PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071202

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071202

Graphics Card Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

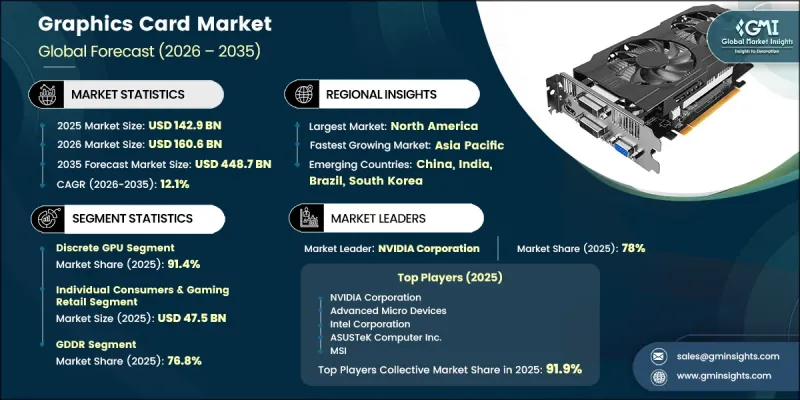

The Global Graphics Card Market was valued at USD 142.9 billion in 2025 and is estimated to grow at a CAGR of 12.1% to reach USD 448.7 billion by 2035.

Market growth is fueled by the increasing integration of artificial intelligence and machine learning technologies, rising demand for high-performance computing capabilities, and the growing need for advanced graphical processing across multiple industries. The expansion of large-scale cloud computing environments and GPU-powered data center infrastructure is creating substantial opportunities for market participants. In addition, increasing demand for graphics-intensive applications, digital content production, and advanced visualization technologies continues to support industry expansion. The market is also benefiting from the wider adoption of GPU computing for blockchain-related operations and other parallel processing tasks that require significant computational efficiency. As organizations continue to invest in accelerated computing solutions and consumers seek enhanced graphical experiences, graphics cards are becoming increasingly essential across enterprise, commercial, and personal computing environments. This combination of technological innovation, infrastructure development, and evolving performance requirements is expected to sustain long-term growth across the global graphics card industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $142.9 Billion |

| Forecast Value | $448.7 Billion |

| CAGR | 12.1% |

The graphics card market continues to gain momentum as organizations increasingly rely on advanced computing systems to handle highly complex workloads. The growing deployment of artificial intelligence and machine learning models has intensified demand for processors designed to efficiently manage large-scale parallel computing operations. Graphics processing units have emerged as critical components for accelerating computational tasks across training and inference environments, making them indispensable in modern computing ecosystems. Increased investment from both public and private sectors in next-generation computing infrastructure is further strengthening market demand. At the same time, rising interest in immersive digital experiences is encouraging the adoption of powerful graphics hardware capable of delivering enhanced visual performance. The continued evolution of computing requirements across commercial, industrial, and institutional sectors is creating a strong foundation for sustained market expansion.

The discrete GPU segment accounted for 91.4% share in 2025. Its dominant position is primarily attributed to superior processing capabilities, extensive memory resources, and dedicated architectures designed for demanding graphical and computational workloads. Unlike integrated solutions, discrete GPUs provide greater performance efficiency for advanced rendering tasks, accelerated computing operations, and data-intensive applications. Their ability to support high memory bandwidth and specialized processing functions makes them the preferred choice across numerous performance-driven computing environments. As demand for increasingly powerful computing platforms continues to rise, discrete graphics cards are expected to maintain their leadership position within the market.

The individual consumers and gaming retail segment generated USD 47.5 billion in 2025. Strong consumer demand for advanced graphics hardware continues to drive revenue growth within this segment. The market benefits from a consistent replacement cycle, as users regularly upgrade graphics cards to support evolving software requirements, improved visual performance standards, and next-generation computing experiences. This ongoing demand pattern contributes to the segment's stability and reinforces its position as a major source of revenue for graphics card manufacturers.

North America Graphics Card Market captured 38.1% share in 2025. The region's leadership is supported by a robust semiconductor industry, substantial investment in advanced computing infrastructure, and a favorable environment for technological innovation. Growing expenditures focused on artificial intelligence development and high-performance computing capabilities have strengthened regional demand for advanced graphics processors. Furthermore, initiatives designed to enhance domestic semiconductor production capacity have encouraged additional investment in computing infrastructure, supporting broader adoption of GPU-based technologies.

Key companies operating in the Global Graphics Card Market include NVIDIA Corporation, Intel Corporation, Advanced Micro Devices, MSI, ASUSTeK Computer Inc., Gigabyte Technology, Sapphire Technology, Zotac, Palit Microsystems, Colorful Technology, PowerColor, XFX, PNY Technologies, ASRock, Leadtek Research, Sparkle, Matrox Graphics, Advantech Co., Ltd., and Kontron AG. Companies operating in the graphics card market are focusing on a combination of innovation, strategic partnerships, and product portfolio expansion to strengthen their competitive positions. Leading manufacturers continue to invest heavily in research and development to improve processing performance, energy efficiency, and advanced computing capabilities. Businesses are also introducing next-generation graphics solutions tailored for artificial intelligence, cloud computing, professional visualization, and consumer applications. Strategic collaborations with semiconductor suppliers, cloud service providers, and technology firms are helping companies expand market reach and accelerate product adoption. In addition, firms are increasing investments in manufacturing capacity and supply chain optimization to meet rising global demand. Geographic expansion, enhanced distribution networks, and customer-focused product differentiation remain important growth strategies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 GPU type trends

- 2.2.2 End-User trends

- 2.2.3 Memory type trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of AI, machine learning, and high-performance computing (HPC) workloads

- 3.2.1.2 Expansion of the global gaming industry and demand for high performance graphics rendering

- 3.2.1.3 Rapid development of hyperscale data centers and cloud-based GPU infrastructure

- 3.2.1.4 Increasing use of GPUs in professional content creation and visualization applications

- 3.2.1.5 Growing deployment of GPUs in cryptocurrency, blockchain, and parallel processing applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing and development costs of advanced GPU architectures

- 3.2.2.2 Supply chain constraints and dependence on advanced semiconductor foundries

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of edge computing and on-device AI acceleration

- 3.2.3.2 Emergence of metaverse, AR/VR, and immersive digital environments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By GPU Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Discrete Graphics Card devices

- 5.3 Discrete GPU

- 5.4 Integrated GPU

Chapter 6 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Cloud service providers (CSPs) & hyperscalers

- 6.3 Enterprise IT & private clouds

- 6.4 Individual consumers & gaming retail

- 6.5 Professional visualization enterprises

- 6.6 Government, defense & sovereign infrastructure

- 6.7 Automotive OEMs

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Memory Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 GDDR

- 7.2.1 GDDR6

- 7.2.2 GDDR6X

- 7.2.3 GDDR7

- 7.3 HBM

- 7.3.1 HBM2

- 7.3.2 HBM3

- 7.3.3 HBM3e

- 7.3.4 HBM4

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 NVIDIA Corporation

- 9.1.2 Advanced Micro Devices

- 9.1.3 Intel Corporation

- 9.1.4 ASUSTeK Computer Inc.

- 9.1.5 MSI

- 9.2 Regional key players

- 9.2.1 North America

- 9.2.1.1 PNY Technologies

- 9.2.2 Asia Pacific

- 9.2.2.1 Gigabyte Technology

- 9.2.2.2 Sapphire Technology

- 9.2.2.3 Zotac

- 9.2.2.4 Palit Microsystems

- 9.2.2.5 Colorful Technology

- 9.2.2.6 PowerColor

- 9.2.2.7 XFX

- 9.2.2.8 ASRock

- 9.2.2.9 Leadtek Research

- 9.2.2.10 Sparkle

- 9.2.2.11 Advantech Co., Ltd

- 9.2.3 Europe

- 9.2.3.1 Kontron AG

- 9.2.3.2 Matrox Graphics

- 9.2.1 North America