PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071206

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071206

North America Camera Lens Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

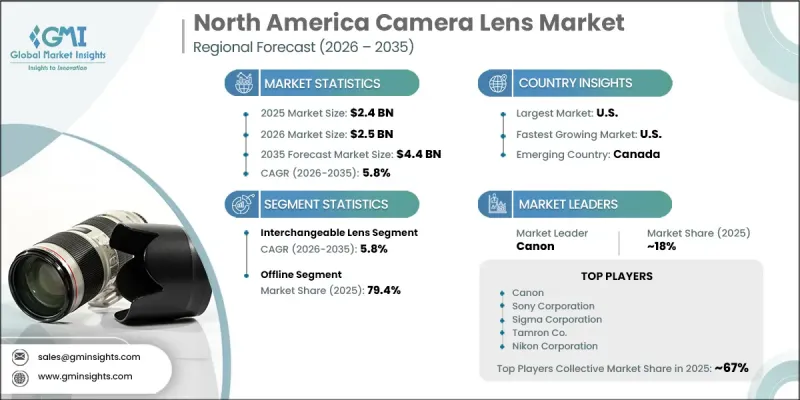

North America Camera Lens Market was valued at USD 2.4 billion in 2025 and is estimated to grow at a CAGR of 5.8% to reach USD 4.4 billion by 2035.

Growth is fueled by rapid advancements in smartphone imaging systems, where consumers are increasingly prioritizing superior photo and video quality. This shift has encouraged manufacturers to develop highly sophisticated optical solutions, including multi-lens configurations, improved zoom performance, and enhanced low-light imaging capabilities. As smartphones continue to replace traditional cameras for everyday use, demand for compact, high-precision lens modules has strengthened significantly. The integration of artificial intelligence and computational imaging technologies is further reshaping optical design requirements, pushing the need for advanced lens systems that can support enhanced digital processing. In parallel, the expansion of digital content creation, streaming platforms, and social media-driven visual communication is boosting demand for high-performance camera equipment across North America.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.4 Billion |

| Forecast Value | $4.4 Billion |

| CAGR | 5.8% |

The interchangeable lens segment generated USD 1.5 billion in 2025 and is forecast to grow at a CAGR of 5.8% through 2035. Increasing participation in professional photography, filmmaking, videography, and digital content production is driving demand for advanced camera systems and compatible lens ecosystems. The ongoing shift from DSLR to mirrorless platforms is also encouraging users to upgrade to newer lens technologies, further accelerating replacement cycles. Interchangeable lenses are widely preferred due to their flexibility, superior optical performance, and ability to deliver enhanced depth control, improved low-light results, and variable focal length options across creative and commercial applications.

The offline distribution channel accounted for 79.4% share in 2025 and is expected to grow at a CAGR of 5.7% during 2026-2035. Physical retail channels remain important for buyers who prefer hands-on evaluation of optical equipment before purchase. Customers often assess parameters such as ergonomics, build quality, autofocus performance, and image sharpness in person, particularly when investing in high-value professional-grade lenses. Specialty camera stores and electronics retailers continue to play a key role by offering expert consultation, product demonstrations, and post-purchase support services that enhance customer confidence.

United States Camera Lens Market captured USD 1.8 billion in 2025 and is projected to grow at a CAGR of 5.8% from 2026 to 2035. Strong demand is supported by a large base of professional photographers, filmmakers, broadcasters, and digital creators who require high-performance imaging equipment. The growing influence of online content creation and social media platforms is further increasing demand for advanced optical solutions. The country also continues to lead in imaging innovation, with ongoing advancements in computational photography, artificial intelligence-enabled imaging systems, and precision optical engineering contributing to frequent product upgrades and replacement cycles.

Key companies operating in the North America camera lens market include Canon Inc., Sony Corporation, Nikon Corporation, FUJIFILM Corporation, Panasonic Corporation (Lumix), Sigma Corporation, Tamron Co., Ltd., Carl Zeiss AG, Largan Precision Co., Ltd., Sunny Optical Technology Group Co., Ltd., Asia Optical Co., Inc., Tokina Co., Ltd., Kantatsu Co., Ltd., Sekonix Co., Ltd., Venus Optics (Laowa Lenses), Samyang Optics (Rokinon), Meike Global, 7Artisans Photoelectric Technology, TTArtisan (Shenzhen Mingjiang Optical), Viltrox (Shenzhen Jueying Technology), and Mitakon. Market participants are focusing on strengthening their competitive positioning through continuous innovation in optical design and manufacturing precision. Companies are investing in advanced lens technologies that support high-resolution imaging, computational photography, and AI-driven camera systems. Strategic collaborations with smartphone manufacturers and camera OEMs are helping firms integrate next-generation lenses into mainstream devices. Expansion of product portfolios across premium, mid-range, and entry-level segments is enabling broader market penetration. Firms are also emphasizing faster product upgrade cycles to align with evolving consumer expectations in digital imaging.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Type

- 2.2.3 Focal length

- 2.2.4 Mount/compatibility

- 2.2.5 Price range

- 2.2.6 Application

- 2.2.7 End Use

- 2.2.8 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for advanced smartphone cameras

- 3.2.1.2 Growth of professional content creation & social media economy

- 3.2.1.3 Expansion of media, entertainment, and OTT industry

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Intense competition from smartphone camera technology

- 3.2.2.2 High cost of advanced lens manufacturing

- 3.2.3 Opportunities

- 3.2.3.1 Innovation in smartphone camera modules

- 3.2.3.2 Industrial automation and machine vision

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Trade data analysis (HS Code 9002.11)

- 3.7.1 Import/export volume & value trends

- 3.7.2 Key trade corridors & tariff impact

- 3.8 Pricing analysis

- 3.8.1 Historical price trend analysis (driven by primary research)

- 3.8.2 Pricing strategy by player type (premium / value / mass market)

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behavior analysis

- 3.12.1 Purchasing patterns

- 3.12.2 Preference analysis

- 3.12.3 Regional variations in consumer behavior

- 3.12.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Built-in lens

- 5.3 Interchangeable lens

Chapter 6 Market Estimates & Forecast, By Focal Length, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Ultra-wide (<16mm)

- 6.3 Wide (16-35mm)

- 6.4 Standard (35-70mm)

- 6.5 Short telephoto (70-135mm)

- 6.6 Long telephoto (>135mm)

Chapter 7 Market Estimates & Forecast, By Mount/Compatibility, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Mirrorless mount

- 7.3 DSLR mount

- 7.4 C-mount

- 7.5 CS-mount

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Price Range, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Consumer electronics

- 9.3 Automotive

- 9.4 Medical

- 9.5 Industrial & machine vision

- 9.6 Other (security & surveillance, scientific research)

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Professional users

- 10.3 Individuals

- 10.4 Manufacturers

- 10.5 Consumer electronics

- 10.6 Automotive

- 10.7 Medical

- 10.8 Others

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 Online

- 11.2.1 E-commerce platforms

- 11.2.2 Company owned website

- 11.3 Offline

- 11.3.1 Camera specialty stores

- 11.3.2 Electronics retail chains

- 11.3.3 Authorized dealer network

Chapter 12 Market Estimates & Forecast, By Country, 2022 - 2035, (USD Billion) (Million Units)

- 12.1 Key trends

- 12.2 U.S.

- 12.3 Canada

Chapter 13 Company Profiles

- 13.1 Top Global Players

- 13.1.1 Canon Inc.

- 13.1.2 Sony Corporation

- 13.1.3 Nikon Corporation

- 13.1.4 Sigma Corporation

- 13.1.5 Tamron Co., Ltd.

- 13.1.6 FUJIFILM Corporation

- 13.1.7 Panasonic Corporation (Lumix)

- 13.1.8 Carl Zeiss AG

- 13.2 Regional Champions

- 13.2.1 Largan Precision Co., Ltd.

- 13.2.2 Sunny Optical Technology Group Co., Ltd.

- 13.2.3 Asia Optical Co., Inc.

- 13.2.4 Tokina Co., Ltd.

- 13.2.5 Kantatsu Co., Ltd.

- 13.2.6 Sekonix Co., Ltd.

- 13.3 Emerging Players

- 13.3.1 Venus Optics (Laowa Lenses)

- 13.3.2 Samyang Optics (Rokinon)

- 13.3.3 Meike Global

- 13.3.4 7Artisans Photoelectric Technology

- 13.3.5 TTArtisan (Shenzhen Mingjiang Optical)

- 13.3.6 Viltrox (Shenzhen Jueying Technology)

- 13.3.7 Mitakon