PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071347

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071347

Zero-Emission Heavy Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

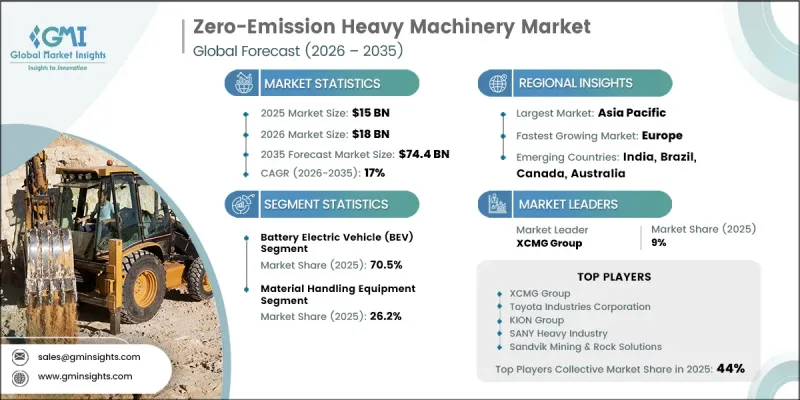

The Global Zero-Emission Heavy Machinery Market was valued at USD 15 billion in 2025 and is estimated to grow at a CAGR of 17% to reach USD 74.4 billion in 2035.

Market expansion is driven by the alignment of global decarbonization mandates, improving battery economics, and increasing operational viability of electrified heavy equipment in regulated industrial applications. Regulatory pressure on non-road mobile machinery emissions has intensified across major economies, accelerating the replacement of diesel-based fleets with zero-emission alternatives. The European Union's Stage V standards for non-road machinery have established a strict baseline, while several European countries have already implemented even more stringent procurement requirements for construction and industrial equipment used in high-emission environments. Lifecycle cost analysis increasingly favors electric heavy machinery as operating efficiency gains, reduced maintenance requirements, and lower fuel dependency offset higher upfront capital costs over multi-year usage cycles. The ongoing evolution of energy storage systems, charging infrastructure, and electrified drivetrains continues to strengthen the commercial feasibility of zero-emission equipment, positioning the market for sustained long-term expansion across global industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15 Billion |

| Forecast Value | $74.4 Billion |

| CAGR | 17% |

The battery electric vehicle (BEV) platforms segment held a 70.5% share, representing USD 10.6 billion in 2025. The leadership of BEV systems is supported by the maturity of lithium-ion battery technology, cost efficiency improvements, and compatibility with compact and mid-sized machinery applications. Their ability to operate effectively within standard shift cycles without requiring extensive charging infrastructure has further strengthened adoption across industrial use cases.

The material handling equipment segment held a 26.2% share, generating USD 3.9 billion. Growth is driven by strong adoption of electric forklifts, automated warehouse transport systems, and port logistics machinery, where operational patterns align effectively with battery charging cycles. These applications benefit from electrification due to predictable usage schedules, indoor operation environments, and increasing automation in logistics infrastructure.

North America Zero-Emission Heavy Machinery Market accounted for 20% share in 2025, representing USD 3 billion. The United States leads regional demand, supported by evolving emissions regulations for off-road machinery and increasing adoption of clean construction and industrial equipment. Regulatory frameworks governing non-road emissions continue to drive fleet modernization, encouraging the replacement of diesel-powered machinery with electric alternatives across construction, mining, and logistics operations.

Major companies operating in the global zero-emission heavy machinery market include Volvo Construction Equipment, Komatsu Ltd., Caterpillar Inc., CNH Industrial, XCMG Group, SANY Heavy Industry, Liebherr Group, JCB Ltd., Sandvik AB, Terex Corporation, Epiroc AB, Wacker Neuson SE, Hyster-Yale Group, Inc., Toyota Industries Corporation, KION Group, CATL, Allison Transmission, Forsee Power, Ballard Power Systems Inc., PowerCell Group AB, and Kreisel Electric GmbH & Co KG. Companies operating in the zero-emission heavy machinery market are adopting multiple strategic approaches to strengthen their market position and accelerate adoption. A primary focus is the development of advanced battery-electric and hybrid powertrain systems designed to improve operational efficiency and reduce the total cost of ownership. Manufacturers are also investing heavily in battery technology partnerships and in-house energy storage development to enhance performance and extend equipment runtime. Expansion of charging infrastructure ecosystems and modular energy solutions is another key strategy aimed at improving deployment flexibility across construction and mining sites. Companies are increasingly prioritizing fleet integration capabilities, digital monitoring systems, and predictive maintenance tools to enhance equipment lifecycle management.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Machinery Type

- 2.2.4 Battery Capacity

- 2.2.5 Application

- 2.2.6 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Technology & Innovation Landscape

- 3.5 Regulatory landscape

- 3.6 Impact on forces

- 3.6.1 Growth drivers

- 3.6.2 Industry pitfalls & challenges

- 3.6.3 Opportunities

- 3.7 Pricing analysis, 2025 (driven by primary research)

- 3.7.1 Historical price trend analysis (2022-2025)

- 3.7.2 Pricing strategy by player type (premium/value/cost-plus)

- 3.7.3 Regional price variation analysis

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Trade data analysis (driven by paid database)

- 3.11.1 Import/export volume & value trends (Driven by Primary Research)

- 3.11.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer (Driven by Primary Research)

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Battery Electric Vehicle (BEV)

- 5.3 Hydrogen Fuel Cell (FCEV)

- 5.4 Plug-in Hybrid (PHEV)

- 5.5 Others (Emerging Powertrains)

Chapter 6 Market Estimates & Forecast, By Machinery Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Earthmoving & Excavation Equipment

- 6.3 Haulage & Dumping Equipment

- 6.4 Material Handling Equipment

- 6.5 Lifting & Access Equipment

- 6.6 Drilling & Foundation Equipment

- 6.7 Others (Mixers, Pavers, Compactors, Rollers, Sweepers)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Mining

- 7.4 Ports & Logistics Terminals

- 7.5 Agriculture

- 7.6 Industrial & Municipal

- 7.7 Others (Forestry, Defense, Specialized Off-Highway)

Chapter 8 Market Estimates & Forecast, By Battery Capacity, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Less Than 50 kWh

- 8.3 50 kWh to 200 kWh

- 8.4 200 kWh to 500 kWh

- 8.5 More Than 500 kWh

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 OEM Direct Sales

- 9.3 Dealer & Distributor Network

- 9.4 Rental & Leasing

- 9.5 Online & E-Commerce Platforms

Chapter 10 Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 U.K.

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Global players

- 11.1.1 Caterpillar Inc.

- 11.1.2 Komatsu Ltd.

- 11.1.3 Volvo Construction Equipment

- 11.1.4 Epiroc AB

- 11.1.5 Sandvik AB

- 11.1.6 Liebherr Group

- 11.1.7 SANY Heavy Industry

- 11.1.8 XCMG Group

- 11.1.9 JCB Ltd.

- 11.1.10 CATL

- 11.1.11 Toyota Industries Corporation

- 11.1.12 KION Group

- 11.2 Regional players

- 11.2.1 Ballard Power Systems Inc.

- 11.2.2 Terex Corporation

- 11.2.3 Hyster-Yale Group, Inc.

- 11.2.4 Wacker Neuson SE

- 11.2.5 CNH Industrial

- 11.2.6 Allison Transmission

- 11.3 Emerging players

- 11.3.1 Forsee Power

- 11.3.2 Kreisel Electric GmbH & Co KG

- 11.3.3 PowerCell Group AB