PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045826

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045826

Industrial Hydrogen Energy Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

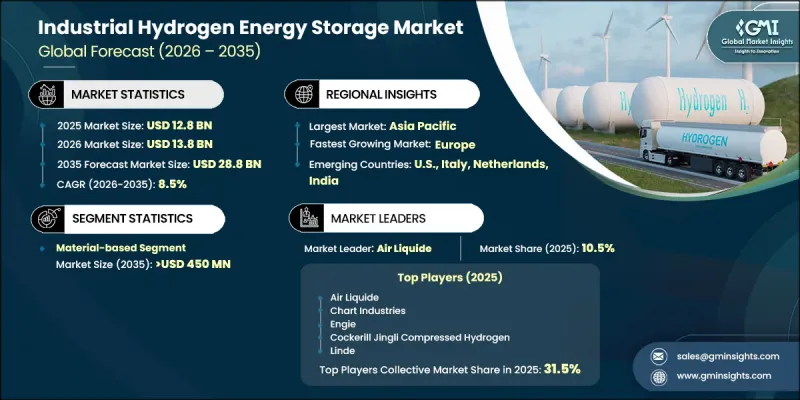

The Global Industrial Hydrogen Energy Storage Market was valued at USD 12.8 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 28.8 billion by 2035.

Growth in the industrial hydrogen energy storage industry is driven by the accelerating global shift toward decarbonization and the rising need for efficient renewable energy integration solutions. Hydrogen is increasingly being recognized as a clean and flexible energy carrier that supports emissions reduction across power generation, manufacturing, transportation, and heavy industry applications. Expanding renewable energy penetration is also increasing demand for long-duration storage systems capable of balancing intermittent power supply. Technological advancements in hydrogen storage, including high-pressure containment systems, cryogenic technologies, and solid-state storage innovations, are improving efficiency, safety, and scalability. Rising investments in hydrogen production facilities, storage infrastructure, and distribution networks are further strengthening market development. Governments and private stakeholders are actively supporting hydrogen economy frameworks through funding initiatives, policy incentives, and large-scale infrastructure projects. Integration of hydrogen storage with solar and wind energy systems is also enhancing grid stability and energy reliability, positioning hydrogen as a key enabler of future clean energy systems across global industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.8 Billion |

| Forecast Value | $28.8 Billion |

| CAGR | 8.5% |

The material-based segment is expected to reach USD 450 million by 2035. Continuous innovation in hydrogen storage materials is significantly contributing to this segment's expansion, with growing development of advanced compounds such as metal hydrides, chemical hydrides, and complex hydride systems. These materials are gaining attention due to their high storage density, stability, and ability to improve overall system efficiency. Advancements in material science are enhancing hydrogen absorption and release performance, making storage systems more reliable and commercially viable for large-scale industrial applications. Ongoing research and development efforts are further improving cost efficiency and operational safety in hydrogen storage technologies.

U.S. Industrial Hydrogen Energy Storage Market is projected to reach USD 4.2 billion by 2035. Market expansion in the United States is supported by strong federal policy frameworks, rising clean energy investments, and growing demand for sustainable industrial energy solutions. Incentive programs under national clean energy legislation are accelerating the development of hydrogen production and storage infrastructure. The presence of large-scale industrial sectors such as refining, chemicals, and metallurgy is further driving demand for efficient hydrogen storage systems. In addition, the rapid expansion of renewable energy capacity is increasing the need for long-duration storage technologies to ensure grid stability. Public-private collaborations and large-scale hydrogen hub initiatives are further strengthening deployment across the country, positioning the U.S. as a leading growth market.

Key companies operating in the Global Industrial Hydrogen Energy Storage Market include Air Liquide, Linde plc, Air Products and Chemicals, Inc., ENGIE, Plug Power Inc., Nel ASA, ITM Power PLC, McPhy Energy S.A., Chart Industries, Worthington Industries, Hexagon Purus ASA, FuelCell Energy, Inc., Everfuel A/S, NPROXX B.V., Cockerill Jingli Compressed Hydrogen, GKN Compressed Hydrogen, SSE, and Gravitricity Ltd. Companies operating in the industrial hydrogen energy storage market are adopting multiple strategies to strengthen their competitive position and expand global reach. Leading players are heavily investing in research and development to improve hydrogen storage efficiency, safety, and scalability across industrial applications. Strategic partnerships with energy utilities, industrial manufacturers, and renewable energy developers are enabling companies to accelerate project deployment and expand infrastructure networks. Firms are also focusing on large-scale hydrogen hub developments and integrated storage solutions linked with wind and solar energy systems. Expansion of manufacturing capacity and localization of supply chains are helping reduce production costs and improve accessibility. In addition, companies are actively engaging in government-backed clean energy programs and policy-driven initiatives to secure long-term contracts.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Method trends

- 2.1.3 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Capacity & production landscape (Driven by Primary Research)

- 3.7.1 Capacity by key producer (Driven by Primary Research)

- 3.7.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

- 3.8 Impact of AI & Generative AI on the market (Core Solution)

- 3.8.1 AI-Driven production optimization (Core Solution)

- 3.8.2 Predictive maintenance & fault detection (Core Solution)

- 3.9 Emerging opportunities & trends

- 3.10 Investment analysis & future prospects

- 3.11 Sustainability initiatives & industry 4.0 integration

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Key developments

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive positioning matrix

Chapter 5 Market Size and Forecast, By Method, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Compression

- 5.3 Liquefaction

- 5.4 Material based

Chapter 6 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Netherlands

- 6.3.6 Russia

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.5 Rest of World

Chapter 7 Company Profiles

- 7.1 Air Liquide

- 7.2 Air Products and Chemicals, Inc.

- 7.3 Chart Industries

- 7.4 Cockerill Jingli Compressed hydrogen

- 7.5 ENGIE

- 7.6 Everfuel A/S

- 7.7 FuelCell Energy, Inc.

- 7.8 GKN Compressed Hydrogen

- 7.9 Gravitricity Ltd

- 7.10 Hexagon Purus ASA

- 7.11 ITM Power PLC

- 7.12 Linde plc

- 7.13 McPhy Energy S.A.

- 7.14 Nel ASA

- 7.15 NPROXX B.V.

- 7.16 Plug Power Inc.

- 7.17 SSE

- 7.18 Worthington Industries