PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071333

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071333

All-wheel Drive Tractors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

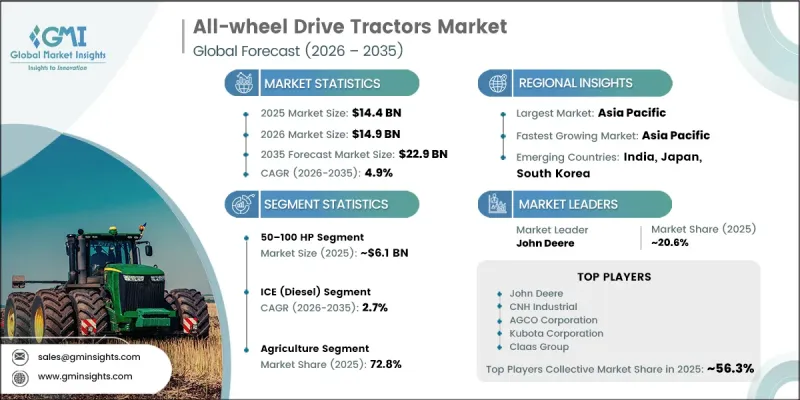

The Global All-Wheel Drive Tractors Market was valued at USD 14.4 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 22.9 billion in 2035.

The market growth is driven by the steady expansion of agricultural mechanization across both developed and developing economies, as farmers increasingly shift toward advanced machinery to improve productivity and reduce dependence on manual labor. All-wheel drive tractors are gaining strong traction due to their superior stability, enhanced traction, and improved performance on uneven and challenging terrains, making them highly suitable for diverse farming conditions. The rise of large-scale commercial agriculture and precision farming practices is further strengthening demand for high-performance agricultural equipment. Government-backed subsidies and rural development programs are also encouraging farmers to adopt mechanized solutions. In addition, the growing need for heavy-duty farming equipment capable of handling intensive operations such as plowing, hauling, seeding, and tilling is supporting sustained market expansion globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.4 Billion |

| Forecast Value | $22.9 Billion |

| CAGR | 4.9% |

The 50-100 HP segment generated USD 6.1 billion in 2025 and is expected to grow at a CAGR of 4.6% from 2026 to 2035. This segment leads the market due to its optimal balance of power output, operational efficiency, and cost-effectiveness across a broad range of agricultural tasks. Tractors in this category are widely used in medium-scale farming operations where activities such as cultivation, spraying, seeding, hauling, and plowing require reliable multi-implement support. Their relatively lower fuel consumption compared to higher horsepower models also enhances their appeal among cost-conscious farmers.

The ICE (diesel) segment accounted for 88.7% share in 2025 and is projected to grow at a CAGR of 2.7% through 2035. Diesel-powered tractors dominate the industry due to their high torque output, long operational life, and strong capability to handle demanding agricultural workloads. These tractors are extensively used in large-scale farming operations for tasks such as tilling, harvesting, plowing, and transportation across extensive farmlands. Their durability and ability to sustain long working hours make them a preferred choice in commercial agriculture.

China All-Wheel Drive Tractors Market captured USD 2.2 billion in 2025 and is expected to grow at a CAGR of 7.3% from 2026 to 2035. The country's strong performance is supported by rapid agricultural modernization, expanding farm consolidation, and government initiatives promoting mechanized farming practices. Increasing demand for high-capacity tractors is driven by large-scale cultivation and the need for efficient operations across varied terrain conditions.

Major players operating in the global all-wheel drive tractors industry include John Deere, CNH Industrial, AGCO Corporation, Kubota Corporation, Mahindra & Mahindra, Claas, Yanmar Corporation, Escorts Kubota Limited, TAFE, SDF Group, Argo Tractors, JCB, YTO Group, Lovol Intelligent Agriculture, Kioti Tractor (Daedong), LS Tractor (LS Mtron), Solis Tractors (International Tractors Limited), TYM Tractors, Zetor Tractors, Antonio Carraro, and Iseki & Co., Ltd. Companies in the all-wheel drive tractors market are focusing on expanding their product portfolios with advanced horsepower ranges and improved fuel-efficient technologies to meet diverse farming needs. Manufacturers are investing in smart farming integration, including precision agriculture systems and telematics-based monitoring solutions to enhance operational efficiency. Strategic partnerships with agricultural cooperatives and distributors are strengthening rural market penetration. Firms are also prioritizing localized manufacturing to reduce costs and improve supply chain efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Horsepower

- 2.2.3 Propulsion

- 2.2.4 Application

- 2.2.5 Mode of Operation

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing mechanization of agriculture across developed and emerging economies

- 3.2.1.2 Rising demand for high-performance tractors for heavy-duty farming applications

- 3.2.1.3 Growth of large-scale commercial farming and precision agriculture practices

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High acquisition and maintenance costs of AWD tractors

- 3.2.2.2 Fluctuations in fuel prices and operational expenses

- 3.2.3 Opportunities

- 3.2.3.1 Growing adoption of autonomous and smart farming technologies

- 3.2.3.2 Rising demand for electric and hybrid agricultural machinery

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.9.3 Regional price variation analysis

- 3.10 Trade data analysis (global HS code- 870190) (driven by paid database)

- 3.10.1 Import/export volume and value trends (driven by paid database)

- 3.10.2 Key trade corridors and tariff impact (driven by paid database)

- 3.10.3 Country-level trade patterns

- 3.11 Impact of AI and generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases and adoption roadmap by segment

- 3.11.3 Risks, limitations and regulatory considerations

- 3.12 Capacity and production landscape (driven by primary research)

- 3.12.1 Installed capacity by region and key producer (driven by primary research)

- 3.12.2 Capacity utilization rates and expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Below 50 HP

- 5.3 50-100 HP

- 5.4 Above 100 HP

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 ICE (Diesel)

- 6.3 Hybrid

- 6.4 Electric (BEV)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Agriculture

- 7.3 Construction

- 7.4 Forestry

- 7.5 Mining

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Operation Mode, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Manual

- 8.3 Autonomous

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Top Global Players

- 11.1.1 John Deere

- 11.1.2 CNH Industrial

- 11.1.3 AGCO Corporation

- 11.1.4 Kubota Corporation

- 11.1.5 Mahindra & Mahindra

- 11.1.6 Claas

- 11.1.7 Yanmar Corporation

- 11.2 Regional Champions

- 11.2.1 Escorts Kubota Limited

- 11.2.2 TAFE

- 11.2.3 SDF Group

- 11.2.4 Argo Tractors

- 11.2.5 JCB

- 11.2.6 YTO Group

- 11.2.7 Lovol Intelligent Agriculture

- 11.3 Emerging & Specialized Players

- 11.3.1 Kioti Tractor (Daedong)

- 11.3.2 LS Tractor (LS Mtron)

- 11.3.3 Solis Tractors (International Tractors Limited)

- 11.3.4 TYM Tractors

- 11.3.5 Zetor Tractors

- 11.3.6 Antonio Carraro

- 11.3.7 Iseki & Co., Ltd.