PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071193

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071193

Asia Pacific Cold Chain Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

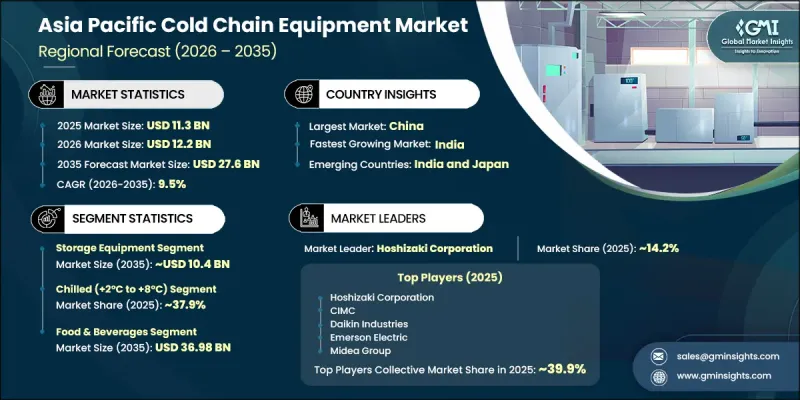

Asia Pacific Cold Chain Equipment Market was valued at USD 11.3 billion in 2025 and is estimated to grow at a CAGR of 9.5% to reach USD 27.6 billion by 2035.

Market growth is driven by increasing investments in temperature-controlled infrastructure across food preservation systems, pharmaceutical logistics networks, and healthcare supply chains handling temperature-sensitive products. A key structural driver is the rapid expansion of pharmaceutical manufacturing activity across major regional economies, supported by rising production of advanced therapies and biologics. At the same time, accelerating urbanization and the formalization of food distribution systems are increasing demand for modern cold storage and refrigerated transport solutions. The ongoing shift from fragmented storage facilities toward fully integrated, digitally enabled cold chain ecosystems is reshaping equipment requirements across the region. The adoption of IoT-enabled monitoring systems and automated temperature control technologies is further improving operational efficiency and compliance standards. Regulatory frameworks are also becoming more stringent, with stronger alignment toward international cold chain quality and safety guidelines, which is encouraging upgrades in storage and transportation infrastructure. As a result, cold chain equipment is evolving from basic refrigeration systems into highly controlled, data-driven logistics infrastructure supporting both food and pharmaceutical industries across Asia Pacific.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.3 Billion |

| Forecast Value | $27.6 Billion |

| CAGR | 9.5% |

The storage equipment segment held a 46% share, reaching USD 5.2 billion in 2025. It is projected to rise to approximately USD 10.4 billion by 2035, expanding at a CAGR of 7.3% during the forecast period. This segment includes a wide range of infrastructure such as refrigerated storage facilities, temperature-controlled chambers, freezing systems, and advanced preservation units used across multiple industries. Demand remains strong due to increasing reliance on large-scale storage infrastructure for perishable goods and temperature-sensitive pharmaceutical products. Continued investment in cold storage expansion and modernization is reinforcing the segment's leadership position in the overall market structure.

The chilled temperature segment accounted for approximately 37.9% of total Asia Pacific cold chain equipment revenue in 2025, making it the leading temperature category within the market. This segment supports a broad spectrum of applications that require controlled cooling conditions for maintaining product quality and safety. It plays a central role in the storage and transportation of perishable food products as well as sensitive medical and biological materials. Growing emphasis on maintaining strict temperature consistency throughout the supply chain is driving continued reliance on chilled storage and transport solutions across industries.

China Cold Chain Equipment Industry held 43% share in 2025. The country's leadership position is supported by its strong pharmaceutical manufacturing base and extensive logistics infrastructure supporting temperature-controlled distribution. Continued investment in modern cold chain facilities and the expansion of regulated distribution networks are further strengthening market growth. Rising demand for advanced refrigeration and monitoring systems is also contributing to infrastructure upgrades across the national cold chain ecosystem.

Key companies operating in the Asia Pacific cold chain equipment market include Danfoss A/S, Carrier Global Corporation, Daikin Industries Ltd., Johnson Controls International, Trane Technologies (Thermo King), Emerson Electric/Copeland, Mitsubishi Electric Corporation, CIMC (China International Marine Containers), Midea Group, Blue Star Limited, Hoshizaki Corporation, Haier Biomedical, Liebherr Group, Fujitsu General, Voltas Limited, Panasonic Corporation (HVAC & Cold Chain), Gree Electric Appliances, Zhongke Meiling (Meling Biomedical), Bingshan Group (Dalian Bingshan), Peli BioThermal, and va-Q-tec. Companies operating in the Asia Pacific cold chain equipment market are focusing on technology integration, infrastructure expansion, and service enhancement to strengthen their competitive position. Major players are increasingly investing in IoT-enabled refrigeration systems, real-time temperature monitoring solutions, and automated control technologies to improve operational reliability and compliance. Strategic collaborations with logistics providers, pharmaceutical manufacturers, and food supply chain operators are enabling broader market penetration. Firms are also expanding production capacities and regional manufacturing footprints to meet rising demand more efficiently. In addition, companies are prioritizing energy-efficient and environmentally sustainable refrigeration technologies to align with tightening regulatory standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Equipment type

- 2.2.3 Temperature range

- 2.2.4 Application

- 2.2.5 Mode of operation

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for temperature-sensitive transportation and storage solutions

- 3.2.1.2 Expansion of biologics, vaccines, and temperature-sensitive pharmaceutical products

- 3.2.1.3 Growing investment in organized cold storage infrastructure and food logistics

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High installation and operational costs associated with advanced refrigeration systems

- 3.2.2.2 Energy consumption and maintenance complexity of cold chain infrastructure

- 3.2.3 Opportunities

- 3.2.3.1 Increasing adoption of IoT-enabled monitoring and automation technologies

- 3.2.3.2 Expansion of pharmaceutical cold chain infrastructure across emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.10 Trade data analysis (HS Code 8418 for active refrigerating/freezing machinery and HS Code 9406 for insulated cold room structures) (driven by paid database)

- 3.10.1 Import/export volume and value trends (driven by paid database)

- 3.10.2 Key trade corridors and tariff impact (driven by paid database)

- 3.11 Impact of AI and generative AI on the market

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases and adoption roadmap by segment

- 3.11.3 Risks, limitations and regulatory considerations

- 3.12 Capacity and production landscape (driven by primary research)

- 3.12.1 Installed capacity by region and key producer (driven by primary research)

- 3.12.2 Capacity utilization rates and expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Storage equipment

- 5.3 Transportation equipment

- 5.4 Monitoring & control systems

- 5.5 Temperature-controlled packaging

Chapter 6 Market Estimates & Forecast, By Temperature Range, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Controlled ambient (+15°C to +25°C)

- 6.3 Chilled (+2°C to +8°C)

- 6.4 Frozen (-18°C to -25°C)

- 6.5 Cryogenic (Below -80°C)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.2.1 Fruits & vegetables

- 7.2.2 Dairy products

- 7.2.3 Meat, fish & seafood

- 7.2.4 Processed food & ready-to-eat meals

- 7.2.5 Bakery & confectioneries

- 7.2.6 Others

- 7.3 Pharmaceuticals

- 7.3.1 Vaccines

- 7.3.2 Biologics & biosimilars

- 7.3.3 Temperature-sensitive APIs

- 7.3.4 Clinical trial materials

- 7.4 Healthcare

- 7.4.1 Blood products & plasma

- 7.4.2 Organs & tissue for transplantation

- 7.4.3 Medical supplies & reagents

- 7.5 Chemicals

- 7.5.1 Specialty chemicals

- 7.5.2 Volatile compounds

- 7.6 Biotechnology

- 7.6.1 Cell & gene therapies

- 7.6.2 Research samples & biobanking

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Mode of Operation, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Active systems

- 8.3 Passive systems

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Country, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.1.1 China

- 10.1.2 India

- 10.1.3 Japan

- 10.1.4 South Korea

- 10.1.5 Australia

- 10.1.6 Philippines

- 10.1.7 Thailand

- 10.1.8 Vietnam

Chapter 11 Company Profiles

- 11.1 Top Global Players

- 11.1.1 Daikin Industries Ltd.

- 11.1.2 Carrier Global Corporation

- 11.1.3 Trane Technologies (Thermo King)

- 11.1.4 Emerson Electric

- 11.1.5 Johnson Controls International

- 11.1.6 Danfoss A/S

- 11.1.7 Mitsubishi Electric Corporation

- 11.2 Regional Champions

- 11.2.1 Hoshizaki Corporation

- 11.2.2 CIMC (China International Marine Containers)

- 11.2.3 Midea Group

- 11.2.4 Bingshan Group (Dalian Bingshan)

- 11.2.5 Haier Biomedical

- 11.2.6 Blue Star Limited

- 11.2.7 Voltas Limited

- 11.3 Emerging & Specialized Players

- 11.3.1 Panasonic Corporation (HVAC & Cold Chain)

- 11.3.2 Gree Electric Appliances

- 11.3.3 Zhongke Meiling (Meling Biomedical)

- 11.3.4 Liebherr Group

- 11.3.5 Fujitsu General

- 11.3.6 Peli BioThermal

- 11.3.7 va-Q-tec