PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071220

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071220

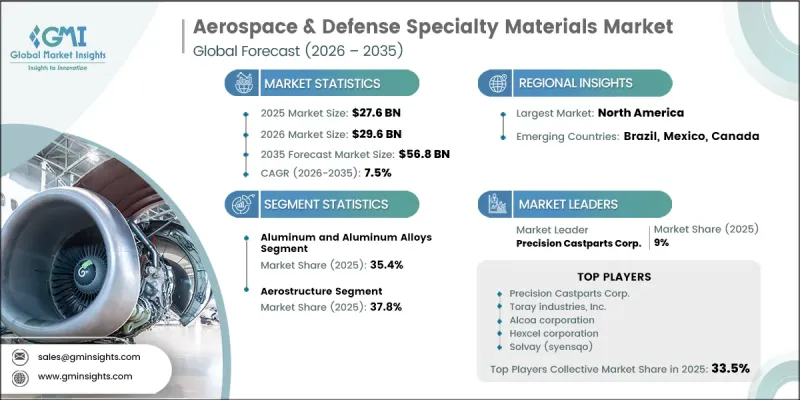

Aerospace and Defense Specialty Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Aerospace & Defense Specialty Materials Market was valued at USD 27.6 billion in 2025 and is estimated to grow at a CAGR of 7.5% to reach USD 56.8 billion by 2035.

Market expansion is driven by increasing commercial aircraft production rates, rising defense spending across NATO members and Indo-Pacific economies, and stricter sustainability requirements that are accelerating the adoption of lightweight, high-performance material solutions. The industry is undergoing a clear structural transition away from traditional steel-based systems toward aluminum alloys, titanium, advanced composites, and superalloys as aerospace manufacturers pursue higher efficiency, durability, and fuel performance targets. In parallel, the growing deployment of hypersonic defense systems, satellite constellations, and reusable space launch platforms is widening the application scope for specialty materials beyond conventional aircraft structures. Defense modernization initiatives across allied nations are also sustaining long-term demand across fighter jets, naval systems, armored vehicles, and missile technologies, reinforcing the strategic importance of advanced material innovation across aerospace and defense supply chains.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $27.6 Billion |

| Forecast Value | $56.8 Billion |

| CAGR | 7.5% |

The aluminum and aluminum alloys accounted for 35.4% share in 2025, maintaining their position as the leading material category due to their favorable strength-to-weight ratio, ease of fabrication, and cost efficiency across multiple aerospace applications. These materials remain widely utilized in primary and secondary structural components across both commercial and defense aircraft platforms. Their extensive use is supported by established manufacturing processes and long-standing integration into certified aerospace design standards, ensuring continued demand across the industry.

The aerostructure applications segment held a 37.8% share in 2025. This category includes major aircraft structures that must meet stringent safety, performance, and certification requirements. Continuous innovation in aircraft design and material engineering is supporting the increasing use of advanced alloys, composites, and high-performance metals across structural applications in both commercial and defense aviation sectors.

North America Aerospace & Defense Specialty Materials Market held 38% share in 2025, making it the largest regional contributor. The region's dominance is supported by a strong concentration of aerospace manufacturing activity, extensive defense procurement programs, and a well-established ecosystem of aircraft and space system developers. High investment levels in advanced aircraft platforms and next-generation defense technologies continue to reinforce the region's leadership position in specialty materials demand.

Major companies operating in the global aerospace & defense specialty materials market include Hexcel Corporation, Toray Industries, Inc., Solvay (Syensqo), Teijin Limited, Alcoa Corporation, Precision Castparts Corp., ATI (Allegheny Technologies Incorporated), SGL Carbon, Mitsubishi Chemical Group Corporation, Carpenter Technology Corporation, Victrex plc, Huntsman International LLC, Voestalpine Bohler Edelstahl GmbH, Arris Composites, Inc., Albany International Corporation, and Swiss Steel Group. Companies operating in the aerospace & defense specialty materials market are focusing on strategic initiatives to strengthen their competitive positioning and expand market reach. Key strategies include increasing investment in advanced material research and development to enhance strength, durability, thermal resistance, and weight reduction capabilities. Market participants are also prioritizing the development of next-generation composites, titanium alloys, and high-performance polymers tailored for aerospace and defense applications. Strategic collaborations with aircraft manufacturers, defense contractors, and space system developers are helping accelerate product integration and adoption. Companies are expanding production capacities and optimizing supply chains to meet rising demand from commercial aviation and defense programs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Material Type

- 2.2.2 Application

- 2.2.3 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Commercial Aircraft Production & Fleet Modernization Programs

- 3.2.1.2 Increased Defense Spending & Military Modernization Initiatives

- 3.2.1.3 Lightweighting Mandates for Fuel Efficiency & Emissions Reduction

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply Chain Consolidation & Limited Qualified Mill Capacity

- 3.2.2.2 Geopolitical Material Dependencies

- 3.2.3 Market opportunities

- 3.2.3.1 Development of Sustainable & Recycled Aerospace Materials

- 3.2.3.2 Additive Manufacturing & Near-Net-Shape Processing Expansion

- 3.2.3.3 Domestic Production Capacity Building

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By Active Ingredient

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Aluminum & aluminum alloys

- 5.2.1 2xxx series (High Strength, Copper-Based)

- 5.2.2 7xxx series (High Strength, Zinc-Based)

- 5.2.3 Other aluminum alloys

- 5.3 Titanium & titanium alloys

- 5.3.1 Grade 5 (Ti-6Al-4V)

- 5.3.2 Grade 9 & other aerospace grades

- 5.3.3 Beta titanium alloys

- 5.4 Composites

- 5.4.1 Polymer matrix composites (PMCs)

- 5.4.2 Metal matrix composites (MMCs)

- 5.4.3 Ceramic matrix composites (CMCs)

- 5.5 Superalloys

- 5.5.1 Nickel-based superalloys (Inconel, Hastelloy)

- 5.5.2 Cobalt-based superalloys

- 5.6 Steel & specialty steels

- 5.6.1 Stainless steel alloys (300 & 400 Series, 17-4PH)

- 5.6.2 High-strength structural steels

- 5.6.3 Tool steels

- 5.7 High-performance polymers & plastics

- 5.7.1 PEEK & high-temperature thermoplastics

- 5.7.2 Thermoset resins & prepregs

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Aerostructure

- 6.2.1 Wings & wing structures

- 6.2.2 Fuselage & tail sections

- 6.2.3 Fairings & nacelles

- 6.3 Propulsion systems

- 6.3.1 Turbine engines & components

- 6.3.2 Exhaust systems

- 6.3.3 Propulsion mounts & supports

- 6.4 Components

- 6.4.1 Landing gear systems

- 6.4.2 Hydraulic & pneumatic components

- 6.4.3 Actuators & control surfaces

- 6.5 Cabin interiors

- 6.5.1 Seating systems

- 6.5.2 Interior panels & linings

- 6.5.3 Galley & lavatory structures

- 6.6 Equipment, systems & support

- 6.6.1 Avionics housings

- 6.6.2 Fasteners & brackets

- 6.6.3 Wiring & cable management systems

- 6.7 Satellites & space systems

- 6.7.1 Satellite structures & bus systems

- 6.7.2 Thermal protection systems

- 6.7.3 Launch vehicle structures

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Toray industries, Inc.

- 8.2 Hexcel corporation

- 8.3 Solvay (syensqo)

- 8.4 Teijin limited

- 8.5 Precision Castparts Corp.

- 8.6 Alcoa corporation

- 8.7 ATI (Allegheny Technologies Incorporated)

- 8.8 SGL carbon

- 8.9 Mitsubishi chemical group corporation

- 8.10 Swiss steel group

- 8.11 Carpenter technology corporation

- 8.12 Voestalpine bohler edelstahl gmbh

- 8.13 Arris composites, Inc.

- 8.14 Albany international corporation

- 8.15 Victrex plc

- 8.16 Huntsman international LLC