PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038757

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038757

Renewable Energy Insurance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

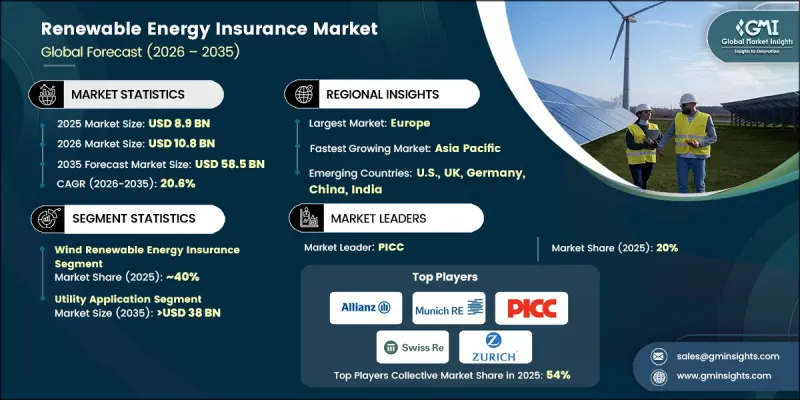

The Global Renewable Energy Insurance Market was valued at USD 8.9 billion in 2025 and is estimated to grow at a CAGR of 20.6% to reach USD 58.5 billion by 2035.

The increasing deployment of renewable energy assets has intensified the need for specialized insurance solutions that safeguard high-value installations against a wide range of risks. Geographic diversity and evolving climate conditions are elevating exposure to environmental uncertainties, making risk transfer mechanisms essential for project sustainability. Capital inflows from institutional and private investors into renewable power generation and energy storage systems are further reinforcing the importance of insurance coverage. These policies play a critical role in protecting infrastructure from operational challenges, financial losses, and unforeseen disruptions, thereby improving project viability and investor confidence. As climate variability continues to influence energy systems, insurance solutions are becoming integral to risk management frameworks. The renewable energy insurance market is therefore emerging as a vital support system for the clean energy transition, helping stakeholders maintain financial stability while navigating an increasingly complex risk environment.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.9 Billion |

| Forecast Value | $58.5 Billion |

| CAGR | 20.6% |

Renewable energy insurance provides structured financial protection for projects by addressing risks associated with operations, technology performance, and environmental factors. Coverage typically includes protection against physical asset damage, operational interruptions, construction-related setbacks, and liability concerns. These insurance solutions are essential for developers, operators, and investors seeking to ensure long-term project stability and minimize exposure to financial uncertainties. As environmental risks intensify, the reliance on insurance solutions is increasing, supporting broader adoption of renewable energy infrastructure and enabling stakeholders to manage potential losses more effectively.

The wind segment accounted for 40% share in 2025 and is expected to grow at a CAGR of 20% by 2035. The expansion of large-scale wind energy installations has heightened exposure to technical and operational risks, which can result in costly repairs and extended downtime. These challenges are encouraging the development of tailored insurance products that address performance risks, equipment failures, and revenue disruptions, thereby strengthening the outlook for insurers specializing in this segment.

The utility segment accounted for 69.8% of the market in 2025 and is anticipated to reach USD 38 billion by 2035. The integration of renewable energy into utility operations has introduced new complexities in asset management and system reliability. This has increased the need for insurance solutions that address operational risks, system vulnerabilities, and financial impacts associated with service disruptions. Utilities are increasingly adopting comprehensive insurance coverage to protect against revenue loss and ensure continuity in energy supply.

United States Renewable Energy Insurance Market held an 80% share in 2025, generating USD 1.9 billion. The growing impact of environmental disruptions on energy infrastructure has increased financial exposure for asset owners. As a result, there is a growing demand for insurance solutions that cover asset damage, operational interruptions, and performance-related losses. Additionally, the increasing focus on sustainable infrastructure and green financing initiatives is encouraging organizations to incorporate insurance as a key component of their risk management strategies.

Key participants in the Global Renewable Energy Insurance Market include AEGIS, AIG, Allianz, Aon, AXA, AXIS Capital Holdings, Canopius, Chubb, Descartes Underwriting, Energy Insurance Mutual, Fairfax Financial Holdings, Gallagher, HDI Global, Horton Group, kWh Analytics, Liberty Specialty Markets, Markel Group, Marsh & McLennan Companies, Miller, Munich Re, Ping An Insurance (Group) Company of China, PICC, RSA Insurance, Swiss Re, Tokio Marine Kiln, Travelers, Willis Towers Watson (WTW), and Zurich Insurance. Companies operating in the renewable energy insurance market are strengthening their position through innovation, partnerships, and expanded service offerings. They are investing in advanced risk modeling and data analytics to better assess project-specific exposures and provide customized insurance solutions. Strategic collaborations with energy developers and financial institutions are enabling insurers to enhance product relevance and accelerate market penetration. Firms are also broadening their global presence by entering emerging renewable energy markets and strengthening distribution networks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Technology trends

- 2.1.3 Coverage type trends

- 2.1.4 End use trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of renewable energy insurance

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization & IoT integration

- 3.10 Growth in untapped markets & applications

- 3.11 Investment analysis & future prospects

- 3.12 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.12.1 AI-Driven production optimization (Driven by Primary Research)

- 3.12.2 Predictive maintenance & fault detection (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Rest of World

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Solar PV

- 5.3 Wind

- 5.4 Hydropower

- 5.5 Others

Chapter 6 Market Size and Forecast, By Coverage Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Property insurance

- 6.3 Liability insurance

- 6.4 Business interruption insurance

- 6.5 Equipment breakdown insurance

- 6.6 Others

Chapter 7 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Utility

- 7.3 Commercial & industrial

- 7.4 Residential

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 Poland

- 8.3.4 Spain

- 8.3.5 France

- 8.3.6 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Taiwan

- 8.5 Rest of World

Chapter 9 Company Profiles

- 9.1 AEGIS

- 9.2 AIG

- 9.3 Allianz

- 9.4 Aon

- 9.5 AXA

- 9.6 AXIS Capital Holdings Limited

- 9.7 Canopius

- 9.8 Chubb

- 9.9 Descartes Underwriting

- 9.10 Energy Insurance Mutual Limited

- 9.11 Fairfax Financial Holdings Limited

- 9.12 Gallagher

- 9.13 HDI Global

- 9.14 Horton Group

- 9.15 kWh Analytics

- 9.16 Liberty Specialty Markets

- 9.17 Markel Group Inc.

- 9.18 Marsh & McLennan Companies, Inc.

- 9.19 Miller

- 9.20 Munich Re

- 9.21 Ping An Insurance (Group) Company of China, Ltd.

- 9.22 PICC

- 9.23 RSA Insurance

- 9.24 Swiss Re

- 9.25 Tokio Marine Kiln

- 9.26 Travelers

- 9.27 Willis Towers Watson (WTW)

- 9.28 Zurich Insurance