PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061305

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061305

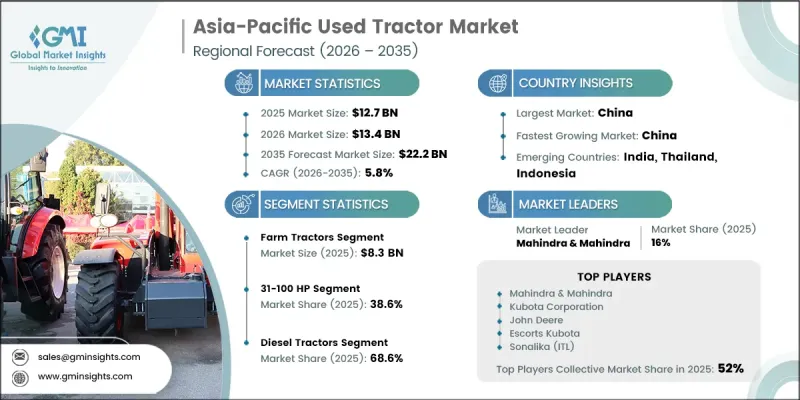

Asia-Pacific Used Tractor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

Asia-Pacific Used Tractor Market was valued at USD 12.7 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 22.2 billion by 2035.

The market growth is influenced by the rising need for affordable agricultural mechanization solutions across the region. Increasing pressure on farm productivity, coupled with the shift toward cost-efficient farming practices, is driving consistent demand for pre-owned agricultural machinery. Rapid urbanization is also contributing to changing land use patterns, which indirectly supports demand for efficient and economical farming equipment. Farmers are increasingly prioritizing reliable machinery that can deliver performance at lower investment levels, encouraging steady expansion of the used tractor market. In addition, the growing emphasis on agricultural modernization and productivity enhancement is prompting continuous upgrades in farm equipment usage. The rise of digital platforms for equipment transactions has also improved market accessibility, allowing buyers and sellers to connect more efficiently. Improvements in refurbishment quality and inspection standards are further strengthening consumer trust, making used tractors a viable alternative to new equipment across both small and large farming operations in Asia-Pacific.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $12.7 Billion |

| Forecast Value | $22.2 Billion |

| CAGR | 5.8% |

The farm tractors segment accounted for a 65.6% share in 2025, generating USD 8.3 billion. This segment remains dominant due to its extensive use in core agricultural activities and its importance in enhancing farm productivity. Demand for these tractors is primarily driven by their ability to support essential farming operations such as cultivation, plowing, and general field management. Their versatility, durability, and adaptability across different farm sizes have made them a preferred choice among agricultural users seeking dependable machinery at lower costs. Continuous improvements in tractor specifications and functional efficiency have further strengthened their role in modern farming practices.

The 31-100 HP segment held a share of 38.6% in 2025, valued at USD 4.9 billion. This horsepower category leads the market due to its balanced performance, operational efficiency, and affordability. It offers sufficient power to handle a wide range of agricultural tasks while maintaining manageable fuel and maintenance costs. Farmers prefer this range for its adaptability across multiple applications, including hauling, soil preparation, and implement operations. Enhanced compatibility with attachments and improved mechanical configurations have further increased its adoption among farming communities.

China Used Tractor Market held a 30.1% share and generated USD 3.8 billion in 2025. The country's strong position is supported by its large agricultural base and continuous advancement in farming practices. Increasing adoption of mechanized farming solutions and rising demand for cost-effective agricultural equipment are key growth drivers. The market is further strengthened by an established distribution ecosystem and growing preference for quality-assured pre-owned tractors. Ongoing modernization of agricultural operations continues to sustain strong demand momentum in the country, supported by consistent improvements in farm efficiency and equipment utilization.

Key players operating in the Asia-Pacific Used Tractor Market include John Deere, Mahindra & Mahindra, Kubota Corporation, CNH Industrial, Escorts Kubota, TAFE, Yanmar, Sonalika, LS Mtron, VST Tillers Tractors, Foton Agricultural, Lovol, Kioti, Swaraj, Indo Farm Equipment, YTO Group, Kukje Machinery, Shifeng Group, Dongfeng Agricultural, Iseki & Co., and TYM Tractors. Companies operating in the Asia-Pacific used tractor market are focusing on several strategic initiatives to strengthen their competitive position and expand market penetration. A key strategy includes strengthening refurbishment and reconditioning capabilities to enhance product reliability and extend equipment lifecycle. Market players are also investing in quality certification processes to build customer trust and improve resale value. Expansion of digital sales platforms is another major focus, enabling wider market access and streamlined buyer-seller interactions. Companies are also developing strong dealer and distribution networks to improve regional availability and after-sales support. In addition, financing solutions and flexible payment options are being introduced to make used tractors more affordable for farmers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Horsepower

- 2.2.3 Fuel

- 2.2.4 End User

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Drivers

- 3.2.1.1 Growing agricultural mechanization and farm productivity needs

- 3.2.1.2 Rising demand for cost-effective and reliable farm machinery

- 3.2.1.3 Innovation in refurbishment standards and equipment certification

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Competition from low-quality and unverified used equipment

- 3.2.2.2 Limited financing options for used agricultural equipment

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of online marketplaces and equipment listing platforms

- 3.2.3.2 Integration of equipment tracking and condition monitoring

- 3.2.1 Drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (2020-2024) (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium/Mid-Range/Value) (Driven by Primary Research)

- 3.6.3 Price Comparison: Proprietary Brands vs. Partnership Brands vs. Generic

- 3.6.4 Retailer Margin Structures & Wholesale Pricing Dynamics

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Primary Research)

- 3.10.1 Import/Export Volume & Value Trends (2020-2024) (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Origin Countries (China, Vietnam, South Korea) (Driven by Primary Research)

- 3.10.3 Tariff Impact & Trade Agreement Implications

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap (Smart Assistants in Audio Accessories, Personalized Recommendations)

- 3.11.3 AI-Enabled Features in Next-Gen Accessories (Adaptive Noise Cancellation, Health Monitoring)

- 3.11.4 Risks, Limitations & Regulatory Considerations

- 3.12 Refurbishment Capacity & Dealer Infrastructure Landscape (Driven by Primary Research)

- 3.12.1 Refurbishment Facility Capacity by Region & Key Player (Driven by Primary Research)

- 3.12.2 Dealer Network Density & Auction Throughput Analysis (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Farm tractor

- 5.2.1 Sub-compact utility tractor

- 5.2.2 Compact utility tractor

- 5.2.3 Specialty tractor

- 5.3 Construction tractor

- 5.4 Garden tractor

Chapter 6 Market Estimates & Forecast, By Horsepower, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Below 30 HP

- 6.3 31-100 HP

- 6.4 101-200 HP

- 6.5 Above 200 HP

Chapter 7 Market Estimates & Forecast, By Fuel, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Diesel

- 7.3 Petrol

- 7.4 Others (e.g., CNG, LPG)

Chapter 8 Market Estimates & Forecast, By End Users, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Individual Owners

- 8.3 Commercial

- 8.4 Residential

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Dealerships

- 9.3 Auctions

- 9.4 Private sales

- 9.5 Online platforms

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 China

- 10.3 India

- 10.4 Japan

- 10.5 South Korea

- 10.6 Indonesia

- 10.7 Thailand

- 10.8 Singapore

- 10.9 Australia

Chapter 11 Company Profiles

- 11.1 Top Global Player

- 11.1.1 Mahindra & Mahindra

- 11.1.2 Kubota Corporation

- 11.1.3 Sonalika

- 11.1.4 John Deere

- 11.1.5 Escorts Kubota

- 11.1.6 Yanmar

- 11.1.7 Lovol

- 11.1.8 TAFE

- 11.1.9 YTO Group

- 11.2 Regional Player

- 11.2.1 LS Mtron

- 11.2.2 Kioti

- 11.2.3 Foton Agricultural

- 11.2.4 Iseki & Co.

- 11.2.5 VST Tillers Tractors

- 11.2.6 Swaraj

- 11.2.7 CNH Industrial

- 11.3 Emerging Players

- 11.3.1 TYM Tractors

- 11.3.2 Dongfeng Agricultural

- 11.3.3 Shifeng Group

- 11.3.4 Kukje Machinery

- 11.3.5 Indo Farm Equipment