PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045713

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045713

Automotive TIC Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

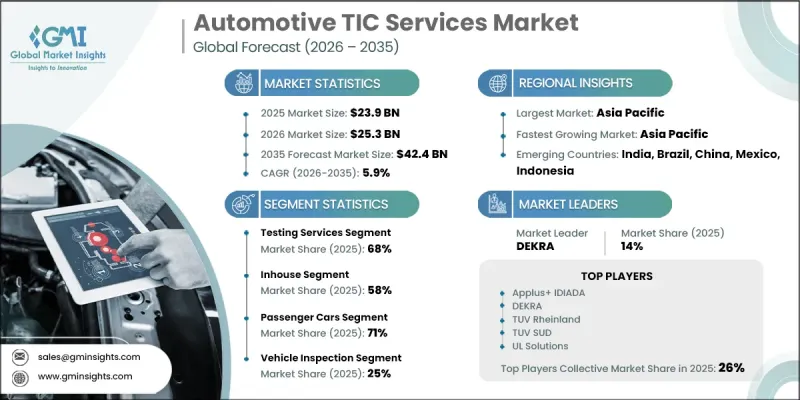

The Global Automotive TIC Services Market was valued at USD 23.9 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 42.4 billion by 2035.

The market is expanding as regulatory authorities continue to enforce stricter standards related to vehicle safety, emissions control, and cybersecurity requirements, increasing the reliance on testing, inspection, and certification services. The globalization of automotive manufacturing and supply chains is further driving the need for standardized compliance frameworks across multiple regions. Rapid advancements in electric mobility are strengthening demand for specialized validation capabilities, particularly in areas such as battery performance, thermal efficiency, and charging systems. At the same time, the growing integration of advanced software systems in vehicles is shifting industry focus toward continuous validation processes for connected and intelligent technologies. Digital transformation within the sector is also influencing testing methodologies, with advanced simulation tools improving efficiency and reducing development timelines. In addition, commercial fleet operators are increasingly leveraging TIC services to enhance operational reliability, ensure compliance, and optimize performance, contributing to sustained market growth across the automotive ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $23.9 Billion |

| Forecast Value | $42.4 Billion |

| CAGR | 5.9% |

The testing services segment accounted for 68% share in 2025 and is expected to grow at a CAGR of 5.4% from 2026 to 2035. These services focus on assessing vehicle systems, components, and complete units under both controlled and operational environments to ensure adherence to safety, performance, and emission requirements. The scope includes multiple validation processes designed to support regulatory approvals and maintain product reliability.

The in-house segment held a share of 58% in 2025 and is projected to grow at a CAGR of 4.9% through 2035. Internal TIC capabilities enable automotive manufacturers to retain full control over testing and certification workflows, resulting in faster execution, improved data security, and better alignment with internal development processes. However, such capabilities require substantial investments in advanced infrastructure, technical expertise, and continuous system upgrades, making them more viable for large-scale manufacturers with consistent testing needs.

U.S. Automotive TIC Services Market reached USD 5.1 billion in 2025 and is expected to grow at a CAGR of 6.3% between 2026 and 2035. Market growth is supported by a strong regulatory environment that emphasizes safety, emissions compliance, and advanced vehicle validation requirements. Increasing focus on electric vehicle safety standards and evolving compliance frameworks are further strengthening demand for comprehensive TIC services across the country.

Key companies operating in the Automotive TIC Services Market include Applus+, Bureau Veritas, CATARC, DEKRA, Element Materials Technology, Eurofins, Intertek, SGS, TUV Rheinland, TUV SUD, and UL Solutions. Companies in the Automotive TIC Services Market are adopting a range of strategic initiatives to reinforce their competitive positioning and expand their market footprint. They are increasing investments in advanced testing infrastructure, particularly for electric vehicles, connected systems, and emerging automotive technologies. Strategic partnerships and collaborations with automotive manufacturers are being pursued to accelerate innovation and ensure early integration into development cycles. Firms are also expanding their global presence to support multinational clients and meet regional compliance requirements efficiently. Emphasis on digitalization, including the adoption of simulation tools and data-driven testing methods, is improving operational efficiency and reducing turnaround times.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Sourcing

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent regulatory compliance

- 3.2.1.2 Globalization of the automotive industry

- 3.2.1.3 Rising demand for vehicle performance testing

- 3.2.1.4 Consumer demand for quality assurance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced TIC equipment

- 3.2.2.2 Complex regulatory environment

- 3.2.3 Market opportunities

- 3.2.3.1 Growth opportunities in emerging markets

- 3.2.3.2 Development of electric and autonomous vehicles

- 3.2.3.3 Expansion of commercial vehicle TIC services

- 3.2.3.4 Integration of advanced technologies in TIC services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis (Driven by Primary Research)

- 3.5.1 Historical price trend analysis

- 3.5.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 National Highway Traffic Safety Administration

- 3.6.1.2 Environmental Protection Agency

- 3.6.2 Europe

- 3.6.2.1 European Commission

- 3.6.2.2 United Nations Economic Commission for Europe

- 3.6.3 Asia Pacific

- 3.6.3.1 Ministry of Industry and Information Technology

- 3.6.3.2 Ministry of Road Transport and Highways

- 3.6.4 Latin America

- 3.6.4.1 Agencia Nacional de Transportes Terrestres

- 3.6.4.2 Secretaria de Infraestructura, Comunicaciones y Transportes

- 3.6.5 Middle East & Africa

- 3.6.5.1 Saudi Standards, Metrology and Quality Organization

- 3.6.5.2 National Regulator for Compulsory Specifications

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 Gen AI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by primary research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Testing services

- 5.3 Inspection services

- 5.4 Certification services

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Sourcing, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 In-house

- 6.3 Outsourced

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Vehicle inspection

- 8.3 Emission testing

- 8.4 Component testing

- 8.5 Telematics

- 8.6 ADAS

- 8.7 Homologation testing

- 8.8 Fuels, fluids and lubricants

- 8.9 Electric systems and components

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.3.8 Poland

- 9.3.9 Romania

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.4.8 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Bureau Veritas

- 10.1.2 DEKRA

- 10.1.3 Eurofins Scientific

- 10.1.4 Element Materials Technology

- 10.1.5 Intertek

- 10.1.6 SGS

- 10.1.7 TUV Rheinland

- 10.1.8 TUV SUD

- 10.1.9 UL Solutions

- 10.2 Regional players

- 10.2.1 Applus+ IDIADA

- 10.2.2 Automotive Research Association of India

- 10.2.3 CATARC

- 10.2.4 China Automotive Technology and Research Center

- 10.2.5 Japan Automobile Research Institute

- 10.2.6 Korea Testing Laboratory

- 10.2.7 SOCOTEC

- 10.2.8 TUV NORD

- 10.3 Emerging players

- 10.3.1 ALS

- 10.3.2 CSA

- 10.3.3 MISTRAS