PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071373

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071373

North America On Grid Solar PV Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

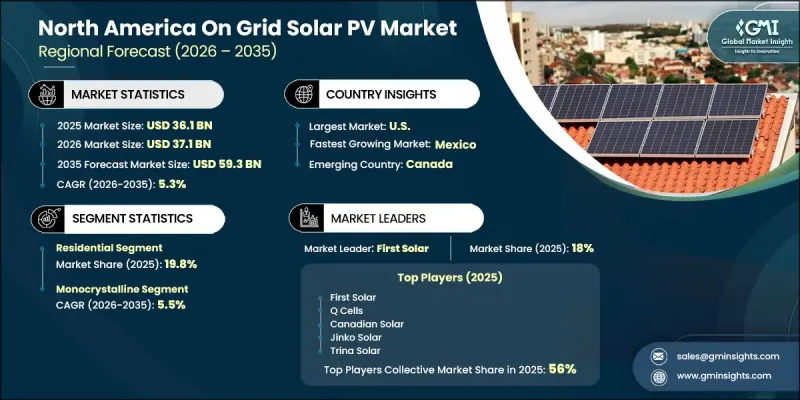

North America On-Grid Solar PV Market was valued at USD 36.1 billion in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 59.3 billion by 2035.

Market growth is driven by rising adoption of grid-connected solar systems across residential, commercial, and utility segments as end users seek to reduce reliance on conventional electricity and improve long-term energy cost stability. Expanding acceptance of solar energy across urban, suburban, and industrial environments is further reinforcing deployment momentum. Favorable climatic conditions across several regions are also supporting consistent solar generation, strengthening overall system performance and adoption. In parallel, policy support in the form of renewable energy standards, clean energy procurement frameworks, tax incentives, and utility-level decarbonization targets is encouraging large-scale investment in solar infrastructure. These mechanisms create a more predictable environment for developers, investors, and equipment suppliers. Declining system costs driven by manufacturing efficiencies, economies of scale, and intensifying competition are further accelerating adoption. At the same time, the availability of financing models such as loans, leases, and power purchase agreements is reducing upfront cost barriers for residential users. Together, these factors support steady market penetration across all major end-use segments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $36.1 Billion |

| Forecast Value | $59.3 Billion |

| CAGR | 5.3% |

The residential segment is expected to reach USD 12.5 billion by 2035, accounting for 19.8% share in 2025 and expanding at a CAGR of 6.1% through 2035. Growth in this segment is supported by rising consumer awareness of clean energy solutions and increasing electricity prices, which are prompting greater adoption of rooftop solar systems. Households and utilities are increasingly integrating solar PV systems to strengthen energy security while aligning with sustainability and emissions reduction goals. Rising homeowner investment in distributed solar installations is also contributing to long-term cost savings and greater energy independence, further strengthening residential market expansion.

Thin-film technology is projected to grow at a CAGR of 6.5% through 2035, particularly across utility-scale and specialized applications, supported by its operational flexibility despite lower efficiency levels compared to crystalline silicon technologies. Increasing emphasis on supply chain diversification and reduced dependence on imported crystalline silicon components is encouraging greater investment in thin-film production capacity, especially across North America and Europe. In addition, emerging use cases such as building-integrated photovoltaics, lightweight flexible solar modules, agrivoltaic systems, and mobility-based solar applications are expanding the addressable market for thin-film technologies and driving new growth opportunities.

U.S. On-Grid Solar PV Market is projected to reach USD 56 billion by 2035. Rising electricity demand, combined with the urgent need to decarbonize the power sector, is prompting utilities and large energy consumers to accelerate deployment of grid-connected solar systems nationwide. Continued grid modernization initiatives, along with growing integration of energy storage solutions, are improving the reliability and operational flexibility of solar PV systems. Expanding deployment supported by innovative financing structures and large-scale project development is further strengthening the country's solar energy landscape and reinforcing long-term market growth.

Key companies operating in the North America on-grid solar PV market include Trina Solar, First Solar, JinkoSolar, Canadian Solar, LONGi, SunPower Corporation, NextEra Energy, EDF Renewables, Enel Green Power, Recurrent Energy, QCells, Enbridge, GCL-SI, Grew Energy, Sunova Solar, Solar Cellz, T1 Energy, JA SOLAR Technology, BAUER Solar Canada, and Philadelphia Solar. Companies in the North America on-grid solar PV market are focusing on expanding utility-scale project portfolios and securing long-term power purchase agreements to ensure stable revenue streams. Many players are investing in advanced PV technologies, including high-efficiency modules and system optimization tools, to improve energy output and reduce the levelized cost of electricity. Strategic partnerships with utilities, governments, and large corporate buyers are being used to strengthen project pipelines and accelerate deployment. Firms are also increasing investments in domestic manufacturing facilities to reduce supply chain risks and qualify for incentive programs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Component trends

- 2.4 Technology trends

- 2.5 End use trends

- 2.6 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Technology and innovation landscape

- 3.8 Cost structure analysis

- 3.9 Price trend analysis (Driven by Primary Research)

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type

- 3.10 Trade data analysis (Driven by Primary Research)

- 3.10.1 Import/export value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Impact of AI & generative AI on the market [SOLUTION CORE]

- 3.11.1 Predictive maintenance & fault detection

- 3.11.2 Grid optimization & load forecasting

- 3.11.3 Digital twin simulation & testing

- 3.11.4 Risks, limitations & regulatory considerations

- 3.12 Emerging opportunities & trends

- 3.13 Digitalization & IoT integration

- 3.14 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2025

- 4.2.1 U.S.

- 4.2.2 Canada

- 4.2.3 Mexico

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Component, 2022 - 2035 (USD Billion & MW)

- 5.1 Key trends

- 5.2 Modules

- 5.3 Inverters

- 5.4 Trackers

- 5.5 BOS

Chapter 6 Market Size and Forecast, By Technology, 2022 - 2035 (USD Billion and MW)

- 6.1 Key trends

- 6.2 Monocrystalline

- 6.2.1 PERC

- 6.2.2 TopCon

- 6.2.3 HJT

- 6.2.4 IBC/TBC

- 6.3 Polycrystalline

- 6.4 Thin film

- 6.4.1 Cadmium Telluride

- 6.4.2 Amorphous Silicon

- 6.4.3 Copper Indium Gallium Diselenide

Chapter 7 Market Size and Forecast, By End Use, 2022 - 2035 (USD Billion and MW)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial & Industrial

- 7.4 Utility

Chapter 8 Market Size and Forecast, By Country, 2022 - 2035 (USD Billion and MW)

- 8.1 Key trends

- 8.2 U.S.

- 8.3 Canada

- 8.4 Mexico

Chapter 9 Company Profiles

- 9.1 BAUER Solar Canada

- 9.2 Canadian Solar

- 9.3 EDF Renewables

- 9.4 Enbridge

- 9.5 Enel Green Power

- 9.6 First Solar

- 9.7 GCL-SI

- 9.8 Grew Energy

- 9.9 JA SOLAR Technology

- 9.10 JinkoSolar

- 9.11 LONGi

- 9.12 NextEra Energy

- 9.13 Philadelphia Solar

- 9.14 QCells

- 9.15 Recurrent energy

- 9.16 Solar Cellz

- 9.17 Sunova Solar

- 9.18 SunPower Corporation

- 9.19 T1 Energy

- 9.20 Trina Solar