PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045873

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045873

Commercial Recycling Bins Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

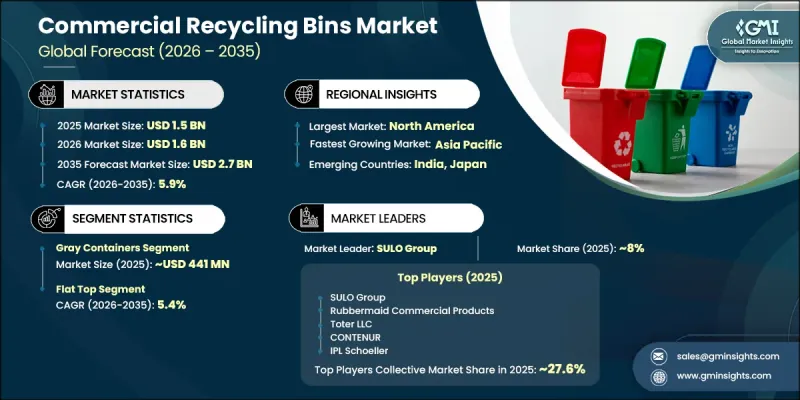

The Global Commercial Recycling Bins Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 2.7 billion by 2035.

Market growth is supported by strict environmental regulations and mandatory waste segregation policies implemented across commercial sectors worldwide. Governments across North America, Europe, and several Asia Pacific economies are introducing aggressive waste diversion and sustainability targets that require businesses, educational facilities, healthcare institutions, and retail establishments to adopt dedicated recycling infrastructure. These regulatory initiatives are creating steady procurement demand for commercial recycling bins across multiple end-use industries. Expanding adoption of circular economy practices and extended producer responsibility frameworks is also encouraging broader investment in organized waste management systems across both existing and newly developed facilities. In addition, rapid expansion of commercial real estate and institutional infrastructure is contributing significantly to market growth. New office buildings, retail developments, healthcare centers, and educational campuses increasingly integrate commercial recycling bins as a standard component of sustainable facility planning. Property developers and facility operators are prioritizing durable, visually coordinated recycling systems to support green building certifications and long-term environmental compliance objectives. Rising construction activity across emerging economies is further expanding growth opportunities for the commercial recycling bins market worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.7 Billion |

| CAGR | 5.9% |

The gray containers segment generated USD 441 million in 2025 and is projected to grow at a CAGR of 4.1% from 2026 to 2035. Gray recycling containers continue to maintain a leading market position due to their extensive use for collecting general waste and mixed recyclable materials across a wide range of commercial facilities. These bins are widely utilized in retail stores, healthcare environments, office buildings, educational institutions, and commercial establishments where versatile waste collection systems are required to support standardized waste segregation practices. Their compatibility with established waste management systems and color-coded disposal frameworks across mature commercial markets continues to strengthen adoption and deployment volumes globally.

The flat top segment accounted for USD 675.7 million in 2025 and is expected to grow at a CAGR of 5.4% through 2035. Flat top recycling bins continue to dominate the commercial recycling bins market because of their practical design advantages and operational convenience within commercial environments. These bins offer efficient storage capabilities and can be easily stacked or repositioned when facilities require flexible waste management arrangements. Their design also supports clear labeling, instructional displays, and color-coded identification systems that help improve waste segregation efficiency among users. Growing preference for space-saving and visually organized recycling solutions across commercial properties is further supporting demand for flat top recycling bins.

U.S. Commercial Recycling Bins Market was valued at USD 586.8 million in 2025 and is anticipated to register a CAGR of 5.6% between 2026 and 2035. North America continues to represent the largest regional market for commercial recycling bins due to comprehensive environmental regulations, strong commercial construction activity, and highly developed institutional waste management infrastructure. The United States maintains a dominant position within the region because of its large commercial real estate sector and extensive presence of retail establishments, corporate offices, educational institutions, and public facilities requiring standardized recycling systems. Increasing emphasis on sustainability initiatives and organized waste collection programs continues to support long-term market growth across the country.

Major companies operating in the Global Commercial Recycling Bins Market include Rubbermaid Commercial Products, Bigbelly, Inc., Busch Systems International Inc., Toter LLC, Orbis Corporation, SULO Group, and SSI Schaefer Waste among leading global participants. Key regional companies include Glasdon International Limited, Otto Environmental Systems North America, Inc., Rehrig Pacific Company, ESE World B.V., Molok Ltd, CONTENUR, and Craemer Group. Emerging and specialized market participants include Commercial Zone Products, Carlisle FoodService Products, Witt Industries, Rossignol, Cascade Engineering, Continental Commercial Products, and IPL Schoeller. Companies operating in the Commercial Recycling Bins Market are focusing on multiple strategic initiatives to strengthen competitive positioning and expand market presence. Leading manufacturers are investing in product innovation to develop durable, aesthetically appealing, and sustainable recycling bin solutions that align with evolving environmental regulations and commercial facility requirements. Many companies are integrating smart waste management technologies, including sensor-based monitoring systems and automated collection tracking features, to improve operational efficiency and waste handling performance. Strategic partnerships with commercial property developers, municipalities, and waste management service providers are also helping businesses secure long-term contracts and expand distribution networks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Model

- 2.2.4 Material

- 2.2.5 End Use

- 2.2.6 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Stringent environmental regulations and mandatory recycling policies across commercial sectors

- 3.2.1.2 Rapid growth of commercial real estate and expansion of institutional facilities

- 3.2.1.3 Rising corporate sustainability commitments and ESG reporting requirements

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High upfront cost of durable materials and weatherproofing for commercial-grade bins

- 3.2.2.2 Lack of standardized color-coding and waste stream labeling across jurisdictions

- 3.2.3 Opportunities

- 3.2.3.1 Growing adoption of smart and sensor-enabled recycling bins with fill-level monitoring

- 3.2.3.2 Expansion into high-growth emerging markets with developing waste management infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.9.3 Regional price variations

- 3.10 Trade data analysis (HS code for metal bins- 7323.99) (driven by paid database)

- 3.10.1 Import/export volume and value trends (driven by paid database)

- 3.10.2 Key trade corridors and tariff impact (driven by paid database)

- 3.10.3 Regional trade dependencies

- 3.11 Impact of AI and generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases and adoption roadmap by segment

- 3.11.3 Risks, limitations and regulatory considerations

- 3.12 Capacity and production landscape (driven by primary research)

- 3.12.1 Installed capacity by region and key producer (driven by primary research)

- 3.12.2 Capacity utilization rates and expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Green Containers

- 5.3 Blue Containers

- 5.4 Gray Containers

- 5.5 Others (Brown, Yellow, etc.)

Chapter 6 Market Estimates & Forecast, By Model, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Dome Top

- 6.3 Flat Top

- 6.4 Hood Top

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Metals

- 7.2.1 Steel & Stainless Steel

- 7.2.2 Aluminum

- 7.3 Plastics

- 7.3.1 Polyethylene

- 7.3.2 Polypropylene (PP)

- 7.3.3 Polyethylene Terephthalate (PET)

- 7.3.4 Acrylonitrile Butadiene Styrene (ABS)

- 7.3.5 Fiberglass

- 7.3.6 Others (Polycarbonate (PC), Galvanized Steel)

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Supermarkets

- 8.3 Department Stores

- 8.4 Cafes and Coffee Shops

- 8.5 Educational Institutes

- 8.6 Offices

- 8.7 Retail Stores

- 8.8 Hospitals

- 8.9 Others (Convenience Stores, Specialty Stores, Parks, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct Sales

- 9.3 Indirect Sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Top Global Players

- 11.1.1 Rubbermaid Commercial Products

- 11.1.2 Bigbelly, Inc.

- 11.1.3 Busch Systems International Inc.

- 11.1.4 Toter LLC

- 11.1.5 Orbis Corporation

- 11.1.6 SULO Group

- 11.1.7 SSI Schaefer Waste

- 11.2 Regional Champions

- 11.2.1 Glasdon International Limited

- 11.2.2 Otto Environmental Systems, Inc.

- 11.2.3 Rehrig Pacific Company

- 11.2.4 ESE World B.V.

- 11.2.5 Molok Ltd

- 11.2.6 CONTENUR

- 11.2.7 Craemer Group

- 11.3 Emerging & Specialized Players

- 11.3.1 Commercial Zone Products

- 11.3.2 Carlisle FoodService Products

- 11.3.3 Witt Industries

- 11.3.4 Rossignol

- 11.3.5 Cascade Engineering

- 11.3.6 Continental Commercial Products

- 11.3.7 IPL Schoeller