PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071246

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071246

Coal Ash Utilization and Disposal Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

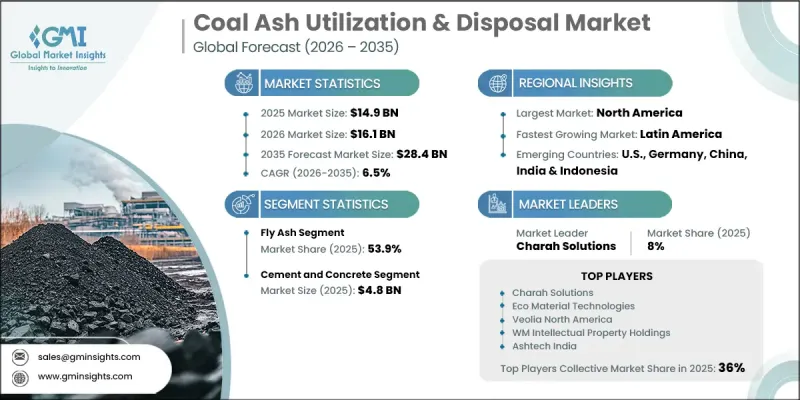

The Global Coal Ash Utilization and Disposal Market was valued at USD 14.9 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 28.4 billion by 2035.

Growth in the coal ash utilization and disposal industry is driven by the combined influence of infrastructure development, sustainability-focused resource management initiatives, and increasing environmental remediation activities. Demand remains strong across the construction sector, where coal ash serves as a widely accepted supplementary cementitious material that supports both cost efficiency and sustainability objectives. Regulatory frameworks promoting responsible ash handling and disposal practices are further accelerating market expansion. Growing construction activity in rapidly developing regions continues to strengthen demand for coal ash-derived materials, while manufacturers are increasingly incorporating supplementary cementitious materials into long-term decarbonization strategies. From an economic perspective, coal ash offers significant cost advantages compared to conventional raw material alternatives in several industrial applications. Within cement production, fly ash provides a competitively priced substitute for traditional cementitious inputs while maintaining performance standards in blended formulations. In addition, government-funded infrastructure development projects are increasing the use of fly ash-enhanced construction materials and ash-derived fill products, creating additional growth opportunities across the global coal ash utilization and disposal market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.9 Billion |

| Forecast Value | $28.4 Billion |

| CAGR | 6.5% |

Among material types, the fly ash segment held a 53.9% share in 2025 and is anticipated to grow at a CAGR of 7% through 2035. Its strong market presence is supported by favorable performance characteristics, reliable supply availability, and broad acceptance across multiple industrial applications. Fly ash is widely utilized due to its ability to enhance material properties while supporting efficient production processes. Consistent quality and large-scale availability continue to reinforce its commercial attractiveness, contributing to sustained demand across developed and emerging markets alike. The material remains a critical component in a wide range of construction and infrastructure-related applications, further strengthening its leadership position within the industry.

The cement and concrete application segment generated USD 4.8 billion in 2025, representing 32.2% share. The segment is forecast to grow at a CAGR of 7.3% through 2035. Demand growth is being fueled by increasing emphasis on reducing carbon emissions while maintaining economic efficiency in construction material production. The incorporation of fly ash into cement and concrete formulations enables manufacturers to reduce reliance on conventional cement components while preserving required performance characteristics. As sustainability targets become increasingly important across the construction sector, the use of coal ash-derived materials is expected to remain a key strategy for balancing environmental objectives with operational cost management.

North America Coal Ash Utilization and Disposal Market held 43.2% share in 2025. Market growth across the region is supported by evolving environmental regulations governing ash storage, monitoring, and disposal practices. Updated compliance requirements related to site management, groundwater oversight, and closure activities are creating substantial opportunities for service providers specializing in ash handling, remediation, engineering, and disposal solutions. As utility operators continue implementing regulatory compliance measures, demand for professional management services and large-scale remediation projects is expected to remain a significant driver of regional market expansion.

Key participants operating in the global coal ash utilization and disposal market include ASH GROVE, Ashtech India, Burns & McDonnell, Casila Infracon, CEMEX, Charah Solutions, Clean Harbors, DTE Energy, Eco Material Technologies, Enviro Corporation, GEOCYCLE, Heidelberg Materials, ICM Marshall, JAYCEE BUILDCORP LLP, REFEX, RPM Solutions, Salt River Materials Group, Titan America, Veolia North America, and WM Intellectual Property Holdings. Companies competing in the coal ash utilization and disposal industry are adopting a range of strategic initiatives to strengthen their market presence and improve competitive positioning. Market participants are expanding processing and recycling capabilities to maximize the commercial value of coal ash-derived products while meeting evolving environmental standards. Investments in advanced beneficiation technologies, material recovery systems, and sustainable disposal solutions are helping companies enhance operational efficiency and product quality. Strategic collaborations with utilities, construction material manufacturers, and infrastructure developers are also enabling firms to secure long-term supply agreements and expand customer reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Ash type trends

- 2.1.3 Method trends

- 2.1.4 Application trends

- 2.1.5 Service type trends

- 2.1.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of coal ash utilization & disposal

- 3.8 Emerging opportunities & trends

- 3.9 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

- 3.11 Capacity & production landscape (Driven by Primary Research)

- 3.11.1 Capacity by region & key producer (Driven by Primary Research)

- 3.11.2 Capacity utilization rates & expansion pipelines (Driven by Primary Research)

- 3.12 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.12.1 AI-Driven production optimization (Driven by Primary Research)

- 3.12.2 Predictive maintenance & fault detection (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Ash Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Fly ash

- 5.3 Bottom ash

- 5.4 Boiler slag

- 5.5 FGD gypsum

- 5.6 FBC ash

- 5.7 Others

Chapter 6 Market Size and Forecast, By Method, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Utilization

- 6.3 Disposal

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Cement & concrete

- 7.3 Bricks & blocks

- 7.4 Road construction & infrastructure

- 7.5 Wallboard & gypsum products

- 7.6 Mine reclamation

- 7.7 Agriculture

- 7.8 Waste stabilization

- 7.9 Others

Chapter 8 Market Size and Forecast, By Service Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Collection & handling

- 8.3 Transportation & logistics

- 8.4 Beneficiation & processing

- 8.5 Disposal & landfill management

- 8.6 Pond closure & remediation

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 Italy

- 9.3.4 France

- 9.3.5 Poland

- 9.3.6 Czech Republic

- 9.3.7 Turkey

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Indonesia

- 9.4.7 Malaysia

- 9.4.8 Vietnam

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Morocco

- 9.5.4 South Africa

- 9.5.5 Egypt

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Chile

- 9.6.3 Argentina

- 9.6.4 Colombia

Chapter 10 Company Profiles

- 10.1 ASH GROVE

- 10.2 Ashtech India

- 10.3 Burns & McDonnell

- 10.4 Casila Infracon

- 10.5 CEMEX

- 10.6 Charah Solutions

- 10.7 Clean Harbors

- 10.8 DTE Energy

- 10.9 Eco Material Technologies

- 10.10 Enviri Corporation

- 10.11 GEOCYCLE

- 10.12 Heidelberg Materials

- 10.13 ICM Marshall

- 10.14 JAYCEE BUILDCORP LLP

- 10.15 REFEX

- 10.16 RPM Solutions

- 10.17 Salt River Materials Group

- 10.18 Titan America

- 10.19 Veolia North America

- 10.20 WM Intellectual Property Holdings