PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061352

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061352

Gas Generator Sets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

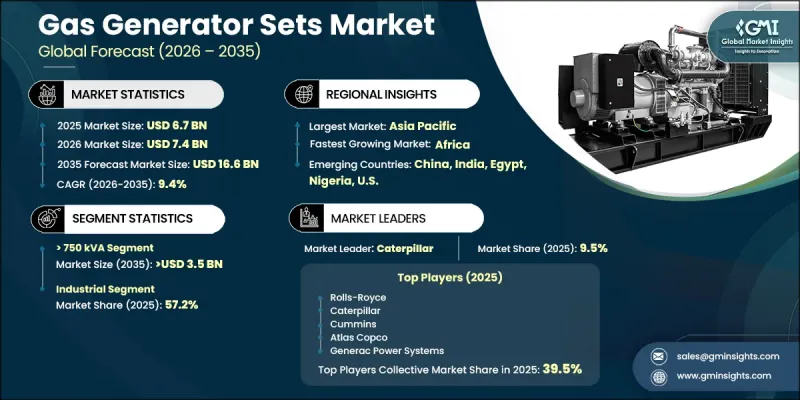

The Global Gas Generator Sets Market was valued at USD 6.7 billion in 2025 and is estimated to grow at a CAGR of 9.4% to reach USD 16.6 billion by 2035.

The industry is undergoing a notable transformation as demand shifts toward cleaner fuel-compatible power systems with lower emissions, supported by stricter environmental regulations and rising sustainability awareness across multiple regions. Increasing integration of intelligent monitoring solutions and predictive maintenance technologies is reshaping operational efficiency within gas generator systems. At the same time, growing concerns over energy security, combined with rising demand from expanding commercial infrastructure, are further accelerating market expansion. Gas generator sets operate using gaseous fuels such as natural gas and biogas to generate electricity through engine-driven systems. These units are widely deployed for standby, backup, and continuous power applications across residential, commercial, and industrial sectors. Their advantages include lower emissions, improved fuel efficiency, reduced noise levels, and higher operational reliability. Increasing urbanization and infrastructure development are boosting demand for compact and efficient power systems, particularly in densely populated areas. Additionally, rising power shortages in developing economies, expansion of remote project sites, and supportive government incentives for clean energy adoption are further strengthening industry growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.7 Billion |

| Forecast Value | $16.6 Billion |

| CAGR | 9.4% |

The high-capacity segment rated above 750 kVA is expected to reach USD 3.5 billion by 2035. These generator sets are widely deployed in large-scale industrial and commercial environments where an uninterrupted, high-load power supply is essential. They are commonly used in sectors such as manufacturing, petrochemicals, mining, and heavy engineering operations. Their ability to deliver stable performance under continuous high-demand conditions makes them critical for maintaining uninterrupted industrial processes.

The industrial gas generator sets segment accounted for 57.2% share in 2025. This dominance is attributed to increasing adoption across industrial operations as energy consumption patterns evolve and production requirements become more complex. These systems offer cost advantages due to stable fuel pricing and efficient combustion performance, making them suitable for industries facing cost optimization pressures. Continued industrial expansion and large-scale infrastructure development are further supporting segment growth.

U.S. Gas Generator Sets Market was valued at USD 853.8 million in 2025. Growth in the country is being supported by the rapid expansion of data center infrastructure and rising investments in construction activities. A growing preference for cleaner and more efficient energy solutions is encouraging the adoption of gas and dual-fuel generator systems. In addition, ongoing real estate development aligned with environmental compliance standards is further driving demand for advanced gas-based power generation solutions.

Major companies operating in the Global Gas Generator Sets Industry include Aggreko, Atlas Copco, Briggs & Stratton, Brilltech, Caterpillar, Champion Power Equipment, Cummins, DuroMax Power Equipment, Firman Power Equipment, Generac Power Systems, Genesal Energy, HIMOINSA, Mahindra Powerol, Mitsubishi Heavy Industries, Rehlko, Rolls-Royce, Wartsila, WEN Products, Westinghouse Outdoor Power Equipment, and Yanmar Holdings Co. Companies operating in the gas generator sets market are focusing on multiple strategic initiatives to strengthen their market position and enhance competitiveness. Industry players are increasingly investing in cleaner and more fuel-efficient generator technologies that align with evolving environmental regulations. Many manufacturers are integrating advanced digital monitoring, automation, and predictive maintenance capabilities to improve performance reliability and reduce downtime. Expansion of product portfolios across different power ratings is helping companies address diverse end-user requirements. Strategic partnerships with infrastructure developers and energy service providers are supporting wider market penetration. In addition, companies are investing in R&D to improve engine efficiency, reduce emissions, and enhance fuel flexibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Power rating trends

- 2.1.3 End use trends

- 2.1.4 Application trends

- 2.1.5 Sales channel trends

- 2.1.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of gas generator sets

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization & IoT integration

- 3.9.1 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

- 3.11 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.11.1 By region (Driven by Primary Research)

- 3.11.2 By power rating (Driven by Primary Research)

- 3.12 Trade data analysis (Driven by Primary Research)

- 3.12.1 Import/export value trends (Driven by Primary Research)

- 3.12.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Capacity by region & key producer (Driven by Primary Research)

- 3.13.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

- 3.14 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.14.1 AI-Driven production optimization (Driven by Primary Research)

- 3.14.2 Predictive maintenance & fault detection (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East

- 4.2.5 Africa

- 4.2.6 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Power Rating, 2022 - 2035 (USD Million & ‘000 Units)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 330 kVA

- 5.6 > 330 kVA - 750 kVA

- 5.7 > 750 kVA

Chapter 6 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & ‘000 Units)

- 6.1 Key trends

- 6.2 Residential

- 6.2.1 Single family

- 6.2.2 Multi family

- 6.3 Commercial

- 6.3.1 Telecom

- 6.3.2 Healthcare

- 6.3.3 Data centers

- 6.3.4 Educational institutions

- 6.3.5 Government centers

- 6.3.6 Hospitality

- 6.3.7 Retail sales

- 6.3.8 Real estate

- 6.3.9 Commercial complex

- 6.3.10 Infrastructure

- 6.3.11 Others

- 6.4 Industrial

- 6.4.1 Oil & gas

- 6.4.2 Manufacturing

- 6.4.3 Construction

- 6.4.4 Electric utilities

- 6.4.5 Mining

- 6.4.6 Transportation & logistics

- 6.4.7 Others

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & ‘000 Units)

- 7.1 Key trends

- 7.2 Standby

- 7.3 Peak shaving

- 7.4 Prime/continuous

Chapter 8 Market Size and Forecast, By Sales Channel, 2022 - 2035 (USD Million & ‘000 Units)

- 8.1 Key trends

- 8.2 Online

- 8.3 Dealer

- 8.4 Retail

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Russia

- 9.3.2 UK

- 9.3.3 Germany

- 9.3.4 France

- 9.3.5 Spain

- 9.3.6 Austria

- 9.3.7 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Australia

- 9.4.3 India

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.4.6 Indonesia

- 9.4.7 Malaysia

- 9.4.8 Thailand

- 9.4.9 Vietnam

- 9.4.10 Philippines

- 9.4.11 Myanmar

- 9.4.12 Bangladesh

- 9.5 Middle East

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Qatar

- 9.5.4 Turkey

- 9.5.5 Iran

- 9.5.6 Oman

- 9.6 Africa

- 9.6.1 Egypt

- 9.6.2 Nigeria

- 9.6.3 Algeria

- 9.6.4 South Africa

- 9.6.5 Angola

- 9.6.6 Kenya

- 9.6.7 Mozambique

- 9.7 Latin America

- 9.7.1 Brazil

- 9.7.2 Mexico

- 9.7.3 Argentina

- 9.7.4 Chile

Chapter 10 Company Profiles

- 10.1 Aggreko

- 10.2 Atlas Copco

- 10.3 Briggs & Stratton

- 10.4 Brilltech

- 10.5 Caterpillar

- 10.6 Champion Power Equipment

- 10.7 Cummins

- 10.8 DuroMax Power Equipment

- 10.9 Firman Power Equipment

- 10.10 Generac Power Systems

- 10.11 Genesal Energy

- 10.12 HIMOINSA

- 10.13 MAHINDRA POWEROL

- 10.14 Mitsubishi Heavy Industries

- 10.15 Rehlko

- 10.16 Rolls-Royce

- 10.17 Wartsila

- 10.18 WEN Products

- 10.19 Westinghouse Outdoor Power Equipment

- 10.20 YANMAR HOLDINGS CO.