PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061430

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061430

Liquefied Petroleum Gas Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

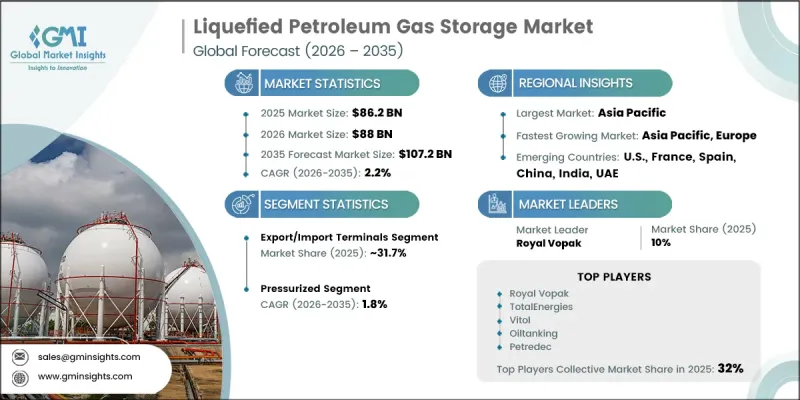

The Global Liquefied Petroleum Gas Storage Market was valued at USD 86.2 billion in 2025 and is estimated to grow at a CAGR of 2.2% to reach USD 107.2 billion by 2035.

Rising urbanization levels and increasing preference for cleaner fuel alternatives are positively influencing the growth of the liquefied petroleum gas storage industry. Governments across various economies are actively promoting wider LPG accessibility through supportive programs and initiatives, which is contributing significantly to market expansion. Growing emphasis on reducing environmental pollution and improving energy efficiency is further encouraging LPG adoption across residential, commercial, and industrial sectors. In addition, strict safety regulations and rising investments by public and private organizations in advanced storage technologies are supporting industry development. Increasing global energy demand, driven by population growth and expanding urban infrastructure, is also accelerating the need for efficient fuel storage solutions. Advancements in LPG storage systems, including enhanced storage capacity, improved materials, and digital monitoring technologies, are strengthening operational efficiency and safety standards across the industry. Moreover, the growing utilization of LPG in manufacturing, refining, petrochemical operations, and multiple industrial processes is creating favorable business opportunities for the global liquefied petroleum gas storage market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $86.2 Billion |

| Forecast Value | $107.2 Billion |

| CAGR | 2.2% |

The industrial use segment is expected to reach USD 19.1 billion by 2035 due to the increasing adoption of LPG as a cleaner and more energy-efficient industrial fuel alternative. Industries are steadily shifting toward LPG to improve operational efficiency while reducing environmental impact compared to conventional fuel sources. Growing demand for reliable bulk storage infrastructure, including large-scale tanks and industrial storage facilities, is supporting segment growth. Rising industrial fuel consumption and the increasing focus on sustainable industrial operations are also contributing to the expansion of the industrial use segment within the liquefied petroleum gas storage market.

The pressurized segment was valued at USD 37 billion in 2025 and is anticipated to grow at a CAGR of 1.8% from 2026 to 2035. Pressurized LPG tanks continue to play a critical role in the safe storage and transportation of liquefied petroleum gas by maintaining the fuel in liquid form under controlled pressure conditions. These storage systems provide high energy density and enable efficient storage of substantial LPG volumes within compact spaces, making them suitable for a wide range of residential and industrial applications. Technological advancements and the incorporation of enhanced safety and monitoring features are further supporting the adoption of pressurized LPG storage systems across multiple sectors.

North America Liquefied Petroleum Gas Storage Market reached USD 21.7 billion in 2025 and is projected to grow at a CAGR of 1.4% through 2035. Strong availability of shale gas resources and increasing focus on expanding LPG production capacities are contributing to industry growth across the country. Rising energy demand driven by population growth and evolving energy consumption patterns is also supporting market expansion. The ongoing transition toward cleaner energy solutions has increased LPG adoption across residential, commercial, and industrial applications. In addition, the integration of automation technologies and smart monitoring systems within storage and distribution infrastructure is improving operational efficiency and strengthening the overall business landscape for the U.S. liquefied petroleum gas storage market.

Major companies operating in the Global Liquefied Petroleum Gas Storage Industry include Arslan Enginery, CB&I, Chemet Group, China Petroleum, CIMC ENRIC, CLW Group, Emirates Gas, Flogas, ISISAN, Karbonsan, LAPESA GRUPO EMPRESARIAL, Modern Welding, Oiltanking, Omera, Pertamina, Petredec, Roben Manufacturing, Royal Vopak, TotalEnergies, TransTech Energy, and Vitol. Companies operating in the liquefied petroleum gas storage market are focusing on multiple strategic initiatives to strengthen their competitive position and expand their global presence. Industry participants are investing heavily in advanced storage technologies, automation systems, and digital monitoring solutions to improve operational safety, storage efficiency, and supply chain management. Many companies are also expanding storage capacities and upgrading infrastructure to meet rising LPG demand across industrial, commercial, and residential sectors. Strategic collaborations, long-term supply agreements, and partnerships with energy distributors are helping businesses enhance market penetration and customer reach. In addition, manufacturers are emphasizing the development of environmentally sustainable and regulation-compliant storage solutions to align with evolving industry standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Storage type trends

- 2.4 Ownership model trends

- 2.5 Application trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of liquefied petroleum gas storage terminal (Solution Core)

- 3.8 Price trend analysis, 2022-2035 (USD/Barrel) (Driven by Primary Research)

- 3.8.1 By storage type (Driven by Primary Research)

- 3.8.2 By region (Driven by Primary Research)

- 3.9 Emerging opportunities & trends

- 3.9.1 Digital transformation with IoT technologies

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis & future outlook

- 3.11 Impact of AI & Generative AI on the market (Solution Core)

- 3.11.1 AI-Driven production optimization (Solution Core)

- 3.11.2 Predictive maintenance & fault detection (Solution Core)

- 3.12 Trade data analysis (Driven by Primary Research)

- 3.12.1 Import/export volume & value trends (Driven by Primary Research)

- 3.12.2 Key trade corridors & tariff impact (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Storage Type, 2022 - 2035 (USD Million, Million Barrels)

- 5.1 Key trends

- 5.2 Pressurized

- 5.3 Refrigerated

- 5.4 Mounded

- 5.5 Underground

Chapter 6 Market Size and Forecast, By Ownership Model, 2022 - 2035 (USD Million, Million Barrels)

- 6.1 Key trends

- 6.2 Captive

- 6.3 Third-Party Commercial

- 6.4 PPP

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million, Million Barrels)

- 7.1 Key trends

- 7.2 Residential/Commercial

- 7.3 Industrial

- 7.4 Petrochemical Feedstock

- 7.5 Autogas

- 7.6 Export/Import Terminals

- 7.7 Strategic Reserves

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million, '000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Spain

- 8.3.2 Russia

- 8.3.3 UK

- 8.3.4 Italy

- 8.3.5 France

- 8.3.6 Germany

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Turkey

- 8.5.4 South Africa

- 8.5.5 Morocco

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Mexico

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 Arslan Enginery

- 9.2 CB&I

- 9.3 Chemet Group

- 9.4 China Petroleum

- 9.5 CIMC ENRIC

- 9.6 CLW Group

- 9.7 Emirates Gas

- 9.8 Flogas

- 9.9 ISISAN

- 9.10 Karbonsan

- 9.11 LAPESA GRUPO EMPRESARIAL

- 9.12 Modern Welding

- 9.13 Oiltanking

- 9.14 Omera

- 9.15 Pertamina

- 9.16 Petredec

- 9.17 Roben Manufacturing

- 9.18 Royal Vopak

- 9.19 TotalEnergies

- 9.20 TransTech Energy

- 9.21 Vitol