PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071380

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071380

Hairy Cell Leukemia Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

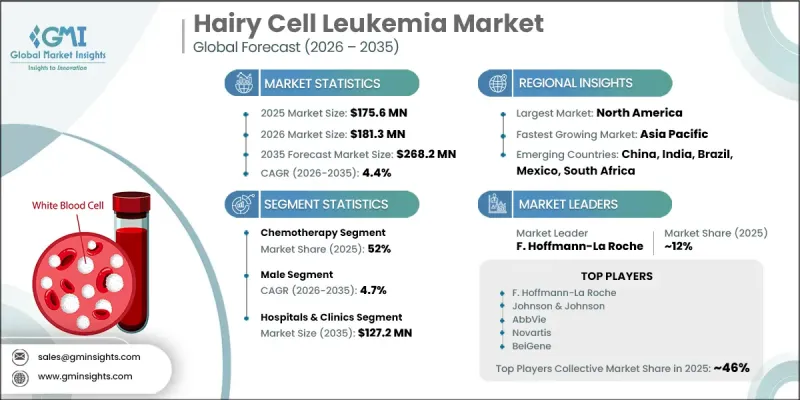

The Global Hairy Cell Leukemia Market was valued at USD 175.6 million in 2025 and is estimated to grow at a CAGR of 4.4% to reach USD 268.2 million by 2035.

Market expansion is supported by the rising incidence of hematologic cancers, ongoing improvements in diagnostic technologies, and increasing awareness of rare oncology conditions. Growth is further reinforced by a steady patient population across major healthcare systems and improved clinical recognition of hairy cell leukemia (HCL). Enhanced access to specialized oncology centers and earlier diagnostic interventions are contributing to timely treatment initiation and better disease management outcomes. In addition, favorable reimbursement support for orphan drugs and rising investment in rare disease research are creating a more supportive environment for market development. The increasing adoption of precision medicine, along with broader availability of targeted therapies, is also improving treatment effectiveness and expanding therapeutic options for patients. Continuous advancements in molecular diagnostics and strengthening healthcare infrastructure across developed and emerging regions are further supporting long-term market stability and growth momentum.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $175.6 Million |

| Forecast Value | $268.2 Million |

| CAGR | 4.4% |

Hairy cell leukemia is a rare chronic B-cell lymphoproliferative disorder characterized by abnormal B lymphocyte accumulation in the bone marrow, spleen, and peripheral blood. The condition is defined by the presence of malignant cells with hair-like projections visible under microscopic examination. It typically progresses slowly and is commonly associated with symptoms such as fatigue, recurrent infections, weakness, anemia, easy bruising, and splenic enlargement. Despite its slow progression, long-term monitoring and medical intervention are often required to manage complications and prevent disease advancement.

The chemotherapy segment accounted for 52% share in 2025, representing USD 91.3 million, and is projected to grow at a CAGR of 4.2% through 2035. This segment remains the primary treatment approach due to its well-established clinical efficacy and long-standing use in achieving durable remission in newly diagnosed patients. Purine analog therapies, particularly cladribine and pentostatin, continue to serve as core treatment options across major healthcare markets. Their proven clinical outcomes, strong physician familiarity, and sustained effectiveness support their continued dominance in the therapeutic landscape.

The male segment held a share of 76.3% in 2025, valued at USD 134 million, and is projected to reach USD 209.9 million by 2035, growing at a CAGR of 4.7%. This dominance is primarily linked to the significantly higher prevalence of hairy cell leukemia in men compared to women across global populations. As a result, males represent the largest patient group requiring diagnosis, ongoing treatment, and long-term disease management. This consistent gender-based disparity continues to drive higher treatment utilization and reinforces demand for both established and emerging therapeutic options.

North America Hairy Cell Leukemia Market accounted for USD 68.3 million in 2025 and is expected to reach USD 99.5 million by 2035. Regional leadership is driven by a well-established oncology care system, advanced diagnostic capabilities, and strong access to approved and emerging therapies for rare blood cancers. The region also benefits from active participation in rare disease research supported by leading academic institutions, pharmaceutical companies, and patient advocacy networks. Increasing adoption of molecular diagnostics, precision medicine approaches, and targeted treatment strategies is further improving patient outcomes and strengthening market expansion across North America.

Key companies operating in the global hairy cell leukemia industry include Roche, Novartis, Pfizer, AbbVie, Johnson & Johnson, Sanofi, Amgen, AstraZeneca, Gilead Sciences, Takeda Pharmaceutical, Astellas Pharma, Merck KGaA, BeiGene, and F. Hoffmann-La Roche. Companies in the hairy cell leukemia market are focusing on expanding their oncology portfolios through targeted therapy development and next-generation treatment innovations. Many players are investing heavily in research and clinical trials aimed at improving remission rates and reducing relapse risks. Strategic collaborations with research institutions and biotech firms are being used to accelerate drug discovery and expand pipeline capabilities. Firms are also strengthening their presence in rare disease segments by pursuing regulatory designations that support faster approvals and extended market exclusivity. In addition, increasing emphasis on precision medicine, biomarker-driven therapies, and improved diagnostic integration is helping companies enhance treatment personalization and strengthen competitive positioning in the rare hematologic oncology space.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Therapy trends

- 2.2.3 Gender trends

- 2.2.4 Treatment providers trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of targeted therapies

- 3.2.1.2 Increasing prevalence of leukemia

- 3.2.1.3 Increased research and development activities related to hairy cell leukemia

- 3.2.1.4 Expanding use of combination immunotherapy regimens

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment and biologic therapy costs

- 3.2.2.2 Limited availability of approved HCL-specific drugs

- 3.2.3 Market opportunities

- 3.2.3.1 Development of chemo-free treatment approaches

- 3.2.3.2 Emerging opportunities in relapse/refractory HCL treatment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.4.1 Current technology

- 3.4.2 Emerging technologies

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.6 Regulatory landscape (Driven by primary research)

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 Middle East and Africa

- 3.7 Reimbursement scenario

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Pipeline analysis

- 3.11 Future market trends (Driven by primary research)

- 3.12 Impact of AI and generative AI on the market

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Therapy, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Chemotherapy

- 5.3 Targeted therapy

- 5.4 Immunotherapy

- 5.5 Other therapies

Chapter 6 Market Estimates and Forecast, By Gender, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Male

- 6.3 Female

Chapter 7 Market Estimates and Forecast, By Treatment Providers, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals & clinics

- 7.3 Cancer care centers

- 7.4 Academic and research institutes

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AbbVie

- 9.2 Amgen

- 9.3 Astellas Pharma

- 9.4 AstraZeneca

- 9.5 BeiGene

- 9.6 F. Hoffmann-La Roche

- 9.7 Gilead Sciences

- 9.8 Johnson & Johnson

- 9.9 Merck KGaA

- 9.10 Novartis

- 9.11 Pfizer

- 9.12 Takeda Pharmaceutical

- 9.13 Sanofi