD 479.3 billion in 2025 and is estimated to grow at a CAGR of 7.9% to reach USD 1 trillion by 2035.

Market expansion is driven by rapid cost reductions in lithium-ion battery systems, improvements in energy density, and extended driving ranges that are making electric mobility increasingly competitive with conventional vehicles. Automakers are also broadening their electric vehicle portfolios across multiple segments, including SUVs, sedans, pickups, and commercial vans, to address a wider consumer base. Lower maintenance requirements and reduced operating costs are further strengthening adoption, particularly among fleet operators focused on long-term cost efficiency. Global battery electric vehicle uptake is accelerating due to strict emission regulations, national decarbonization strategies, and evolving fuel economy standards. Government mandates promoting zero-emission transportation and restrictions on internal combustion engine vehicle sales are pushing manufacturers toward full electrification. In parallel, public sector investments in electric buses and municipal fleets are increasing volume demand while stimulating the development of charging infrastructure. Rapid expansion of charging networks across urban centers and highways is also reducing range anxiety, improving accessibility, and supporting both private and commercial EV adoption across global markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $479.3 Billion |

| Forecast Value | $1 Trillion |

| CAGR | 7.9% |

The passenger car segment held a 76% share in 2025 and is expected to grow at a CAGR of 7% through 2035. Growth in this segment is supported by significant improvements in battery performance and driving range, making electric passenger cars more practical for daily use. Enhanced energy recovery systems, including regenerative braking, are improving efficiency in urban driving conditions. These advancements are helping reduce range concerns and positioning electric passenger vehicles as a mainstream option for commuting, family travel, and general household transportation.

The lithium-ion battery segment held a 89% share in 2025 and is projected to grow at a CAGR of 8% from 2026 to 2035. Lithium-ion technology continues to lead due to its high energy density, which enables longer driving ranges while maintaining a lightweight system architecture. Its compact design and strong power-to-weight ratio make it highly suitable for passenger cars, SUVs, and commercial electric vehicles. Automakers prefer lithium-ion systems for their ability to optimize interior space, improve efficiency, and enhance overall vehicle performance. Continuous cost reductions in cell manufacturing are further accelerating adoption across the battery electric vehicle ecosystem.

China Battery Electric Vehicle Market held a 45% share in 2025, generating USD 107.3 billion. Market growth in the country is strongly supported by government-driven policies, including incentives, registration benefits, and strict emission regulations that encourage rapid adoption of new energy vehicles. National electrification targets are accelerating deployment across passenger, public transport, and commercial vehicle segments. A well-established domestic battery supply chain is also playing a critical role in strengthening production capacity and supporting large-scale market expansion across the country.

Key companies operating in the Global Battery Electric Vehicle Industry include Tesla, BYD, Volkswagen, General Motors, BMW, Hyundai, Geely, SAIC Motor, Great Wall Motor, and Stellantis. Companies in the Battery Electric Vehicle Market are focusing on strengthening their competitive position through continuous investment in battery innovation, vehicle range expansion, and cost optimization strategies. Automakers are scaling up production capacity while integrating advanced software-defined vehicle platforms to enhance performance and connectivity features. Strategic partnerships with battery manufacturers are helping secure raw material supply chains and improve cost efficiency. Expansion of charging infrastructure collaborations is also being prioritized to support wider EV adoption. In addition, companies are accelerating the development of modular EV platforms to reduce manufacturing complexity and speed up model rollout. Geographic expansion into emerging markets, combined with localized production strategies, is further enhancing market penetration.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Battery

- 2.2.4 Vehicle Range

- 2.2.5 Battery Capacity

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Government incentives and EV subsidies

- 3.2.1.2 Expansion of charging infrastructure

- 3.2.1.3 Falling battery costs

- 3.2.1.4 Stringent emission regulations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront vehicle prices

- 3.2.2.2 Raw material supply volatility

- 3.2.2.3 Charging speed and grid limitations

- 3.2.2.4 Battery recycling and second-life ecosystem gaps

- 3.2.3 Market opportunities

- 3.2.3.1 Commercial fleet electrification

- 3.2.3.2 Emerging market penetration

- 3.2.3.3 Battery swapping and energy services

- 3.2.3.4 Affordable compact BEVs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.3 Occupational Safety and Health Administration (OSHA)

- 3.4.1.4 U.S. Department of Transportation (DOT)

- 3.4.1.5 Canadian Motor Vehicle Safety Standards (CMVSS)

- 3.4.2 Europe

- 3.4.2.1 EU CO2 Emission Performance Standards

- 3.4.2.2 Euro NCAP Safety Standards

- 3.4.2.3 EU Battery Regulation (EU 2023/1542)

- 3.4.2.4 REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals)

- 3.4.2.5 National Type Approval & Road Homologation Requirements

- 3.4.3 Asia Pacific

- 3.4.3.1 China New Energy Vehicle (NEV) Policy Framework

- 3.4.3.2 China Compulsory Certification (CCC)

- 3.4.3.3 Indian Central Motor Vehicle Rules (CMVR)

- 3.4.3.4 Japanese Automotive Safety Standards (JASIC/JIS-based regulations)

- 3.4.3.5 ASEAN Automotive Mutual Recognition Arrangement (AAMRA)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Institute of Metrology (INMETRO) Regulations

- 3.4.4.2 Brazilian National Traffic Council (CONTRAN)

- 3.4.4.3 Mexican NOM Safety and Emission Standards

- 3.4.4.4 Mercosur Vehicle Technical Regulations

- 3.4.4.5 Regional Import & Certification Requirements

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Standardization Organization (GSO) Regulations

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.5.3 Emirates Authority for Standardization and Metrology (ESMA)

- 3.4.5.4 South African National Regulator for Compulsory Specifications (NRCS)

- 3.4.5.5 National Road Traffic Act (NRTA) Compliance

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Trade data analysis (Driven by Paid Research)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis (Driven by Primary Research)

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger Cars

- 5.2.1 Hatchbacks

- 5.2.2 Sedans

- 5.2.3 SUVs

- 5.3 Commercial Vehicles

- 5.3.1 Light duty

- 5.3.2 Medium duty

- 5.3.3 Heavy duty

- 5.3.4 Electric Buses

- 5.4 Two-wheelers

- 5.5 Three-Wheelers

- 5.6 E-Bikes

Chapter 6 Market Estimates & Forecast, By Battery, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Lithium-ion

- 6.3 NiMH

- 6.4 SLA

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Vehicle Range, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Below 150 km

- 7.3 150-300 km

- 7.4 Above 300 km

Chapter 8 Market Estimates & Forecast, By Battery Capacity, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 < 50 kWh

- 8.3 50-100 kWh

- 8.4 > 100 kWh

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Private / personal

- 9.3 Fleet & ride-hailing

- 9.4 Logistics & delivery

- 9.5 Public transit

- 9.6 Defence & government

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Southeast Asia

- 10.4.6 ANZ

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BMW Group

- 11.1.2 BYD

- 11.1.3 Ford Motor Company

- 11.1.4 General Motors

- 11.1.5 Hyundai Motor Company

- 11.1.6 Mercedes-Benz

- 11.1.7 Renault-Nissan-Mitsubishi Alliance

- 11.1.8 Stellantis

- 11.1.9 Tesla

- 11.1.10 Toyota

- 11.1.11 Volkswagen

- 11.2 Regional Players

- 11.2.1 Changan Automobile

- 11.2.2 Chery

- 11.2.3 GAC Group

- 11.2.4 Geely

- 11.2.5 Great Wall Motor

- 11.2.6 SAIC Motor

- 11.3 Emerging Players

- 11.3.1 Li Auto

- 11.3.2 NIO

- 11.3.3 VinFast

- 11.3.4 XPeng