PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083068

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083068

Asia Pacific Zero-Emission Heavy Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

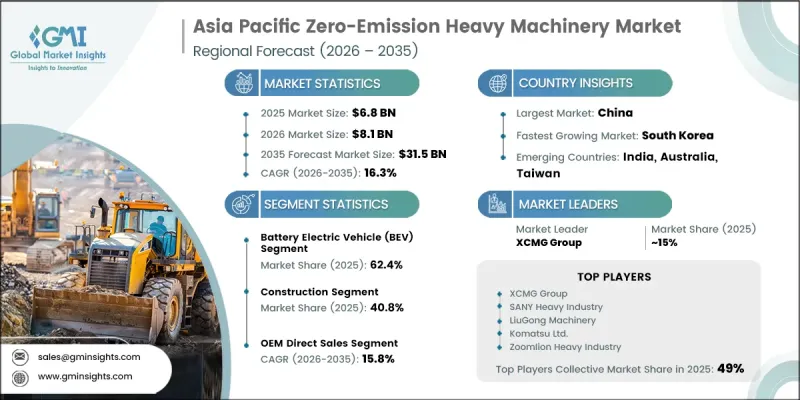

Asia-Pacific Zero-Emission Heavy Machinery Market was valued at USD 6.8 billion in 2025 and is estimated to grow at a CAGR of 16.3% to reach USD 31.5 billion by 2035.

Strong growth momentum is supported by tightening regional decarbonization commitments, accelerating electrification of industrial fleets, and rapid improvements in battery performance and cost efficiency. Demand is also being reinforced by the expansion of asset-light procurement models such as leasing and equipment rental, which are reducing upfront capital barriers for end users. The market is increasingly shaped by the convergence of large-scale infrastructure development, automation-driven jobsite planning, and electrified equipment integration strategies across mining and construction ecosystems. Rising investments in energy storage technologies and electrified drivetrain systems are further strengthening commercialization pathways for zero-emission machinery. As regulatory pressure intensifies and operational efficiency expectations rise, industries across Asia-Pacific are steadily shifting toward electrified heavy equipment solutions that offer lower emissions, reduced lifecycle costs, and improved compliance with environmental standards. These factors collectively position the Asia-Pacific Zero-Emission Heavy Machinery Market for sustained expansion over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.8 Billion |

| Forecast Value | $31.5 Billion |

| CAGR | 16.3% |

Battery electric drivetrain systems accounted for 62.4% share in 2025. Continued improvements in energy density, charging infrastructure expansion, and cost optimization of battery systems are strengthening adoption across heavy-duty applications. As electrification becomes more deeply embedded in industrial fleet modernization strategies, battery electric solutions are expected to maintain a dominant position while gradually sharing space with alternative zero-emission technologies in high-duty-cycle operations.

The construction segment represented 40.8% share in 2025 and is projected to grow at a CAGR of 16.1% through 2035. Strong infrastructure development activity across urban and semi-urban regions is driving consistent demand for electrified heavy machinery in earthmoving, material handling, and site development operations. Increasing adoption of low-emission equipment in regulated project zones is further accelerating market penetration. The segment continues to benefit from large-scale public infrastructure investments and the modernization of construction practices that emphasize sustainability, efficiency, and reduced environmental impact.

China Zero-Emission Heavy Machinery Market held a 44.9% share in 2025, supported by a deeply integrated industrial ecosystem spanning raw material processing, battery manufacturing, and heavy equipment production. The country's strong position is reinforced by its advanced supply chain capabilities and coordinated industrial policy framework that supports electrification across heavy industries. Continuous investment in battery innovation, manufacturing scale-up, and equipment electrification is further strengthening China's leadership in the regional market. Expanding deployment of zero-emission machinery across mining, construction, and logistics operations continues to enhance its dominance over the forecast period.

Key companies operating in the Asia-Pacific Zero-Emission Heavy Machinery Market include XCMG Group, BYD Co., Ltd., SANY Heavy Industry Co., Ltd., Komatsu Ltd., Zoomlion Heavy Industry Science & Technology Co., Ltd., LiuGong Machinery Co., Ltd., Hitachi Construction Machinery Co., Ltd., Kobelco Construction Machinery Co., Ltd., Doosan Bobcat, HD Hyundai, Yanmar Holdings Co., Ltd., China National Heavy Duty Truck Group Co., Ltd., Shandong Lingong Construction Machinery Co., Ltd., Shantui Construction Machinery Co., Ltd., Lingong Machinery Group Co., Ltd., EACON Mining Technology Co., Ltd., Samsung SDI Co., Ltd., Contemporary Amperex Technology Co. (CATL), REPT Battero Energy Co., Ltd., Horyong Engineering Co., Ltd., and Zijin Longking Environmental Technology Co., Ltd. Companies operating in the Asia-Pacific Zero-Emission Heavy Machinery Market are focusing on electrification innovation, strategic alliances, and localized manufacturing expansion to strengthen their competitive positioning. Major players are investing heavily in battery technology integration, drivetrain optimization, and energy-efficient system design to improve equipment performance and operational range. Partnerships with battery suppliers, infrastructure developers, and fleet operators are enabling faster deployment of zero-emission machinery across large-scale industrial projects. Manufacturers are also expanding production facilities within key Asian markets to reduce supply chain dependencies and improve cost efficiency. In addition, companies are enhancing after-sales service networks, digital monitoring systems, and predictive maintenance solutions to improve equipment uptime.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Business trends

- 2.2.1 Type

- 2.2.2 Machinery Type

- 2.2.3 Battery Capacity

- 2.2.4 Application

- 2.2.5 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Technology & Innovation Landscape

- 3.5 Regulatory landscape

- 3.6 Impact on forces

- 3.6.1 Growth drivers

- 3.6.2 Industry pitfalls & challenges

- 3.6.3 Opportunities

- 3.7 Pricing analysis, 2025 (driven by primary research)

- 3.7.1 Historical price trend analysis (2022-2025)

- 3.7.2 Pricing strategy by player type (premium/value/cost-plus)

- 3.7.3 Regional price variation analysis

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

- 3.11 Trade data analysis (driven by paid database)

- 3.11.1 Import/export volume & value trends (Driven by Primary Research)

- 3.11.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Producer (Driven by Primary Research)

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Battery Electric Vehicle (BEV)

- 5.3 Hydrogen Fuel Cell (FCEV)

- 5.4 Plug-in Hybrid (PHEV)

- 5.5 Others (Emerging Powertrains)

Chapter 6 Market Estimates & Forecast, By Machinery Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Earthmoving & Excavation Equipment

- 6.3 Haulage & Dumping Equipment

- 6.4 Material Handling Equipment

- 6.5 Lifting & Access Equipment

- 6.6 Drilling & Foundation Equipment

- 6.7 Others (Mixers, Pavers, Compactors, Rollers, Sweepers)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Mining

- 7.4 Ports & Logistics Terminals

- 7.5 Agriculture

- 7.6 Industrial & Municipal

- 7.7 Others (Forestry, Defense, Specialized Off-Highway)

Chapter 8 Market Estimates & Forecast, By Battery Capacity, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Less Than 50 kWh

- 8.3 50 kWh to 200 kWh

- 8.4 200 kWh to 500 kWh

- 8.5 More Than 500 kWh

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 OEM Direct Sales

- 9.3 Dealer & Distributor Network

- 9.4 Rental & Leasing

- 9.5 Online & E-Commerce Platforms

Chapter 10 Market Estimates and Forecast, By Country, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 China

- 10.3 Japan

- 10.4 India

- 10.5 South Korea

- 10.6 Australia

- 10.7 Taiwan

- 10.8 Singapore

- 10.9 Thailand

Chapter 11 Company Profiles

- 11.1 Tier 1 Global/Top PLAYERS

- 11.1.1 SANY Heavy Industry Co., Ltd.

- 11.1.2 XCMG Group

- 11.1.3 Komatsu Ltd.

- 11.1.4 Hitachi Construction Machinery Co., Ltd.

- 11.1.5 LiuGong Machinery Co., Ltd.

- 11.1.6 Zoomlion Heavy Industry Science & Technology Co., Ltd.

- 11.1.7 Contemporary Amperex Technology Co. (CATL)

- 11.1.8 BYD Co., Ltd.

- 11.2 Tier 2 REGIONAL/NICHE PLAYERS

- 11.2.1 HD Hyundai

- 11.2.2 Kobelco Construction Machinery Co., Ltd.

- 11.2.3 Shandong Lingong Construction Machinery Co., Ltd.

- 11.2.4 Shantui Construction Machinery Co., Ltd.

- 11.2.5 Samsung SDI Co., Ltd.

- 11.2.6 China National Heavy Duty Truck Group Co., Ltd.

- 11.2.7 Yanmar Holdings Co., Ltd.

- 11.3 Tier 3: Emerging players

- 11.3.1 Zijin Longking Environmental Technology Co., Ltd.

- 11.3.2 EACON Mining Technology Co., Ltd.

- 11.3.3 REPT Battero Energy Co., Ltd.

- 11.3.4 Lingong Machinery Group Co., Ltd.

- 11.3.5 Horyong Engineering Co., Ltd.

- 11.3.6 Doosan Bobcat