PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045670

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045670

AI Foundation Model for Automotive Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

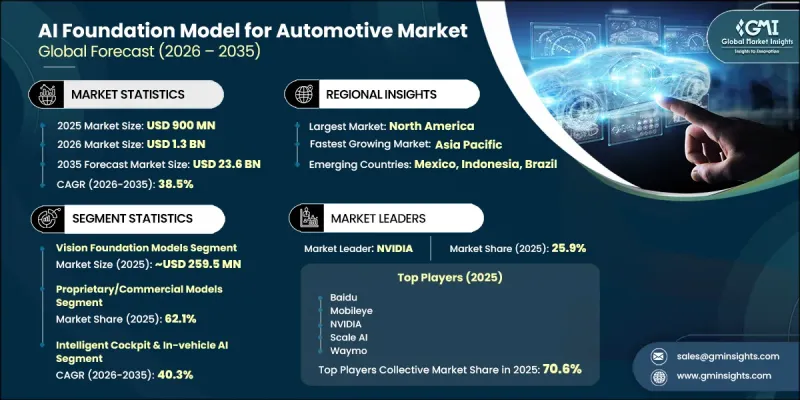

The Global AI Foundation Model for Automotive Market was valued at USD 900 million in 2025 and is estimated to grow at a CAGR of 38.5% to reach USD 23.6 billion by 2035.

The market is advancing rapidly as automotive manufacturers continue transitioning artificial intelligence technologies from pilot deployments to large-scale commercial integration. Increasing adoption of advanced driver assistance systems across mass-market vehicle categories is accelerating demand for AI foundation models capable of supporting perception, planning, and autonomous decision-making functions. Significant investments in AI training infrastructure, vehicle computing platforms, and large-scale data management operations are further strengthening market expansion. Growing emphasis on road safety, operational reliability, and vehicle automation is encouraging continuous software and model upgrades throughout the vehicle lifecycle. Regulatory developments are also playing a major role in industry growth, as authorities continue introducing stricter standards related to intelligent driving technologies and automated safety systems. In addition, advancements in low-power automotive computing hardware and synthetic data generation technologies are helping manufacturers improve validation efficiency, reduce deployment costs, and accelerate the commercialization of AI-powered automotive platforms across passenger, commercial, and fleet vehicle segments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $900 Million |

| Forecast Value | $23.6 Billion |

| CAGR | 38.5% |

Advancements in automotive-grade AI accelerators are significantly improving the performance capabilities of modern autonomous systems. High-performance processing platforms are now capable of delivering hundreds to thousands of TOPS while operating under relatively low power consumption levels, enabling real-time perception and vehicle planning functions without creating excessive hardware costs. At the same time, synthetic data development pipelines are helping automotive companies lower testing and validation expenses associated with complex driving scenarios that are difficult to reproduce in physical environments. These technological improvements are reducing the time required to move AI foundation models from development stages to certified deployment, particularly in operational environments where measurable safety validation is critical for commercial implementation.

The vision foundation models segment accounted for 22.5% share in 2025. Large-scale transformer-based models trained on extensive driving datasets are increasingly being used to support vehicle perception, environmental interpretation, and driving decision functions. These systems reduce dependency on heavily engineered interfaces and simplify development processes, helping manufacturers shorten validation timelines and improve operational efficiency within controlled deployment environments. The growing ability of foundation models to manage multiple autonomous driving tasks simultaneously continues to strengthen their adoption across next-generation automotive systems.

The proprietary and commercial models segment held 62.1% share in 2025 and generated USD 575.1 million. Automotive manufacturers continue to favor proprietary AI platforms due to their validated performance, long-term support capabilities, and clearly defined accountability structures. Regulatory authorities evaluating automated driving technologies increasingly require extensive documentation, performance verification, and scenario-based safety evidence, which benefits companies capable of delivering fully integrated solutions supported by advanced tooling, compliance frameworks, and warranty-backed service models. This preference for commercially supported platforms is expected to continue driving investment across the AI foundation model for the automotive industry.

U.S. AI Foundation Model for Automotive Market reached USD 490.6 million in 2025 and is projected to grow at a CAGR of 38.8% from 2026 to 2035. The United States remains one of the leading regions for the commercialization of advanced autonomous driving technologies due to rapid technological innovation and early adoption of AI-powered mobility solutions. Increasing deployment of higher-level autonomous driving capabilities across modern vehicle platforms is supporting strong market growth throughout the country. Continued investments in autonomous vehicle development, advanced software ecosystems, and intelligent transportation technologies are positioning the United States as a key innovation hub within the global AI foundation model for automotive market. Strong research activity and commercialization initiatives are expected to further strengthen the country's leadership position in advanced vehicle automation technologies during the forecast period.

Major companies operating in the Global AI Foundation Model for Automotive Market include Aurora Innovation, Baidu, Bosch, Mobileye, Momenta, NVIDIA, Scale AI, Tesla, Waymo, and Xpeng Motors. Companies operating in the AI foundation model for the automotive market are adopting multiple strategic initiatives to strengthen their market position and expand commercial adoption. Leading players are investing heavily in artificial intelligence research, large-scale training infrastructure, and high-performance automotive computing platforms to improve autonomous driving capabilities and model accuracy. Strategic partnerships with automotive manufacturers, semiconductor providers, and mobility technology companies are helping accelerate product integration and commercialization efforts. Companies are also focusing on proprietary software ecosystems, synthetic data generation technologies, and advanced simulation platforms to improve validation efficiency and reduce deployment timelines.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Model Capability

- 2.2.3 Licensing

- 2.2.4 Deployment

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand for Vehicle Safety and Accident Reduction

- 3.2.1.2 Regulatory Mandates for Advanced Driver Assistance Systems

- 3.2.1.3 Adoption of autonomous driving & ADAS foundation models

- 3.2.1.4 Increasing integration of generative AI in connected vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Computational Requirements for Real-Time Inference

- 3.2.2.2 Data Privacy Concerns and Cross-Border Data Transfer Restrictions

- 3.2.3 Market opportunities

- 3.2.3.1 Synthetic Data Generation for Long-Tail Scenario Coverage

- 3.2.3.2 Foundation Model Compression and Edge Optimization Techniques

- 3.2.3.3 Expansion into Intelligent Cockpit and In-Vehicle AI Applications

- 3.2.1 Growth drivers

- 3.3 Technology and innovation landscape

- 3.3.1 Current technological trends

- 3.3.1.1 Transformer-Based Perception Models

- 3.3.1.2 Multimodal Sensor Fusion Systems

- 3.3.1.3 Edge AI Inference Platforms

- 3.3.2 Emerging technologies

- 3.3.2.1 Generative World Models for Autonomous Navigation

- 3.3.2.2 Synthetic Data Generation Engines

- 3.3.1 Current technological trends

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 US - National Highway Traffic Safety Administration

- 3.5.1.2 Canada - Transport Canada

- 3.5.2 Europe

- 3.5.2.1 EU - The Directorate-General for Mobility and Transport (DG MOVE)

- 3.5.2.2 Germany - Federal Motor Transport Authority - KBA

- 3.5.3 Asia Pacific

- 3.5.3.1 China - Ministry of Industry and Information Technology (MIIT)

- 3.5.3.2 Japan - Ministry of Land, Infrastructure, Transport and Tourism (MLIT)

- 3.5.4 LATAM

- 3.5.4.1 Brazil - National Traffic Secretariat (SENATRAN)

- 3.5.4.2 Chile - Ministry of Transport and Telecommunications

- 3.5.5 MEA

- 3.5.5.1 South Africa - SASO

- 3.5.5.2 UAE - Roads and Transport Authority - RTA

- 3.5.1 North America

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Multimodal foundation models for driving intelligence

- 3.11.1 Vision-Language Model Integration in Autonomous Systems

- 3.11.2 Sensor Fusion Foundation Models (Camera-LiDAR-Radar)

- 3.11.3 Natural Language Interface for Vehicle Control

- 3.12 OEM vs Tier-1 vs AI platform power shift

- 3.12.1 Tier-1 Supplier Repositioning Strategies

- 3.12.2 Tech Giants’ Entry and Ecosystem Control Dynamics

- 3.12.3 Open-Source vs Proprietary Platform Competition

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case- Key Macro & Industry Variables Driving CAGR

- 3.13.2 Optimistic Scenarios- Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates and Forecast, By Model Capability, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Multimodal Large Language Models (MLLMs)

- 5.3 World Foundation Models

- 5.4 Vision Foundation Models

- 5.5 Generative Models for Synthetic Data

- 5.6 End-to-End Autonomous Driving Models

- 5.7 3D Scene Reconstruction Models

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Licensing, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Open-Source Models

- 6.3 Proprietary/Commercial Models

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By Deployment, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Cloud-Based Models

- 7.3 Edge/On-Vehicle Models

- 7.4 Hybrid Models

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Autonomous Vehicle Planning & Operations

- 8.2.1 Robotaxi Services

- 8.2.2 Autonomous Delivery & Freight

- 8.3 Intelligent Cockpit & In-Vehicle AI

- 8.4 Consumer ADAS

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Autonomous Vehicle Operators

- 9.4 Tier-1 Automotive Suppliers

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 United Kingdom

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.3.7 Sweden

- 10.3.8 Switzerland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 South Korea

- 10.4.4 India

- 10.4.5 Singapore

- 10.4.6 Australia

- 10.4.7 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Chile

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 NVIDIA

- 11.1.2 Tesla

- 11.1.3 Waymo

- 11.1.4 Liquid AI

- 11.1.5 Baidu

- 11.1.6 General Motors

- 11.1.7 Mobileye

- 11.1.8 Scale AI

- 11.1.9 Zoox

- 11.1.10 Toyota Motor

- 11.1.11 Volkswagen

- 11.1.12 Bosch

- 11.1.13 Qualcomm Technologies

- 11.1.14 Aurora Innovation

- 11.2 Regional players

- 11.2.1 Xpeng Motors

- 11.2.2 Momenta

- 11.2.3 Li Auto

- 11.3 Emerging players

- 11.3.1 Nuro

- 11.3.2 PlusAI

- 11.3.3 Waabi