PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065777

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065777

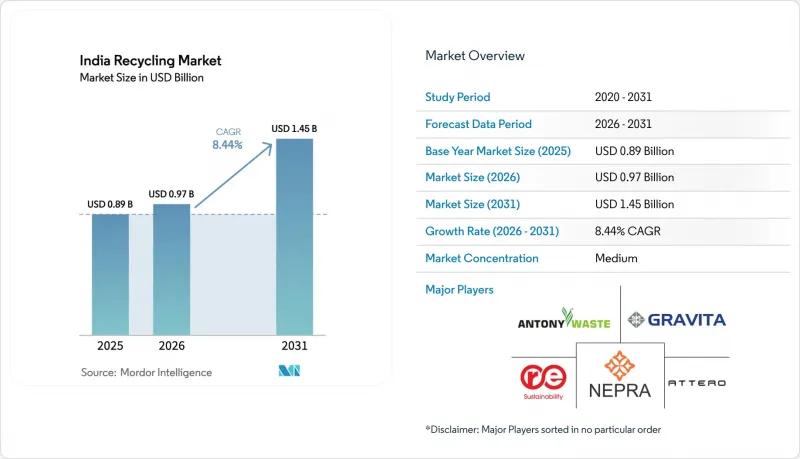

India Recycling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india recycling market size was valued at USD 0.89 billion in 2025 and is estimated to grow from USD 0.97 billion in 2026 to reach USD 1.45 billion by 2031, at a CAGR of 8.44% during the forecast period (2026-2031).

This report is Segmented by Material Type (Plastics, Metals, Paper and Cardboard, Glass, and Others), Source (Municipal, Industrial, Medical Waste, Construction Waste, and Other Sources), Technology (Mechanical Recycling, Chemical Recycling, Biological Recycling, and Other Technologies), and Geography (India). The Market Forecasts are Provided in Terms of Value (USD).

India Recycling Market Trends and Insights

Extended EPR Mandates Across Plastics and Electronics

Plastic Waste Management Rules 2022 and E-Waste Management Rules 2022 impose 60% e-waste collection for 2025-2026, rising to 80% by 2027-2028, and 70% lithium-ion battery recovery by 2027-2028. Environmental compensation levies range from Rs 5,000 to Rs 20,000 per ton, turning non-compliance into a costly option. Credit prices fluctuate between Rs 8 and Rs 25 per kilogram, depending on the polymer grade and regional supply and demand. Maharashtra and Tamil Nadu conduct quarterly audits that encourage organized recyclers to transition toward ISO 14001-certified recovery facilities. Battery rules compel electric-vehicle OEMs to establish closed-loop networks, accelerating reverse-logistics partnerships with Attero and Gravita.

Rising Urban MSW Volumes and Landfill Shortages

India produces 160,000-170,000 tons of municipal solid waste (MSW) daily, yet only 474 of the 2,421 legacy landfills have been remediated under the Swachh Bharat Mission 2.0. Tipping fees in land-scarce metros exceed Rs 800-Rs 1,200 per ton, making recycling more economical than dumping. Central allocations of Rs 1,41,600 crore (USD 17 billion) through 2026 fund material recovery and waste-to-energy plants. However, source segregation remains below 30% in tier-2 cities, resulting in polymer recovery yields of 40-50% compared to 70-80% for segregated streams. Decentralized processors such as Saahas Zero Waste deploy micro-composters that bypass municipal bottlenecks.

Fragmented, Informal Collection Ecosystem

Informal picker networks handle 60-70% of first-mile collection in smaller cities, operating outside tax and labor frameworks. This curtails traceability, undermining ISO 14021 self-declarations sought by brand owners. Formal recyclers pay 15-25% more for feedstock because informal agents circumvent compliance costs. Municipal pilot programs offering IDs, insurance, and fixed prices cover under 20% of workers due to bureaucratic delays. Contamination rates of 20-30% force extra washing and raise processing costs.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Recycled-Content Demand from FMCG and Packaging Majors

- Fiscal Incentives and Lithium-Ion Battery End-of-Life Wave

- Limited Domestic End-Markets for Lower-Grade Recyclate & Scrap Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics currently account for 36.86% of India's recycling market share, yet slower packaging growth and mono-material design are limiting volumes. Attero's USD 76 million raise underscores confidence in battery-metal loops, while premium rPET from chemical recyclers satisfies Coca-Cola India's multi-year off-takes. Paper recycling leverages e-commerce corrugate demand, and tire pyrolysis expands the niche for "other materials." Metals are expected to grow at a 8.94% CAGR to 2031, driven by soaring end-of-life battery flows that are projected to reach 600,000 tons.

The Indian recycling market size for metals is poised to grow as integrated producers such as Hindustan Zinc and Gravita India integrate scrap operations into primary smelting. Plastics retain scale advantages but face pressure from the value chain to deliver food-contact compliance. Premium chemical-route polymers command a double margin over mechanically recycled grades, incentivizing capacity additions in Gujarat and Tamil Nadu. Glass and composites remain small due to high logistics costs and low cullet demand.

List of Companies Covered in this Report:

- A2Z Group

- Antony Waste Handling Cell Limited

- Attero

- Cerebra Integrated Technologies Ltd.

- Dalmia Polypro Industries Pvt. Ltd.

- Eco Recycling

- Gravita India

- Greenko Group

- Hindustan Zinc

- NEST

- Ramky Enviro Engineers

- Rapidue Technologies Pvt. Ltd.

- Saahas Zero Waste

- Sampurn(e)arth Environment Solutions Pvt. Ltd.

- The Shakti Plastic Industries

- UltraTech Cement Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Extended EPR mandates across plastics and electronics

- 4.2.2 Rising urban MSW volumes and landfill shortages

- 4.2.3 Surge in recycled-content demand from FMCG and packaging majors

- 4.2.4 Fiscal incentives (GST concessions, PLI) for recycling plants

- 4.2.5 Lithium-ion battery end-of-life wave from Electric Vehicle adoption

- 4.3 Market Restraints

- 4.3.1 Fragmented, informal collection ecosystem

- 4.3.2 Limited domestic end-markets for lower-grade recycled polymers

- 4.3.3 Volatility in scrap prices linked to global commodity cycles

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Plastics

- 5.1.2 Metals

- 5.1.3 Paper and Cardboard

- 5.1.4 Glass

- 5.1.5 Others

- 5.2 By Source

- 5.2.1 Municipal (Residential and Commercial)

- 5.2.2 Industrial

- 5.2.3 Medical Waste

- 5.2.4 Construction Waste

- 5.2.5 Other Sources

- 5.3 By Technology

- 5.3.1 Mechanical Recycling

- 5.3.2 Chemical Recycling

- 5.3.3 Biological Recycling

- 5.3.4 Other Technologies

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 A2Z Group

- 6.4.2 Antony Waste Handling Cell Limited

- 6.4.3 Attero

- 6.4.4 Cerebra Integrated Technologies Ltd.

- 6.4.5 Dalmia Polypro Industries Pvt. Ltd.

- 6.4.6 Eco Recycling

- 6.4.7 Gravita India

- 6.4.8 Greenko Group

- 6.4.9 Hindustan Zinc

- 6.4.10 NEST

- 6.4.11 Ramky Enviro Engineers

- 6.4.12 Rapidue Technologies Pvt. Ltd.

- 6.4.13 Saahas Zero Waste

- 6.4.14 Sampurn(e)arth Environment Solutions Pvt. Ltd.

- 6.4.15 The Shakti Plastic Industries

- 6.4.16 UltraTech Cement Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment