PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061731

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061731

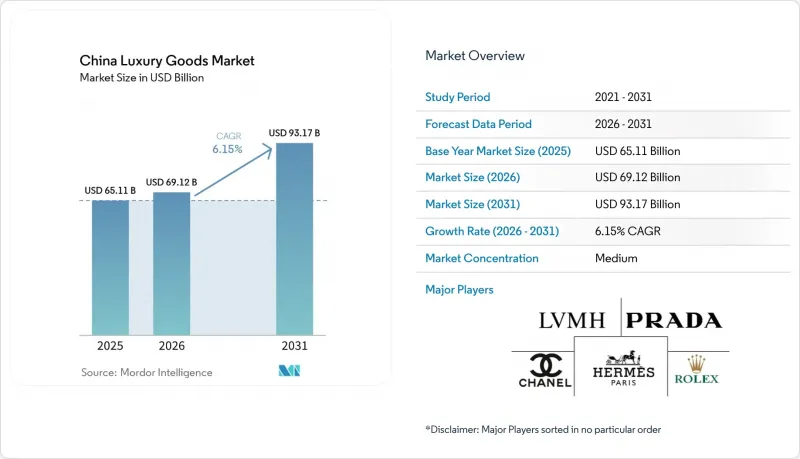

China Luxury Goods - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the china luxury goods market size was valued at USD 65.11 billion in 2025 and estimated to grow from USD 69.12 billion in 2026 to reach USD 93.17 billion by 2031, at a CAGR of 6.15% during the forecast period (2026-2031).

This report is Segmented by Product Type (Clothing and Apparel, Footwear, Eyewear, Leather Goods, Jewelry, Watches, and Beauty and Personal Care), End User (Men, Women, and Unisex), Distribution Channel (Offline Stores and Online Stores). The Market Forecasts are Provided in Terms of Value (USD).

China Luxury Goods Market Trends and Insights

Strategic expansion by foreign brands

International luxury brands are strategically expanding their presence in China through multiple initiatives, including increasing their retail footprint in tier-1 and emerging tier-2 cities. These companies are strengthening their digital presence through omnichannel strategies while developing China-exclusive collections through collaborations with local designers and artists. The establishment of regional headquarters and distribution centers in China enables these brands to improve their operational efficiency and market responsiveness. The companies are also implementing localized marketing campaigns and advanced customer relationship management systems to better understand and serve Chinese consumers. This concentrated focus on the Chinese market reflects its significant growth potential and increasing consumer sophistication. In December 2024, Balenciaga demonstrated this commitment by launching its largest global flagship store in China, featuring a minimalist, futuristic design that echoes the brand's raw architecture concept. These strategic expansions position luxury brands to capitalize on the evolving luxury goods market.

Growing demand for sustainable high-end materials

The increasing focus on sustainability in China's luxury market has emerged as a significant growth driver, particularly among younger consumers who are actively reshaping consumption patterns. Chinese luxury consumers demonstrate a strong preference for environmentally responsible products and show willingness to pay premium prices for sustainable offerings. This market evolution has prompted luxury brands to adapt their strategies by incorporating sustainable materials and establishing transparent supply chains. The transformation is exemplified by initiatives such as Kering's February 2024 collaboration with Tsinghua University and Institut Francais de la Mode (IFM) to launch a Massive Open Online Course focused on sustainable fashion practices. The integration of environmental responsibility into luxury products has become fundamental to Chinese consumers' perception of quality and exclusivity, making sustainability a crucial factor in purchasing decisions within the country's luxury goods market landscape.

Availability of counterfeit products

The widespread availability of counterfeit luxury goods poses a significant challenge to China's luxury market, with the country accounting for approximately 80% of global counterfeit production, according to World Trademark Review. China's extensive manufacturing capabilities and established distribution networks facilitate the production and sale of fake luxury items. Despite government efforts to combat counterfeiting through stricter regulations and enforcement measures, the market continues to be flooded with replicas of high-end brands. These counterfeit products impact the revenue of legitimate luxury brands and affect consumer trust and brand value. The presence of sophisticated counterfeits, often manufactured using similar materials and techniques, makes it difficult for consumers to distinguish between authentic and fake products. The lower price points of counterfeit goods attract price-sensitive consumers, particularly in tier-2 and tier-3 cities, leading to reduced sales of authentic luxury products. Furthermore, digital marketplaces facilitate grey market channels and parallel distribution networks, which undermine official sales networks and disrupt brand pricing strategies.

Other drivers and restraints analyzed in the detailed report include:

- Rapid expansion of e-commerce platforms and digital retail channels

- Government policies promoting domestic consumption and reducing import tariffs on luxury goods

- Lesser demand from price sensitive consumers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The China luxury market is dominated by leather goods, which holds a 27.12% share in 2025. This dominance stems from leather goods' perceived investment value and status symbol significance. The segment's strength is supported by China's established manufacturing infrastructure, expanding middle-class population, and rising disposable incomes. The market continues to grow through e-commerce integration and the established presence of domestic and international brands. Beauty and personal care is emerging as the fastest-growing segment with a projected CAGR of 5.52% (2026-2031), while watches and jewelry maintain substantial market share due to their value retention during economic uncertainty.

The guochao movement has significantly influenced luxury segments, particularly in clothing and apparel through the revival of traditional Hanfu clothing. Companies such as Shisanyu and Xiannixiaozhu have established themselves through their Hanfu designs. In response to increasing national pride and cultural confidence, luxury brands are incorporating Chinese design elements into their products. This cultural integration extends across all luxury categories, influencing product development in leather goods, beauty products, and other segments.

List of Companies Covered in this Report:

- LVMH Moet Hennessy Louis Vuitton SE

- Chanel SA

- Rolex SA

- Hermes International SA

- Prada Holding S.P.A

- Kering SA

- Compagnie Financiere Richemont SA

- The Swatch Group Ltd.

- Chow Tai Fook Jewellery Group Ltd.

- Chow Sang Sang Holdings International Ltd.

- Shanghai Tang Ltd.

- Li-Ning

- Bosideng International Holdings Ltd.

- Lao Feng Xiang Co., Ltd.

- DJI Luxury

- Tapestry Inc.

- Burberry Group plc

- Estee Lauder Companies Inc.

- L'Oreal SA

- Shiseido Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strategic expansion by foreign brands

- 4.2.2 Growing demand for sustainable high-end materials

- 4.2.3 Aggressive marketing by reputed brands

- 4.2.4 Product innovation in terms of raw material and design

- 4.2.5 Rapid expansion of e-commerce platforms and digital retail channels

- 4.2.6 Government policies promoting domestic consumption and reducing import tariffs on luxury goods

- 4.3 Market Restraints

- 4.3.1 Availablity of counterfeit products

- 4.3.2 Lesser demand from price sensitive consumers

- 4.3.3 Economic uncertainty and potential slowdown affecting consumer confidence and spending

- 4.3.4 Growing competition from premium domestic brands in certain product categories

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Clothing and Apparel

- 5.1.2 Footwear

- 5.1.3 Eyewear

- 5.1.4 Leather Goods

- 5.1.5 Jewelry

- 5.1.6 Watches

- 5.1.7 Beauty and Personal Care

- 5.2 By End User

- 5.2.1 Men

- 5.2.2 Women

- 5.2.3 Unisex

- 5.3 By Distribution Channel

- 5.3.1 Offline Stores

- 5.3.2 Online Stores

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 LVMH Moet Hennessy Louis Vuitton SE

- 6.4.2 Chanel SA

- 6.4.3 Rolex SA

- 6.4.4 Hermes International SA

- 6.4.5 Prada Holding S.P.A

- 6.4.6 Kering SA

- 6.4.7 Compagnie Financiere Richemont SA

- 6.4.8 The Swatch Group Ltd.

- 6.4.9 Chow Tai Fook Jewellery Group Ltd.

- 6.4.10 Chow Sang Sang Holdings International Ltd.

- 6.4.11 Shanghai Tang Ltd.

- 6.4.12 Li-Ning

- 6.4.13 Bosideng International Holdings Ltd.

- 6.4.14 Lao Feng Xiang Co., Ltd.

- 6.4.15 DJI Luxury

- 6.4.16 Tapestry Inc.

- 6.4.17 Burberry Group plc

- 6.4.18 Estee Lauder Companies Inc.

- 6.4.19 L'Oreal SA

- 6.4.20 Shiseido Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK