PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044225

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044225

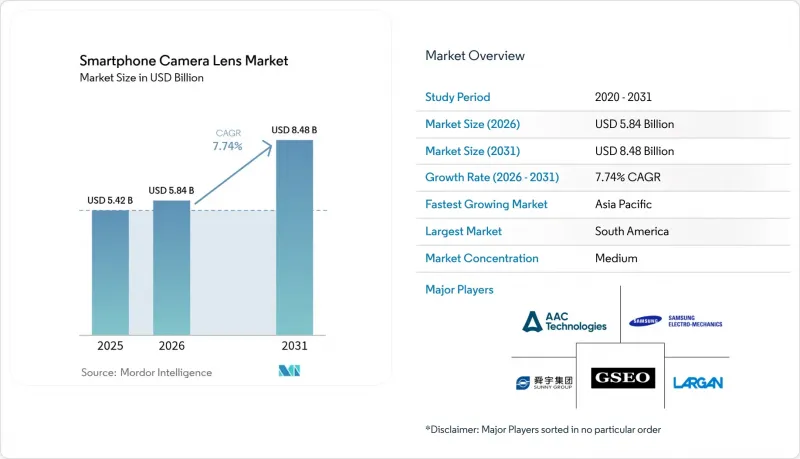

Smartphone Camera Lens - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The smartphone camera lens market size was valued at USD 5.42 billion in 2025 and estimated to grow from USD 5.84 billion in 2026 to reach USD 8.48 billion by 2031, at a CAGR of 7.74% during the forecast period (2026-2031).

Average selling prices for lens modules continue to climb as device makers replace basic plastic optics with 7- or 8-element glass-plastic hybrids, especially in periscope and variable-aperture assemblies. Telescopic zoom capability is expanding into mid-range handsets, giving suppliers a lucrative path to offset stagnant global smartphone shipments. Demand also benefits from multi-camera configurations that require ultra-wide, macro, and depth lenses to support AI-driven computational photography. Precision glass-molding capacity, already operating near full utilization, is set to tighten further as per-unit defects remain higher than conventional wide-angle modules.

Global Smartphone Camera Lens Market Trends and Insights

Rapid Adoption of Periscope and Telephoto Modules

Periscope telephoto modules moved from USD 1,000 flagships to USD 400-600 handsets in 2025, shrinking the optical-zoom gap between premium and mid-range devices. Each assembly relies on 7- or 8-element glass-plastic hybrids plus a prism, so average selling prices jump 18-22% when periscope zoom is added. Shipments rose 34% year over year at Largan Precision, yet prism alignment tolerances below 5 µm keep reject rates roughly 12-15 points higher than for wide-angle lenses. OEM marketing now highlights 5x to 10x optical zoom as a headline feature, reinforcing consumer awareness of lens quality. Capacity constraints in precision glass molding suggest that periscope penetration will continue to lift supplier margins through 2027.

Megapixel Race Above 50 MP Lifting Lens ASPs

Sony's 200 MP LYT-901 sensor sets an optical benchmark of modulation-transfer-function values above 0.6 at 100 lp/mm, forcing lens makers to use aspheric glass and advanced coatings. Samsung's ISOCELL HP5 keeps camera stacks thinner but raises module cost, pushing flagship optical subsystems toward USD 80-100 per phone. The gulf between high-end and entry optics now reaches a 3-6X price multiple, so vendors prioritize premium projects even while global handset volumes flatten. Higher pixel counts also widen image circles, which drives larger lens diameters and additional elements. These requirements explain why hybrid lenses gained nearly half the market in 2025.

Global Smartphone Unit Saturation

Worldwide shipments stalled near 1.2 billion units and India's market slid 1% in 2025, as replacement cycles stretched beyond three years. TechInsights tracked only 4% global unit growth in 1H 2025 versus 8% revenue growth for devices above USD 600, highlighting a shift to value over volume. This saturation caps lens demand growth at single-digit rates even while premium tiers thrive. Suppliers face revenue concentration risk because flagship models represent under one-quarter of units yet almost half of lens income. Any downturn in premium demand could therefore compress margins quickly.

Other drivers and restraints analyzed in the detailed report include:

- AI-Centric Computational Photography Requirements

- Proliferation of Multi-Camera Smartphones

- Aggressive Pricing Pressure in Mid- and Low-Tier Handsets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Telephoto optics posted an 8.58% CAGR to 2031, the quickest pace among all technologies, so their slice of the smartphone camera lens market size is expanding even as total handset units plateau. Shipments rose when periscope zoom modules migrated into USD 400-600 phones, allowing brands to advertise 5x to 10x optical zoom as a mainstream feature. Wide-angle lenses still held 42.36% smartphone camera lens market share in 2025, but their growth stalled because innovation dollars now chase auxiliary cameras. Ultra-wide designs gained relevance after AI rectilinear correction unlocked 120-degree fields of view, while macro sensors began to disappear as high-resolution telephotos can crop in for close-ups. Canon's 26-stop-range SPAD prototype suggests future telephotos will demand >95% light transmission, which pushes even more glass into lens stacks.

Higher element counts and prism assemblies lift telephoto module prices 40-50% above wide units, so suppliers such as Largan and Sunny Optical funnel capacity toward this richer mix. Each periscope lens requires 7-8 glass-plastic hybrid elements, raising both tooling complexity and yield risk. Prism alignment tolerances under 5 µm keep per-unit defect rates roughly 12-15 points above conventional modules, yet profit margins remain attractive because ASPs rise 18-22% whenever periscope zoom is added. Ultra-wide modules, bolstered by rectilinear algorithms, now feature free-form aspheric glass that costs 25-30% more than earlier plastic designs. Macro and depth functions consolidate into higher-resolution secondaries, trimming sensor counts while sustaining total lens revenue per phone.

Glass-plastic hybrids captured 47.89% of 2025 revenue, and their 8.39% CAGR means they will overtake all-plastic designs in smartphone camera lens market share before 2028. Hybrid stacks mix two or three glass elements with four or five plastic ones, marrying chromatic-aberration control to weight savings. All-glass lenses remain confined to foldables and ultra-premium models because a seven-element glass stack weighs 15-20% more and costs up to 40% extra to build. All-plastic optics linger in sub-USD 200 devices, but their share erodes as mid-range makers tout hybrid upgrades for camera differentiation. Sunny Optical more than doubled hybrid-lens revenue in 1H 2025 as Huawei, OPPO, and vivo launched multi-element telephotos.

Process capability is the swing factor. Precision glass molding from Largan achieves surface accuracy below 0.2 µm, impossible with plastics, which ensures MTF above 0.6 at 100 lp/mm for 200 MP sensors. New polymer formulas cut thermal expansion from 70 ppm / °C to 50 ppm / °C, narrowing the focus-shift gap with glass, yet not enough for periscope designs. Foldable phones also favor hybrids because plastic keeps hinge-side weight down, while glass stiffens the stack to withstand repeated folding. As AI imaging pushes transmission targets past 92%, hybrids become the default for mid- and high-end tiers, locking in their path to majority status in the smartphone camera lens market size.

The Smartphone Camera Lens Market Report is Segmented by Lens Technology (Telephoto, Macro/Depth, and More), Lens Material (All-Glass, All-Plastic, and More), Camera Position (Rear-Primary, Rear-Secondary, Front/Facing), Manufacturing Process (Injection Moulding, Precision Glass Moulding, and More), Smartphone Tier (Flagship, Mid-Range, Entry-Level), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 64.22% of 2025 revenue thanks to China's dominance in lens fabrication and assembly, with Guangdong and Jiangsu provinces hosting a majority of global capacity. India's Production-Linked Incentive scheme is redirecting camera module work to Tamil Nadu and Karnataka, trimming lead times for Apple and Samsung. Tata Electronics' takeover of Wistron's iPhone plant exemplifies this shift, accelerating localized sourcing of lenses and actuators. Vietnam is emerging as a secondary center as LG Innotek's V3 expansion doubles local output.

South America is the fastest-growing region at an 8.79% CAGR, propelled by 5G rollouts and a rising preference for mobile video that averages 9 GB per month. Chinese OEMs HONOR, OPPO, and vivo capture share in Brazil, Argentina, and Chile, where smartphones priced under USD 200 doubled shipments in 2024 yet a premium segment above USD 600 is also expanding. This bifurcation fuels lens demand for both cost-sensitive modules and high-margin hybrids.

North America and Europe together account for roughly one-third of global revenue but trail the worldwide growth rate at 6.5-7.0% CAGR because replacement cycles now exceed 3.5 years. Middle East and Africa collectively hold under 10% share; 5G network investments lift penetration, yet affordability keeps lens ASPs in the USD 8-12 range and supports mainly all-plastic designs. Currency volatility and tariffs in Nigeria and Egypt add further constraints.

- Largan Precision Co. Ltd.

- Sunny Optical Technology (Group) Co. Ltd.

- Samsung Electro-Mechanics Co. Ltd.

- Genius Electronic Optical Co. Ltd.

- AAC Technologies Holdings Inc.

- LG Innotek Co. Ltd.

- Kantatsu Co. Ltd.

- Sekonix Co. Ltd.

- Asia Optical Co. Inc.

- Kinko Optical Co. Ltd.

- Haesung Optics Co. Ltd.

- OFILM Group Co. Ltd.

- Newmax Technology Co. Ltd.

- KMOT Co. Ltd.

- Tianyang Optical Technology Co. Ltd.

- Ability Opto-Electronics Technology Co. Ltd.

- Tamron Co. Ltd.

- Hoya Group

- Nidec Sankyo Corp.

- Calin Technology Co. Ltd.

- Fujinon Corporation

- Sekonic Holdings

- Light Co.

- Truemax Engineering Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Multi-Camera Smartphones

- 4.2.2 Megapixel Race Above 50 MP Lifting Lens ASPs

- 4.2.3 Rapid Adoption of Periscope and Telephoto Modules

- 4.2.4 AI-Centric Computational Photography Requirements

- 4.2.5 Localised Lens Supply-Chain Build-Out in India and Vietnam

- 4.2.6 Glass-Plastic Free-Form Lenses for Foldables and Wearables

- 4.3 Market Restraints

- 4.3.1 Global Smartphone Unit Saturation

- 4.3.2 Aggressive Pricing Pressure in Mid- and Low-Tier Handsets

- 4.3.3 High-Layer Hybrid Lens Yield Challenges

- 4.3.4 Export-Control Risk on Precision Glass-Moulding Tools

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Lens Technology

- 5.1.1 Wide/Primary

- 5.1.2 Ultra-Wide

- 5.1.3 Telephoto

- 5.1.4 Macro/Depth

- 5.2 By Lens Material

- 5.2.1 All-Glass

- 5.2.2 All-Plastic

- 5.2.3 Glass-Plastic Hybrid

- 5.3 By Camera Position

- 5.3.1 Rear-Primary

- 5.3.2 Rear-Secondary

- 5.3.3 Front/Facing

- 5.4 By Manufacturing Process

- 5.4.1 Glass Compression Moulding

- 5.4.2 Injection Moulding

- 5.4.3 Precision Glass Moulding

- 5.4.4 Other Manufacturing Process

- 5.5 By Smartphone Tier

- 5.5.1 Flagship

- 5.5.2 Mid-Range

- 5.5.3 Entry-Level

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Largan Precision Co. Ltd.

- 6.4.2 Sunny Optical Technology (Group) Co. Ltd.

- 6.4.3 Samsung Electro-Mechanics Co. Ltd.

- 6.4.4 Genius Electronic Optical Co. Ltd.

- 6.4.5 AAC Technologies Holdings Inc.

- 6.4.6 LG Innotek Co. Ltd.

- 6.4.7 Kantatsu Co. Ltd.

- 6.4.8 Sekonix Co. Ltd.

- 6.4.9 Asia Optical Co. Inc.

- 6.4.10 Kinko Optical Co. Ltd.

- 6.4.11 Haesung Optics Co. Ltd.

- 6.4.12 OFILM Group Co. Ltd.

- 6.4.13 Newmax Technology Co. Ltd.

- 6.4.14 KMOT Co. Ltd.

- 6.4.15 Tianyang Optical Technology Co. Ltd.

- 6.4.16 Ability Opto-Electronics Technology Co. Ltd.

- 6.4.17 Tamron Co. Ltd.

- 6.4.18 Hoya Group

- 6.4.19 Nidec Sankyo Corp.

- 6.4.20 Calin Technology Co. Ltd.

- 6.4.21 Fujinon Corporation

- 6.4.22 Sekonic Holdings

- 6.4.23 Light Co.

- 6.4.24 Truemax Engineering Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment